What if your old employer’s pension scheme is no longer the best home for your money, yet you’re worried that moving it might trigger a tax bill you didn’t see coming? It is completely natural to feel a sense of unease when your retirement savings are scattered across various past jobs, leaving you feeling disconnected from your own financial future. Many professionals share this fear of losing track of their pots or feeling stuck in restricted investment funds. Reclaiming control through a retirement bond Ireland offers a way to bring that money back under your own stewardship.

We believe that managing your future should be straightforward and stress-free. This 2026 reference guide is designed to show you how to consolidate those fragmented savings into one manageable place while fully protecting your tax-free lump sum entitlements. Whether you are navigating the new €2.2 million Standard Fund Threshold or simply seeking better investment flexibility, we will explain how these bonds work in practice. You’ll learn how to transition your funds into a personalised structure that offers the stability, clarity, and optimism you deserve as you plan for the years ahead.

Key Takeaways

- Understand how a Personal Retirement Bond grants you full ownership of your previous pension savings, moving them away from your former employer’s control for greater security.

- Learn how to choose your own investment funds to match your personal risk profile, ensuring your money is working effectively for your long-term goals.

- Discover why a retirement bond Ireland is a vital tool for safeguarding your pension pot when you move jobs or if a previous employer’s scheme closes.

- Clarify the differences between a PRB and a PRSA to ensure you select the most appropriate and tax-efficient home for your specific retirement savings.

- Explore how a professional review can remove the friction of dealing with trustees, allowing for a seamless transition to a consolidated and manageable financial future.

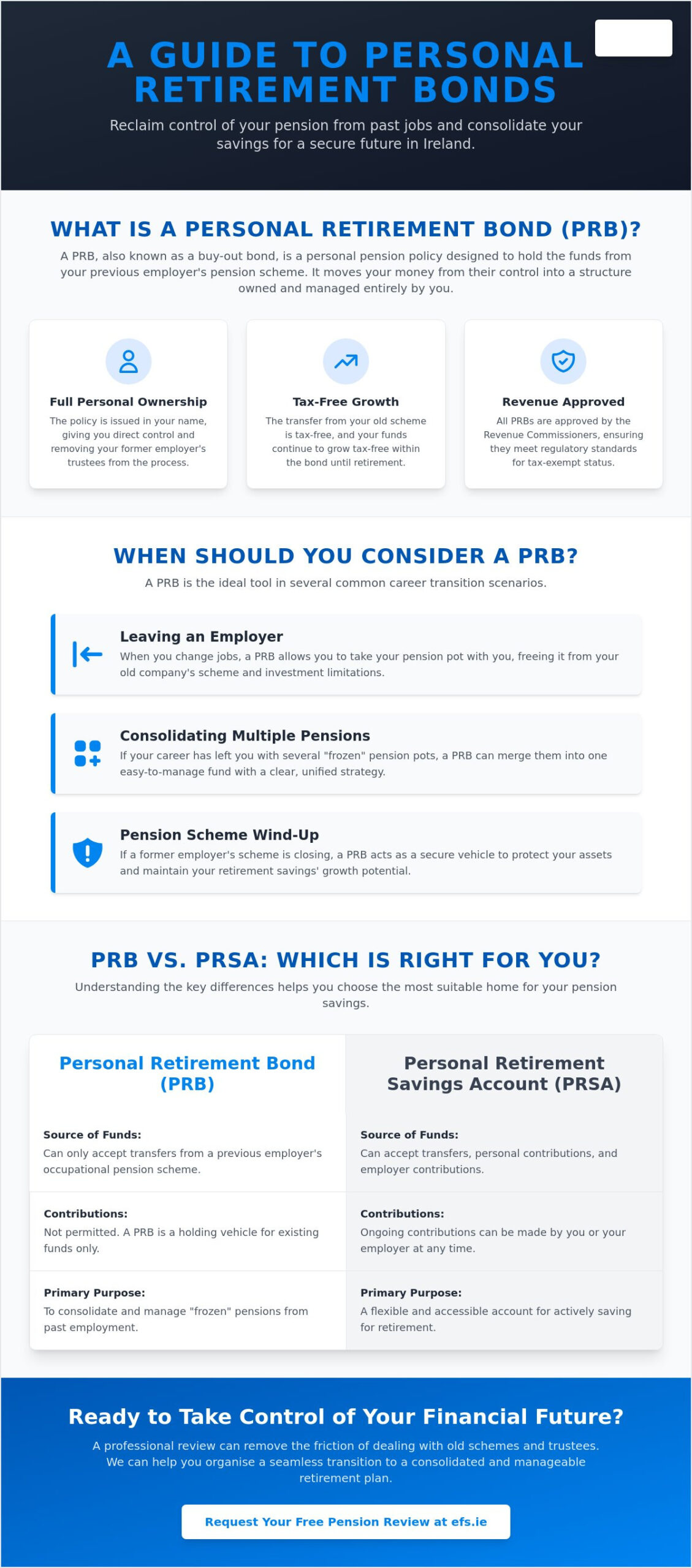

What is a Retirement Bond in Ireland?

A Personal Retirement Bond (PRB) is a private pension structure designed specifically to house the accumulated value of a pension from a previous employment. When you leave a company, your retirement savings often remain in a scheme managed by trustees who are still connected to your former workplace. By opting for a retirement bond Ireland residents can reclaim autonomy over their financial future. Essentially, a PRB is a buy-out bond that allows for a seamless transition of retirement assets from a group environment into an individual policy.

Choosing this path is a significant step toward personal financial stability. Instead of your money being tied to the decisions of a board of trustees, the policy is issued directly in your name. You gain full ownership and control. This means you decide how the funds are managed and which investment strategies align with your long-term goals. For a broader context on how these structures fit into the wider Irish Pension System Overview, it’s helpful to see them as the bridge between corporate employment and personal retirement planning.

How the PRB Structure Works

The mechanics of moving your funds are designed to be as frictionless as possible. The initial transfer from your old occupational scheme into the bond is a tax-free event, ensuring your hard-earned savings remain intact during the transition. Once the capital is safely within the bond, it continues to grow tax-free until you reach retirement age. Because you are now the sole policyholder, the trustees of your old job are no longer involved in your money. It’s a clean break that simplifies your financial landscape and offers a clear path forward.

The Role of the Revenue Commissioners

While you gain more control, the bond still operates within a strictly regulated framework. Every retirement bond Ireland providers offer must be approved by the Revenue Commissioners to maintain its vital tax-exempt status. It is also vital to remember that the rules regarding when and how you can access your funds remain linked to the original scheme’s rules. For instance, if your original scheme allowed for retirement at age 60, the bond usually preserves that right. One key distinction is that contributions cannot be made to a PRB once it is established; it serves strictly as a vehicle for existing funds already earned. If you are unsure how these rules apply to your specific situation, seeking a professional review at efs.ie can provide the clarity you need to move forward with confidence.

When Should You Consider a Personal Retirement Bond?

Career paths in Ireland are more dynamic than ever. It’s rare for someone to stay with a single employer for forty years. Whether you’ve decided to move on for a better opportunity or have recently faced a redundancy, these transitions often leave behind a “frozen” pension pot. This is precisely when a retirement bond Ireland becomes a strategic asset. By moving your funds, you ensure your savings aren’t left in a scheme where you no longer have a voice or direct influence over management decisions.

Leaving Your Current Employer

When you resign, you generally have three paths for your accumulated pension: leave it in the old scheme, move it to your new employer’s plan, or transfer it into a Personal Retirement Bond. While leaving it behind might seem the simplest route, it often limits your investment choices to whatever the former employer’s trustees have selected. A PRB allows you to break that link entirely. You gain access to a wider range of funds, from conservative cash-based options to high-growth equities, tailored to your own risk appetite.

This transition is governed by strict Revenue Rules on Pension Transfers, which ensure that moving your money doesn’t result in an immediate tax liability. It’s a safeguarding mechanism for your hard-earned capital. Sometimes, an employer might close a scheme altogether, known as a wind-up. In these cases, a PRB serves as the default safety net, protecting your assets whilst you decide on your next move. It keeps your money safe, portable, and ready for future growth.

Consolidating Multiple Pension Pots

Managing three or four different pensions from various stages of your career can be an administrative burden. It’s easy to lose track of passwords, annual statements, and fund performance across multiple providers. By pooling these assets into a single retirement bond Ireland professionals can create a central “hub” for their retirement strategy. This consolidation isn’t just about administrative ease; it’s often about long-term cost-efficiency.

- Reduced Fees: Multiple pots often mean multiple sets of annual management charges. Consolidating can help you gain a clearer view of your total wealth whilst potentially lowering cumulative costs.

- Simplified Tracking: A single bond provides one clear statement, making it much easier to monitor your progress toward your retirement goals.

- Better Control: You can align all your old savings with a single, coherent investment strategy rather than having mismatched funds scattered across different providers.

Taking a proactive approach helps you anticipate future needs rather than reacting to them. If you’re feeling overwhelmed by fragmented savings, organising a pension review can help you determine if consolidation is the right step for your specific journey. It’s about moving from uncertainty to a position of calm competence regarding your financial future.

The Key Benefits of a Retirement Bond for Your Pension Pot

Reclaiming your pension doesn’t just offer security; it provides a platform for growth. A retirement bond Ireland offers a level of personal agency that standard occupational schemes simply cannot match. You move from being a passive member of a group to the active owner of your financial destiny. This shift in stewardship is often the first step toward true peace of mind, as you transition from a state of uncertainty to one of calm competence.

The portability of the bond is a vital feature in a modern career. Once established, the bond stays with you regardless of where your future career takes you. It acts as a permanent, private container for your savings. You are no longer dependent on the former employer’s trustees for signatures or approvals, which removes a layer of stress that often complicates financial transitions. This “clean break” provides the stability needed to focus on your next professional chapter without worrying about the administrative hurdles of the past.

Tax efficiency remains a cornerstone of this structure. Any growth within the bond is exempt from Capital Gains Tax and Income Tax, allowing your capital to compound more effectively over time. For those seeking a deeper understanding of the broader landscape, the Citizens Information Guide to Pensions provides an excellent overview of how these tax-advantaged vehicles sit alongside other retirement options. By keeping your money in a dedicated pension environment, you maintain the same tax-free status it enjoyed in your original scheme.

Investment Flexibility and Choice

Most company schemes offer a limited “menu” of funds, often designed for the average employee rather than your specific needs. With a PRB, you can tailor your portfolio to match your personal risk appetite. Whether you prefer the stability of low-risk cash funds or the growth potential of international equity markets, the choice is yours. As of June 2026, yields on bonds suitable for retirement funds are approximately 4.5% to 5%, offering meaningful income streams for those approaching their transition. For those who are already maximising their pension contributions and looking for additional ways to reduce their income tax liability, exploring the EIIS scheme Ireland investors are using in 2026 can provide a powerful complement to your broader retirement strategy. For those considering how property investment might complement their pension strategy, understanding the requirements of a buy to let mortgage Ireland lenders currently offer can help you build a more diversified retirement income plan. Regular reviews with an advisor ensure your strategy evolves as your life stages change, keeping your future goals within reach.

Simplifying Your Retirement Planning

Consolidation brings clarity. Instead of juggling multiple logins and annual statements, you receive one clear overview of your preserved pension assets. This makes it far easier to calculate your total wealth and predict your future income. When the time comes to draw down your funds, you only have one provider to coordinate with, ensuring a seamless experience. This focus on long-term ease is central to effective Retirement Planning Ireland, helping you transition from your working life with confidence and optimism. You don’t just gain a financial product; you gain a straightforward path to long-term security.

Comparing Retirement Bonds vs. PRSAs: Which is Right for You?

Choosing the right home for your previous pension savings is a critical decision that impacts your flexibility later in life. Whilst both the Personal Retirement Savings Account (PRSA) and the retirement bond Ireland residents use are excellent vehicles, they serve different strategic purposes. Understanding the nuances between them allows you to move from a state of confusion to one of calm competence, ensuring your money is positioned for maximum benefit.

The most fundamental difference is that a Personal Retirement Bond is a “closed” structure. It is designed strictly to hold funds from a previous occupational scheme, and you cannot add new monthly contributions to it once it is established. In contrast, a PRSA is a more flexible, open-ended account that can accept both a transfer value from an old job and ongoing regular payments from your current income. If you want to keep your “old” money completely separate from your “new” savings, the bond is often the preferred choice.

Access rules also play a significant role in this comparison. Funds in a PRB generally cannot be accessed before age 60, but there are important exceptions. You may be able to access your bond from age 50 if you have left that employment, provided the original scheme rules allowed for early retirement. This preservation of original rights is a key reason many professionals choose the bond over a PRSA, which may have different age restrictions depending on the contract type. Fee structures also vary; some PRB providers charge an annual management fee of around 0.90%, whilst others may offer charges closer to 0.40% with additional variable elements based on your fund choice.

When to Choose a Retirement Bond

You should lean toward a retirement bond Ireland structure if you wish to preserve specific early retirement rules from your original scheme. It is also a powerful option if you have a large single pot to move and want access to specialised investment funds that might not be available within the more standardised framework of a PRSA. By keeping these assets in a dedicated bond, you maintain a clear boundary between different stages of your career, which can simplify your tax planning as you approach retirement. Higher-rate taxpayers in particular may also benefit from pairing this strategy with the Employment Investment Incentive Scheme Ireland offers, which can deliver up to 50% income tax relief on qualifying investments alongside your pension planning.

When a PRSA Might Be Better

A PRSA might be the better fit if you prefer the simplicity of having just one account where you can also add your own monthly contributions. This is particularly useful for those who want a “one-stop-shop” for their retirement savings. Many people also prefer the standardised fee structure of a Standard PRSA, which has capped charges. If you are looking for a more flexible, ongoing contribution model, you might find our PRSA Ireland guide helpful for comparing these features in more detail.

Deciding between these two paths requires a careful look at your long-term timeline and your desire for investment variety. If you’re ready to take the next step in securing your future, request a personalised pension comparison to see which structure aligns best with your goals.

How to Organise Your Retirement Bond with Engage Financial Solutions

Taking the final step toward consolidating your pension savings should feel like a relief rather than a chore. At Engage Financial Solutions, we act as the buffer between you and the complexities of the financial world, ensuring your transition to a retirement bond Ireland is handled with calm competence. Our process is designed to remove the friction often associated with old employer schemes, allowing you to move from a state of fragmentation to one of total clarity. We begin by looking at your desired end-state, whether that is early retirement or simply long-term family security, and work backward to ensure your current assets are positioned to meet those goals.

Our meticulous review process accounts for the very latest 2026 regulations, including the €2.2 million Standard Fund Threshold and the ongoing transition toward the Total Contributions Approach for the State Pension. We don’t just look at numbers; we look at how your old pension pots fit into your overall lifestyle aspirations. Dealing with former employers and scheme trustees can be a paper-heavy and stressful experience, but we manage those communications on your behalf. This proactive stewardship ensures that your interests are safeguarded at every stage of the transfer, keeping the process straightforward and transparent.

The Seamless Setup Process

We follow a methodical three-step progression to ensure your retirement savings are organised effectively. This logical flow prevents the feeling of being overwhelmed by technical jargon or administrative hurdles.

- Step 1: Data Gathering. You provide a Letter of Authority, which allows us to communicate directly with your previous providers. We gather all the necessary data on your old pensions so you don’t have to hunt for lost policy numbers or old statements.

- Step 2: Comprehensive Comparison. We provide a clear, written comparison that weighs the benefits of leaving your funds where they are versus moving them into a personalised bond. This includes an analysis of fees, which can range from 0.40% to 0.90% depending on the provider, and current bond yields which are averaging 4.5% to 5% as of June 2026.

- Step 3: Managed Transfer. Once you are happy with the strategy, we manage the entire transfer process. We handle the signatures, the trustees, and the Revenue requirements to ensure a seamless transition of your assets into your new policy.

Why Choose an Independent Advisor?

Choosing an independent partner means you aren’t limited to the restricted product range of a single bank or insurance company. We access a wide panel of providers to find the specific retirement bond Ireland residents need for their unique risk profiles. This independence is vital for creating a tailored investment strategy that remains flexible as market conditions change. We provide ongoing support to monitor your fund’s performance, ensuring your path to retirement remains optimistic and secure. If you are ready to reclaim control and bring your scattered pensions into one manageable place, book a consultation with our retirement specialists to safeguard your future.

Take Control of Your Financial Future Today

Consolidating your pension assets is more than just an administrative task; it’s a vital step toward long-term peace of mind. By choosing a retirement bond Ireland professionals can maintain the tax-free status of their hard-earned savings whilst gaining the investment flexibility needed for a modern career. Whether you’re dealing with a single frozen pot or multiple pensions from past roles, bringing them into one manageable structure provides the clarity you need to plan with optimism.

As a firm regulated by the Central Bank of Ireland, we provide expert guidance on ARFs and PRSAs to build tailored financial roadmaps for our clients. We handle the friction of the transfer process so you can focus on your next professional chapter. It’s time to move from uncertainty to a position of calm competence regarding your pension savings.

Secure Your Retirement Pots with a Personal Retirement Bond

Your retirement savings represent your years of dedication; they deserve the highest level of stewardship to ensure a stable and prosperous future.

Frequently Asked Questions

Can I withdraw money from my Retirement Bond before I retire?

You cannot typically access funds before age 60, although you may be able to retire early from age 50 if you have left that employment and the original scheme rules permitted it. Exceptions are also made for early retirement due to serious ill health. This flexibility ensures that your retirement bond Ireland remains aligned with your health and career changes whilst safeguarding your long-term security and providing a clear path to your future.

What happens to my Retirement Bond if I move abroad?

Your bond remains in place and continues to grow tax-free even if you move abroad. It is an Irish-resident policy, so you don’t need to close it or transfer it simply because you have relocated. When you eventually reach retirement age, you can draw down the benefits whilst living overseas, though you should seek professional advice on the specific tax treatment in your new country of residence at that time.

Are there any tax implications when I transfer my pension to a PRB?

There are no immediate tax implications when you transfer your pension to a PRB as it is considered a tax-free event by the Revenue Commissioners. Your capital moves directly from the old scheme to the bond without triggering an income tax bill or a levy. Once the funds are invested, they continue to grow exempt from Capital Gains Tax and Income Tax, preserving the full value of your hard-earned savings.

Can I have more than one Retirement Bond?

You can hold multiple bonds if you have accumulated pension pots from several different previous employers. Each retirement bond Ireland provider issues is typically linked to a specific period of employment. Whilst you can maintain several individual bonds, many people choose to consolidate them with a single provider to simplify their annual administration and gain a much clearer overview of their total retirement wealth in one manageable place.

What happens to the bond if I pass away before reaching retirement age?

If you pass away before reaching retirement age, the full value of your bond is usually paid to your estate or your legal personal representatives. The funds are typically distributed as a lump sum to your dependants or named beneficiaries. This provides an essential layer of financial protection for your family, ensuring that the savings you have built up over your career are protected and passed on according to your wishes.

Do I have to buy an annuity with my Retirement Bond when I retire?

You are not required to buy an annuity, as you can often choose to transfer your funds into an Approved Retirement Fund (ARF) instead. This choice allows you to keep your capital invested whilst taking a flexible income throughout your retirement. Whether you prefer the guaranteed income of an annuity or the flexibility of an ARF depends on your individual circumstances and your desire for ongoing investment control.

Is my money safe in a Retirement Bond if the provider goes bust?

Your money is protected through strict regulation by the Central Bank of Ireland and the oversight of the Pensions Authority. Most providers are also participants in the Investor Compensation Scheme, which provides a safety net for individual clients. We only work with established, robust providers to ensure your savings are held in a secure environment that prioritises long-term stability and the peace of mind you deserve.

How much does it cost to set up a Personal Retirement Bond in Ireland?

There is usually no direct setup fee for a bond, as the costs are typically managed through an Annual Management Charge deducted from the fund value. These charges cover the administration of the policy and the professional guidance provided by your advisor. Because these structures vary between providers, we offer a comprehensive review to ensure you understand how the specific charges apply to your personalised investment strategy.

Disclaimer

Engage Financial Services LTD T/A Engage Financial Solutions is regulated by the Central Bank of Ireland CRO 764570. Director David Moore. Suite 2 First Floor, 14 -18 Main Street, Blackrock, Co Dublin A94 W0Y3