What if the biggest risk to your retirement isn’t a market dip, but the actual structure of your savings? It’s natural to feel some uncertainty about the 2026 auto-enrolment rules or worry that management fees might quietly erode your future wealth. You want to know that your hard-earned money is working effectively, protected by the best possible tax efficiencies available in the local market. This guide offers a clear, professional comparison of a PRSA vs company pension to help you decide which path offers the stability you deserve.

We’ll explore which schemes offer better tax efficiency, how to navigate the €115,000 earnings cap, and the best ways to ensure your pension remains portable as your career evolves. By the end of this article, you’ll have a straightforward understanding of how to maximise employer contributions and secure your long-term financial health with confidence. Let’s look at how you can safeguard your future with calm competence and clarity.

Key Takeaways

- Understand the fundamental differences between a portable PRSA and a structured occupational scheme to ensure your retirement plan matches your career mobility.

- Learn how the 2026 auto-enrolment changes affect your eligibility and why waiting for the new system might not be the most tax-efficient choice for your situation.

- Master the age-related contribution limits and the €115,000 earnings cap to maximise your tax relief at the 20% or 40% rate.

- Compare the nuances of a PRSA vs company pension to identify which scheme allows for the most generous employer contributions based on the latest 2026 regulations.

- Discover how to design a tailored retirement strategy that removes friction and provides long-term stability throughout your professional life.

Understanding the Basics: PRSA and Occupational Schemes Explained

Securing your financial future shouldn’t be a source of stress. Whether you’re just starting your career or you’re a seasoned professional, choosing between a PRSA and a company pension is a vital step toward long-term stability. Both options serve the same fundamental purpose: they allow you to build a tax-efficient fund that will support you once you decide to step back from the workforce. In the current market, most savers are moving toward Defined Contribution structures. This means the final value of your retirement pot isn’t fixed; instead, it depends on the amount you contribute and how your chosen investments perform over time.

The local pension system is designed to be inclusive, offering different paths depending on your employment status and personal goals. When comparing a PRSA vs company pension, the best choice often comes down to how much control you want over your account and whether your employer offers a matching contribution scheme. Both vehicles provide excellent tax relief at your marginal rate, meaning every contribution you make effectively costs you less while building a more substantial future for your older self.

What is a PRSA?

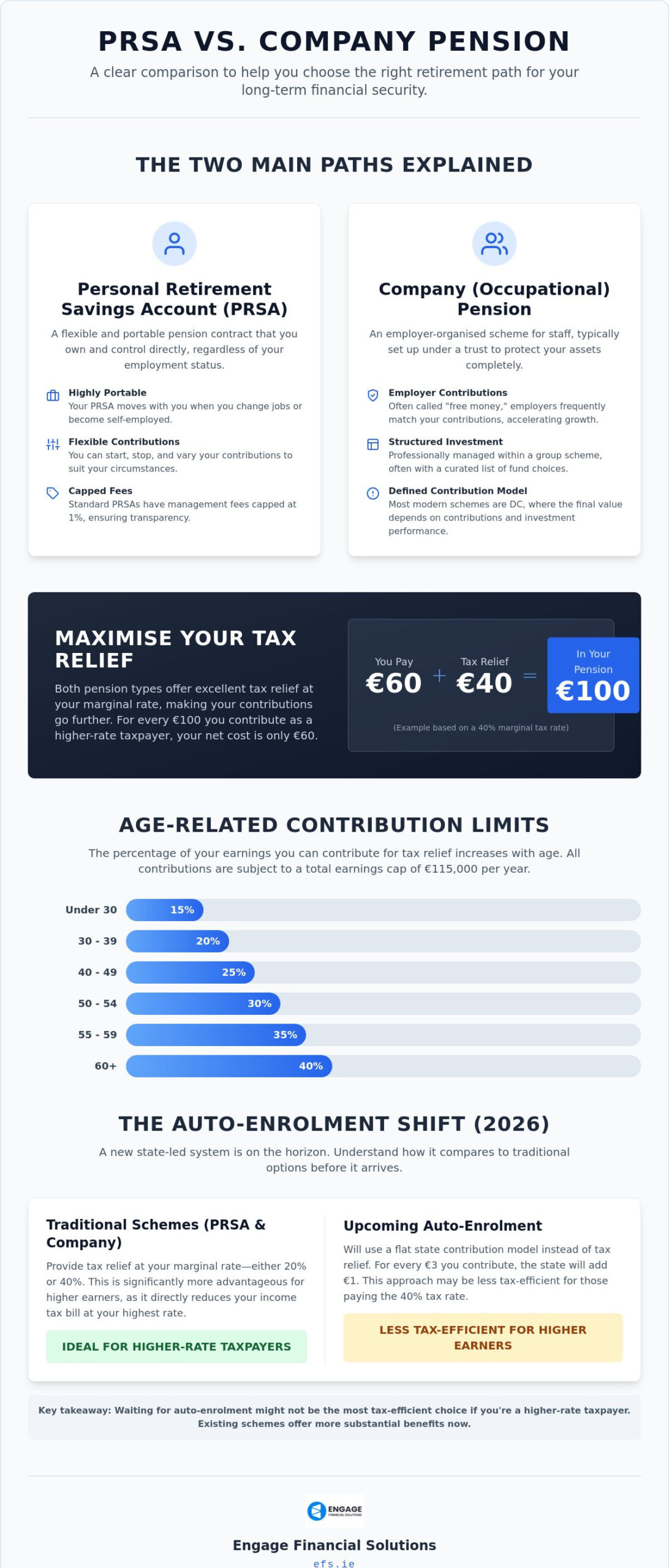

A Personal Retirement Savings Account (PRSA) is a flexible, portable contract between you and a pension provider. It’s an excellent solution for anyone, regardless of whether you’re an employee, self-employed, or currently between jobs. There are two main types to consider. Standard PRSAs have capped management fees of 1% and are generally more straightforward. Non-Standard PRSAs might offer a broader range of investment funds but often come with different fee structures. The standout feature of a PRSA is its portability. If you change employers or move into the gig economy, your account stays with you. It’s a seamless way to maintain a consistent savings habit without the friction of opening a new scheme every time your career takes a new turn.

The Role of the Company Pension

Occupational or company pensions are schemes organised by an employer for the benefit of their staff. These are typically set up under a trust, which ensures that your retirement assets are kept entirely separate from the company’s finances. Most modern workplaces have moved away from traditional Defined Benefit schemes, which promised a specific income based on your final salary. Instead, they favour the Defined Contribution model. This setup is highly collaborative; you contribute a portion of your salary, and your employer often matches that contribution or adds a set percentage. This “free money” from your employer is a significant advantage when weighing up a PRSA vs company pension. It’s a proactive way to accelerate the growth of your fund while enjoying the peace of mind that comes from a professionally managed group scheme.

The Impact of Auto-Enrolment and Modern Regulatory Changes

The local retirement market is undergoing its most significant transformation in decades. By early 2026, the introduction of the “MyFutureFund” auto-enrolment system will fundamentally change how employees save. While this initiative aims to capture those without any coverage, it’s vital to understand that a “one size fits all” approach might not serve your specific financial goals. When weighing up PRSA vs company pension Ireland, the immediate arrival of auto-enrolment shouldn’t necessarily mean you should wait.

One of the most critical distinctions lies in tax efficiency. Traditional Occupational pension schemes and PRSAs allow for tax relief at your marginal rate, which is either 20% or 40%. For a higher-rate taxpayer, this means a €100 contribution only costs €60. In contrast, the auto-enrolment system uses a flat state contribution model. If you’re a high earner, opting for a traditional structure usually provides a much more robust financial advantage than the new state-led alternative.

Recent Finance Act updates have also reshaped the path for company directors. Since early 2025, employer contributions to a PRSA are capped at 100% of the employee’s salary without being treated as a benefit-in-kind. This shift has made PRSAs an incredibly attractive tool for business owners seeking flexibility. If you’re managing these changes, reviewing your current pension structure can ensure you’re not missing out on these enhanced contribution limits. This comparison of PRSA vs company pension Ireland is particularly relevant for those looking to maximise corporate tax relief.

Auto-Enrolment vs. Traditional Pensions

AE is strictly for those not already participating in a qualifying scheme. To be exempt, a scheme must meet minimum contribution levels, such as a total of 3.5% of gross pay. Traditional plans often exceed these minimums, offering better long-term security. A tailored plan allows you to choose investment funds that match your risk appetite, whereas AE follows a more rigid, state-determined path.

The 2026 Retirement Landscape

The Pensions Authority now demands higher standards of transparency and governance. This has led to the rise of “Master Trusts,” where multiple employers join a single, large-scale scheme to reduce fees and improve oversight. These modern standards ensure your savings are managed with meticulous care. Whether you choose a PRSA or a group scheme, you can expect a level of professional stewardship that was less common a decade ago.

Side-by-Side Comparison: Tax Relief, Contributions, and Flexibility

When you look at the nuts and bolts of your retirement plan, the decision often hinges on how much flexibility you need. A PRSA is essentially your personal property; it follows you from one job to the next without any paperwork hurdles. In contrast, funds in Occupational pension schemes are tied to your current employer. If you value having a single, consolidated pot that you control regardless of where you work, the PRSA offers a level of seamlessness that is hard to beat. However, company schemes often provide lower management fees because they benefit from group buying power.

Investment control is another area where the two paths diverge. With a personal account, you typically have a wider menu of funds to choose from, allowing you to tailor your strategy to your specific risk tolerance. Company schemes might offer a more limited selection, but these are often carefully curated by professional trustees. Deciding on a PRSA vs company pension Ireland involves weighing this personal control against the convenience of a managed group environment. It’s about finding the balance that makes you feel most secure about your long-term trajectory.

Maximising Your Tax Efficiency

Tax relief is essentially a reward from the government for being proactive about your future. Locally, you can claim relief at your highest tax rate, which means for every €100 you save, it might only cost you €60 from your take-home pay. This relief is subject to age-related limits, starting at 15% of your earnings if you’re under 30 and rising to 40% once you reach age 60. There is an annual earnings cap of €115,000 that applies to these personal contributions. If you’re unsure which limit applies to you, speaking with an advisor can clarify your position and ensure you’re not overpaying tax.

Employer Contributions and Matching

One of the biggest draws of a company scheme is the “matching” contribution. Many employers will put in €1 for every €1 you contribute, which is an immediate 100% return on your investment before it’s even touched the market. Since January 2025, the rules for PRSAs have become much more generous, allowing companies to contribute up to 100% of an employee’s salary without it being taxed as a benefit-in-kind (BIK). This removes a significant barrier for those comparing a PRSA vs company pension Ireland and makes personal accounts a powerful tool for high-earning professionals and directors alike. These contributions are treated as a business expense for the company, providing a straightforward way to build your wealth while managing corporate tax liabilities.

Identifying the Best Fit for Your Career Stage and Employment Status

Choosing the right path for your future depends entirely on your current professional landscape. It’s helpful to start with your desired end-state; perhaps that’s a comfortable lifestyle by age 60 or the freedom to consult part-time. Working backward from that goal allows you to see which vehicle provides the most efficient engine for your savings. When comparing a PRSA vs company pension Ireland, your employment status is the primary compass. Whether you are climbing the corporate ladder or building a business from the ground up, the structure of your retirement plan should offer both protection and progress.

Many professionals find themselves with “pension silos”—multiple small pots of money left behind at previous jobs. These fragmented accounts can be difficult to track and may carry higher fees than a modern, consolidated arrangement. Moving these funds into a single, portable PRSA can remove the friction of managing several providers. It provides a clear, big-picture view of your total wealth, ensuring that every euro is working toward your long-term security. This holistic integration is a hallmark of a well-managed financial life, preventing your hard-earned savings from becoming stagnant or forgotten.

For the Career-Focused Employee

If you work for a company that offers a generous matching scheme, the occupational pension is usually the most logical choice. When your employer agrees to match your contributions, they are effectively providing a guaranteed return on your investment before it even reaches the market. This “free money” is a significant advantage that shouldn’t be overlooked. To ensure your plan is truly robust, it is wise to link your contributions with Income Protection. This safeguards your ability to continue saving even if an illness or injury prevents you from working, providing a seamless safety net for your future self.

For the Self-Employed and Business Owners

For those in the gig economy or running a small business, the PRSA is often the favoured tool due to its inherent flexibility. Your income may fluctuate from month to month, and a personal account allows you to adjust your contributions without the administrative burden of a group scheme. Company directors can also leverage the 2025 rule changes to make substantial employer contributions, which can be a highly efficient way to manage corporate tax whilst building personal wealth. Viewing this through the lens of Retirement Planning ensures that your business success translates into long-term personal stability. If you are ready to streamline your strategy, book a consultation with our team to explore a tailored solution that fits your unique career trajectory.

Designing a Tailored Retirement Strategy for Long-Term Security

Building a secure future is a journey that requires a steady guide. It’s easy to feel overwhelmed by shifting regulations or the complexity of different schemes, but the goal remains simple: creating a life where you don’t have to worry about money. Your retirement strategy shouldn’t exist in a vacuum. It’s a vital part of your broader financial health, sitting alongside your mortgage and your daily savings. When you look at PRSA vs company pension Ireland, you’re really looking at how to best protect your lifestyle for the decades ahead.

If the 2026 auto-enrolment changes or the recent updates to contribution limits have left you feeling uncertain, you aren’t alone. These transitions are complex, but they also present opportunities to optimise your fund. A professional review ensures that the path you’ve chosen remains seamless and effective as your career evolves. It’s about moving from confusion to a state of calm competence, knowing that your stewardship of your wealth is on the right track. You deserve a plan that works as hard as you do, providing the stability you need to look forward with optimism.

The Value of Professional Guidance

A consultant helps you move through a logical progression: identifying your specific needs, finding the right solution, and ultimately enjoying the benefit of a secure future. This expert-led approach removes the friction from financial planning. Instead of guessing which fund is best, you receive a tailored strategy that reflects your risk appetite and retirement age. Viewing your pension as a pillar of stability allows you to focus on your career today, confident that your tomorrow is already being looked after. It’s about more than just numbers; it’s about the peace of mind that comes from a plan you can trust.

Taking the Next Step

Getting a full-stack view of your financial situation is the first step toward true peace of mind. Whether you need to consolidate old pots or want to explore the tax advantages of a PRSA vs company pension Ireland, the process is more straightforward than you might think. With the Standard Fund Threshold currently at €2.2 million, ensuring you’re within your limits whilst maximising growth is essential for high earners. Switching providers or updating your contribution levels can be handled with ease when you have the right support. Don’t let your retirement plan become an afterthought. Proactive management today leads to a secure and prosperous future.

Contact us for a tailored retirement review and let us help you navigate these changes with confidence and clarity.

Take Control of Your Retirement Journey Today

Deciding on a PRSA vs company pension Ireland doesn’t have to be a source of stress. Whether you prioritise the seamless portability of a personal account or the significant growth potential of a matching employer scheme, the most important step is choosing a path that aligns with your specific career trajectory. By understanding the 2026 regulatory shifts and the €115,000 earnings cap, you’ve already taken a vital step toward safeguarding your long-term stability.

At Engage Financial Solutions, we provide personalised, client-centric consultancy to help you navigate these complex choices. As a firm regulated by the Central Bank, we offer expert guidance on the January 2026 pension changes to ensure your transition is straightforward and tax-efficient. Our goal is to act as your steady guide, removing friction and providing the optimism that comes from true financial security.

Secure your future with a tailored retirement plan from Engage Financial Solutions

Your future self will thank you for the proactive steps you take today to ensure a life of comfort and ease.

Frequently Asked Questions

Is a PRSA better than a company pension if I change jobs frequently?

A PRSA is generally the better option for frequent job changers because it is a personal contract that stays with you regardless of your employer. Unlike an occupational scheme, which is tied to a specific company, your PRSA follows your career path; this removes the administrative stress of managing several different pots. It provides a seamless way to maintain a consistent savings habit whilst moving between roles or transitioning into self-employment.

Can I have both a PRSA and a company pension at the same time?

You can hold both accounts simultaneously, but you generally cannot claim tax relief on contributions to both for the same source of employment income. Many people use a PRSA as a vehicle for Additional Voluntary Contributions (AVCs) to supplement their main company scheme. This dual approach allows you to maximise your retirement fund whilst staying within the annual tax-free limits based on your age and the €115,000 earnings cap.

What happens to my employer contributions if I move from an occupational scheme to a PRSA?

The contributions made by your employer remain yours, but they typically stay within the original scheme’s trust until you decide to transfer them. Transferring these funds into a PRSA is often possible, though it depends on your years of service and the specific rules of the scheme. Consolidating these funds into one portable account can provide a much clearer view of your total wealth and simplify your long-term planning.

How much tax relief can I actually claim on my pension contributions this year?

You can claim tax relief at your highest rate of income tax, which will be either 20% or 40% depending on your earnings. This relief is a significant incentive that effectively reduces the “net cost” of your contribution. For example, a higher-rate taxpayer can put €100 into their fund at a cost of just €60 from their take-home pay, making it one of the most efficient ways to build future stability.

Will auto-enrolment replace the need for a PRSA or company pension in 2026?

Auto-enrolment will not replace the need for a PRSA vs company pension Ireland because it is designed as a basic entry-level system for those with no existing coverage. The “MyFutureFund” system has lower contribution ceilings and a flat state top-up rather than marginal tax relief. For most professionals, a tailored personal or company scheme remains the superior choice for achieving a specific, comfortable retirement lifestyle.

What is the maximum I can contribute to my pension without paying tax?

The maximum tax-free contribution is limited by your age and an annual earnings cap of €115,000. If you are aged 40 to 49, for instance, you can claim relief on contributions up to 25% of your earnings. It is also vital to keep an eye on the Standard Fund Threshold, which is €2.2 million as of 2026; exceeding this lifetime limit can result in a significant tax charge when you eventually draw down your benefits.

How do the management fees compare between a PRSA and an occupational scheme?

Standard PRSAs have a transparent fee structure with an annual management charge capped at 1% and no entry charges. Occupational schemes may offer lower fees if they are part of a large group “Master Trust” that benefits from economies of scale. When weighing up PRSA vs company pension Ireland, you should always ask for a breakdown of all costs to ensure high fees aren’t quietly eroding your potential investment growth.

What happens to my pension fund if I decide to retire early?

You can typically access your occupational pension from age 50 if you are leaving that employment, whilst PRSA funds are generally accessible from age 60. Retiring early usually means your fund has had less time to benefit from compound growth, which may result in a lower monthly income. It is a decision that requires careful stewardship and a professional review to ensure your savings can provide the lifelong security you need.

Disclaimer

Engage Financial Services LTD T/A Engage Financial Solutions is regulated by the Central Bank of Ireland CRO 764570. Director David Moore. Suite 2 First Floor, 14 -18 Main street, Blackrock, Co Dublin A94 W0Y3