What would happen to your family’s security if your monthly salary suddenly stopped due to an unexpected illness or injury? It’s a daunting thought that many of us push to the back of our minds, especially when trying to understand the nuances of income protection Ireland. You want to know that your home is safe and your lifestyle is maintained, yet it’s easy to feel overwhelmed by the perceived high cost of premiums or the complexity of financial planning. We understand that you’re looking for stability and peace of mind, not a high-pressure sales pitch.

This guide will show you how to secure your financial future and maintain your lifestyle with a tailored plan that replaces your salary if you’re unable to work. By exploring the practicalities of income protection Ireland, you’ll gain a clear understanding of how these policies function locally, including how to claim tax relief at your marginal rate to make your cover more affordable. We’ll preview the journey from setting up a policy to receiving payments, ensuring your long-term stability is never left to chance.

Key Takeaways

- Understand how income protection Ireland provides a robust long-term safety net for your earning power, offering security that standard life insurance cannot match.

- Learn how to customise your waiting period to align with your existing employer benefits, which is a key way to manage the monthly cost of income protection Ireland.

- Discover why “own occupation” definitions are the gold standard for ensuring your policy pays out if you’re unable to perform your specific job.

- Explore the straightforward process of claiming tax relief at your marginal rate to lower the effective cost of your cover by up to 40%.

- See how an independent consultant can help you compare multiple providers to find a flexible solution that protects your family’s future.

What is Salary Protection and Why Does it Matter Locally?

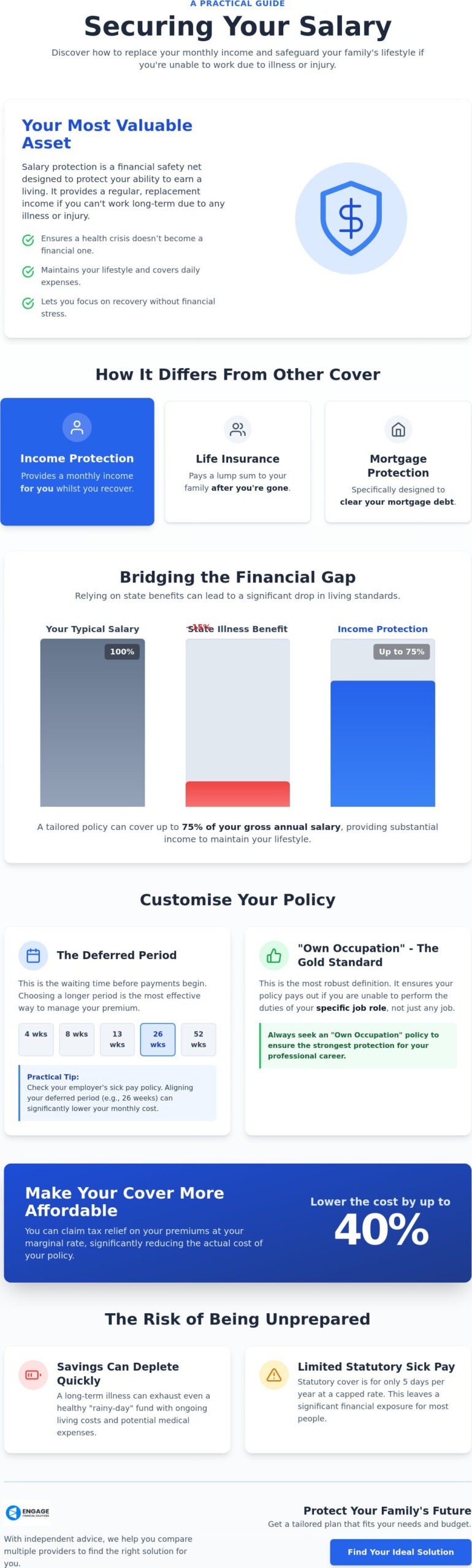

Your most valuable asset isn’t the house you’ve worked hard to buy or the car parked in the driveway. It’s your ability to get up every morning and earn a living. If an illness or injury suddenly took that away, the financial foundation of your life could shift overnight. This is why income protection Ireland is regarded as a long-term safety net, designed to safeguard your lifestyle by providing a steady stream of revenue when you’re physically unable to work. It’s about ensuring that a health crisis doesn’t become a financial one.

Many people confuse this cover with life insurance or mortgage protection, but the purposes are quite different. Life insurance provides for your family after you’re gone, and mortgage protection is designed specifically to clear a debt with a bank. In contrast, income protection Ireland is for you. It puts money directly into your pocket, allowing you to meet your daily expenses, pay your bills, and keep your family’s plans on track while you focus on recovery. To understand the basics, looking at What is Income Protection provides a helpful overview of how these policies are structured globally and within the domestic market.

The gap between what you earn and what the state provides can be startling. If you’re used to a professional salary, relying on the State Illness Benefit often leads to a significant drop in living standards. Most people find that the public safety net barely covers the basics, let alone a mortgage or childcare costs. A tailored plan bridges this gap, providing a level of security that the public system isn’t designed to offer.

The Core Mechanism of Safeguarding Your Earnings

A typical policy allows you to cover up to 75% of your gross annual salary, including any state benefits you might receive. This ensures you have a substantial portion of your normal earnings to rely on. The cover is flexible; it stays with you until you’re fit enough to return to your career or until you reach your chosen retirement age, which is often aligned with the state pension age of 66. Essentially, the benefit serves as a tax-efficient replacement of your monthly paycheque that maintains your financial independence during difficult times.

Why Relying on Savings or Sick Pay Can Be Risky

You might think your savings will see you through, but the “burn rate” of personal cash during a health crisis is often faster than anticipated. Medical costs, specialised treatments, and daily living expenses quickly deplete even a healthy rainy-day fund. Relying on employer sick pay is also a gamble for many in the private sector. Legally, employers are only required to provide five days of statutory sick pay per year, paid at 70% of your normal wages up to a maximum of €110 per day. Once those few days are gone, the financial pressure starts to mount. Removing this uncertainty allows you to focus entirely on your physical rehabilitation without the crushing weight of unpaid bills.

How Does a Protection Plan Actually Work in Practice?

Setting up a policy is a methodical process designed to give you total clarity and confidence. It begins with a straightforward assessment of your health and lifestyle, a phase known as medical underwriting. This step is vital because it ensures your contract is solid and tailored to your specific history, meaning there are no surprises if you ever need to claim. Once your policy is live, you’re protected against the financial fallout of being unable to work due to any illness or injury. A standout feature of these plans is the “waiver of premium” benefit. This ensures that if you ever need to make a claim, you won’t have to keep paying your monthly premiums whilst you’re receiving your replacement salary. It’s a proactive way to remove financial friction when you’re focusing on getting better.

Understanding the Deferred Period and Your Timeline

The deferred period is the waiting time between your last day of work and when your benefit payments begin. In our local market, you can typically choose between 4, 8, 13, 26, or 52 weeks. This choice is the most effective way to manage the cost of your income protection Ireland plan. A practical tip is to check your employment contract for any existing sick pay entitlements. If your company pays your full salary for 13 weeks, it makes sense to set your policy to start at week 13. Choosing a longer waiting period, such as 26 or 52 weeks, can significantly lower your monthly premium, making high-quality cover accessible for various budgets. Selecting the right income protection Ireland strategy depends entirely on how long you could comfortably manage on your own resources.

The Claims Process and Rehabilitation Support

When you need to claim, the experience is designed to be as supportive and stress-free as possible. Payments are made directly to you every month, mimicking the rhythm of your regular salary. This consistent flow of funds helps you maintain your mortgage payments and household bills without any interruption to your lifestyle. Most providers also offer proactive rehabilitation support, such as physiotherapy or mental health counselling, to help you return to health at your own pace. If you’re ready to go back to work but can only manage part-time hours initially, a “proportionate benefit” can bridge the gap between your reduced earnings and your full potential. This ensures your transition back to professional life is gradual and financially supported. If you’re unsure which timeline suits your career path, you can speak with a specialist to map out a tailored strategy.

Your private cover is designed to work alongside the state illness benefit to ensure your total income reaches the maximum allowable threshold. This integrated approach provides a robust shield for your family’s future, ensuring that your long-term goals remain achievable even if your health takes an unexpected turn.

Selecting the Best Policy for Your Unique Circumstances

Finding the right cover isn’t just about the monthly cost; it’s about ensuring the plan fits the life you’ve built. Insurers look at several factors to determine your premium, including your age, current health status, and the specific nature of your daily work. Generally, the younger and healthier you are when you start, the more cost-effective your cover will be. To get a sense of the broader regulatory landscape and consumer rights, the CCPC guide to income protection insurance provides a solid foundation for comparing different policy types and understanding your protections as a consumer.

How Job Classes Influence Your Monthly Premium

Local insurers use four standard risk categories, known as job classes, to calculate premiums. Class 1 includes professional and administrative roles like teachers, accountants, or solicitors, who primarily work in an office setting. Class 2 might cover sales representatives who travel frequently, whilst Class 3 and 4 are reserved for skilled manual workers and heavy manual roles, such as electricians or builders. Precision matters when you’re applying. If you’re a foreman who spends 80% of your time in an office and only 20% on-site, you should ensure this is clearly stated. Accurately describing your duties ensures your income protection Ireland strategy is fairly priced and reflects your actual daily risks.

Essential Features to Look for in a Comprehensive Plan

One of the most critical decisions you’ll make is choosing between “own occupation” and “any occupation” definitions. An “own occupation” policy is the gold standard; it pays out if you’re unable to perform the specific duties of your current job. In contrast, “any occupation” cover only pays if you’re unable to work in any role suited to your experience, which is far less protective. You should also look for “guaranteed” premiums rather than “reviewable” ones. Guaranteed premiums stay the same for the life of the policy, providing long-term financial certainty. Reviewable premiums might start lower, but the insurer can increase them later, often when you’re older and less likely to switch.

Protecting against the rising cost of living is another vital consideration. Adding “escalation in claim” ensures that if you’re out of work for several years, your monthly benefit increases annually to keep pace with inflation. This is especially important given that the average claim in the domestic market lasts approximately seven years. A modern income protection Ireland plan should also include a terminal illness benefit as standard, providing a lump sum payment if you’re diagnosed with a condition that has a limited life expectancy. This integrated approach ensures your safety net is truly comprehensive and ready for any eventuality.

Maximising Your Benefits and Managing the Cost

One of the most compelling reasons to prioritise income protection Ireland is the generous tax treatment available for these policies. Unlike many other forms of insurance, the authorities actively encourage you to protect your salary by offering relief at your marginal rate of income tax. This means that if you’re a higher-rate taxpayer, you can effectively reclaim 40% of your premium costs. It’s a significant saving that makes high-quality cover much more accessible than it might first appear. By leveraging these incentives, you’re not just buying insurance; you’re making a smart, tax-efficient investment in your long-term stability.

How Tax Relief Drastically Reduces the Net Cost

Think of it this way: for every €100 you spend on your monthly premium, the actual cost to your pocket could be as little as €60. You can choose to claim this relief through your annual tax return via the Revenue Commissioners’ “myAccount” service or, in many cases, have it processed directly through your employer’s payroll. This immediate reduction in cost is a unique feature of permanent health insurance that you won’t find with standard life or mortgage cover. For company directors, the benefits are even more pronounced. When the company pays the premiums, the effective tax relief can reach up to 52%, providing a highly efficient way to safeguard your personal financial future through the business.

Tailoring Protection for the Self-Employed

If you work for yourself, the stakes are arguably higher. Without a human resources department or a corporate sick pay scheme to lean on, your revenue often stops the moment you’re unable to work. This is why income protection for the self-employed is often seen as a vital business continuity tool rather than just a personal expense. It ensures that your mortgage and household bills stay current, allowing you to keep your business interests afloat whilst you focus on getting back on your feet. Even with recent changes allowing self-employed individuals to access some state benefits, the weekly amount is rarely enough to maintain a professional lifestyle.

Managing the cost doesn’t mean you have to compromise on the quality of your safety net. You can keep premiums affordable by carefully selecting your deferred period or by opting for a level of cover that matches your essential outgoings rather than your full gross salary. It’s also worth noting that non-smokers often enjoy lower rates, rewarding a healthy lifestyle with more competitive premiums. If you’re ready to see how these tax savings apply to your specific salary, you can request a personalised quote to see the net cost for yourself. This proactive approach to financial stewardship ensures that your protection remains a sustainable and seamless part of your monthly budget.

Finding Your Ideal Solution with Professional Guidance

Choosing how to set up your cover is just as important as the policy itself. You could go directly to a single insurer, but this often limits your view to one brand’s specific products and pricing structures. In contrast, partnering with an independent financial consultancy provides a holistic perspective of the domestic market. This approach brings a sense of calm competence to a process that can otherwise feel complex or daunting. An expert advisor acts as your steward, navigating the various providers to find the most flexible and cost-effective income protection Ireland solution for your specific career path.

The relationship with a financial guide isn’t just a one-off transaction; it’s a long-term partnership focused on your ongoing stability. As your life changes—perhaps through a promotion, a new home, or starting a family—your protection needs will evolve too. Having a trusted advisor who understands your “big picture” aspirations ensures that your safety net remains robust and relevant. They act as the buffer between you and the complexities of the financial world, making sure your journey toward long-term security is as smooth as possible.

Why an Independent Review is Crucial

An independent review is about more than just finding a low premium; it’s about the quality of the contract and the reliability of the provider. Different insurers have varying definitions of what constitutes a “valid claim,” and a professional can spot the fine print that might affect you years down the line. By comparing the whole market, a broker ensures you aren’t overpaying for features you don’t need or, conversely, missing out on vital protections like specific “own occupation” definitions. For a deeper look at how different providers stack up in the current landscape, you can read our best income protection policy comparison to see which features align with your personal goals.

Taking the Next Step Towards Financial Peace of Mind

Moving from uncertainty to security is a straightforward journey when you have the right support. Before your first consultation, it’s helpful to have a few items ready to ensure the advice is as tailored as possible:

- Your most recent payslip to confirm your gross earnings.

- Details of any existing work-related sick pay or pension benefits.

- A brief overview of your health history and any past medical records.

- An idea of your monthly essential outgoings.

At Engage Financial Solutions, we pride ourselves on a seamless onboarding process that removes the friction from financial planning. We handle the paperwork and the communication with insurers, allowing you to focus on your daily life whilst we build your safety net. Securing your income protection Ireland strategy is an act of proactive stewardship for your family. It’s about working backward from your desired future—one of stability and success—to take the necessary actions today. Take control of your financial health and enjoy the lasting peace of mind that comes from knowing you’re looked after, no matter what happens.

Securing Your Financial Resilience for the Years Ahead

You’ve explored how a tailored safety net can replace up to 75% of your earnings, ensuring that an unexpected health setback doesn’t derail your family’s future. By taking advantage of tax relief at your marginal rate, you can significantly reduce the net cost of your plan, making high-quality cover a sustainable part of your monthly budget. Whether you’re an employee or self-employed, aligning your waiting period with your existing benefits is the smartest way to manage your income protection Ireland strategy without sacrificing security.

Choosing the right policy is about more than just the numbers; it’s about the partnership and peace of mind that comes from expert stewardship. As a firm regulated by the Central Bank, we provide access to a wide panel of leading insurers and offer expert guidance tailored to your specific career path. Secure your future with a tailored consultation from Engage Financial Solutions. Taking this simple step today ensures that your lifestyle remains protected, allowing you to move forward with confidence and optimism.

Common Questions About Protecting Your Salary

Is income protection the same as serious illness cover?

No, these two types of insurance serve very different purposes in your financial plan. Serious illness cover pays out a one-off tax-free lump sum if you’re diagnosed with a specific condition listed in your policy, such as a heart attack or stroke. In contrast, income protection provides a regular monthly replacement salary for any illness or injury that prevents you from working, offering a long-term solution for your daily living costs.

How much of my salary can I actually protect?

You can generally protect up to 75% of your gross annual earnings, though this figure includes any state benefits you’re entitled to receive. This limit is designed to provide you with enough funds to maintain your lifestyle whilst ensuring there’s a financial incentive to return to work when you’re healthy. It’s a vital component of an income protection Ireland strategy to calculate this accurately so your family’s essential outgoings are fully covered.

Can I claim tax relief on my monthly premiums?

Yes, you can claim tax relief on your premiums at your marginal rate of income tax, which is either 20% or 40%. This relief is capped at 10% of your total annual income and can be claimed through the Revenue Commissioners’ online service under the “Permanent Health Insurance” section. This incentive makes the net cost of your security far more affordable than other types of insurance that don’t offer similar tax breaks.

What happens if I change jobs or become self-employed?

Your policy is personal to you, meaning it stays in force even if you move to a different employer or start your own business. You don’t lose your cover during career transitions, which provides a continuous safety net throughout your professional life. You should inform your advisor of any significant changes in your duties or salary to ensure your job class and benefit levels remain perfectly tailored to your new circumstances.

Is there a limit to how long I can receive payments?

Payments continue for as long as you meet the medical definition of being unable to work, potentially lasting until your chosen retirement age. Most people align this with the state pension age of 66, but some policies can extend to age 70. There’s no fixed maximum payout period; if you’re unable to work for several years, the policy will continue to support you monthly until you’re fit to return.

Does the policy cover mental health issues or stress-related illnesses?

Yes, modern policies typically cover mental health conditions such as stress, anxiety, and depression, provided they are severe enough to prevent you from doing your job. These conditions are amongst the most common reasons for long-term claims in the domestic market today. Ensuring your plan uses an “own occupation” definition is the best way to guarantee you’re protected for these types of illnesses within your specific professional role.

What is a “deferred period” and how do I choose the right one?

The deferred period is the waiting time between your first day of illness and when your insurance payments begin, with options usually ranging from 4 to 52 weeks. To choose the right one, you should check your employment contract for any existing sick pay benefits. If your employer pays your salary for six months, selecting a 26-week deferred period will lower your income protection Ireland premiums whilst ensuring your cover starts exactly when your employer’s support ends.

Can I have an income protection policy if I already have a pre-existing condition?

Yes, it’s often possible to obtain cover even with a pre-existing condition, though the insurer may apply a specific exclusion or an increased premium. Each application goes through a process called medical underwriting where your health history is assessed individually. Don’t assume you’re ineligible; a professional advisor can help you navigate the market to find a provider that offers the most inclusive terms for your specific health profile.

Disclaimer

Engage Financial Services LTD T/A Engage Financial Solutions is regulated by the Central Bank of Ireland CRO 764570. Director David Moore. Suite 2 First Floor, 14 -18 Main Street, Blackrock, Co Dublin A94 W0Y3