Did you know that most financial experts recommend budgeting an additional 2% to 5% of your property’s purchase price just to cover the fees that arise after you’ve saved your deposit? While reaching that 10% savings milestone is a significant achievement, the reality of closing costs for first time home buyer Ireland often creates a sense of uncertainty at the final hurdle. It’s natural to feel concerned about being short on cash or confused by terms like conveyancing and land registry fees. You’ve worked incredibly hard to reach this point, and you deserve a transition that feels secure, predictable, and managed with professional care.

We believe that your journey to owning a home should be defined by optimism rather than stress. This guide is designed to provide the clarity you need by demystifying every hidden fee and mandatory expense required to secure your property in 2026. You’ll find a definitive checklist of costs, a professional timeline of when specific fees must be paid, and the reassurance that you’re financially prepared for what’s ahead. Our goal is to ensure your move is as seamless as possible, allowing you to focus on the excitement of your new beginning.

Key Takeaways

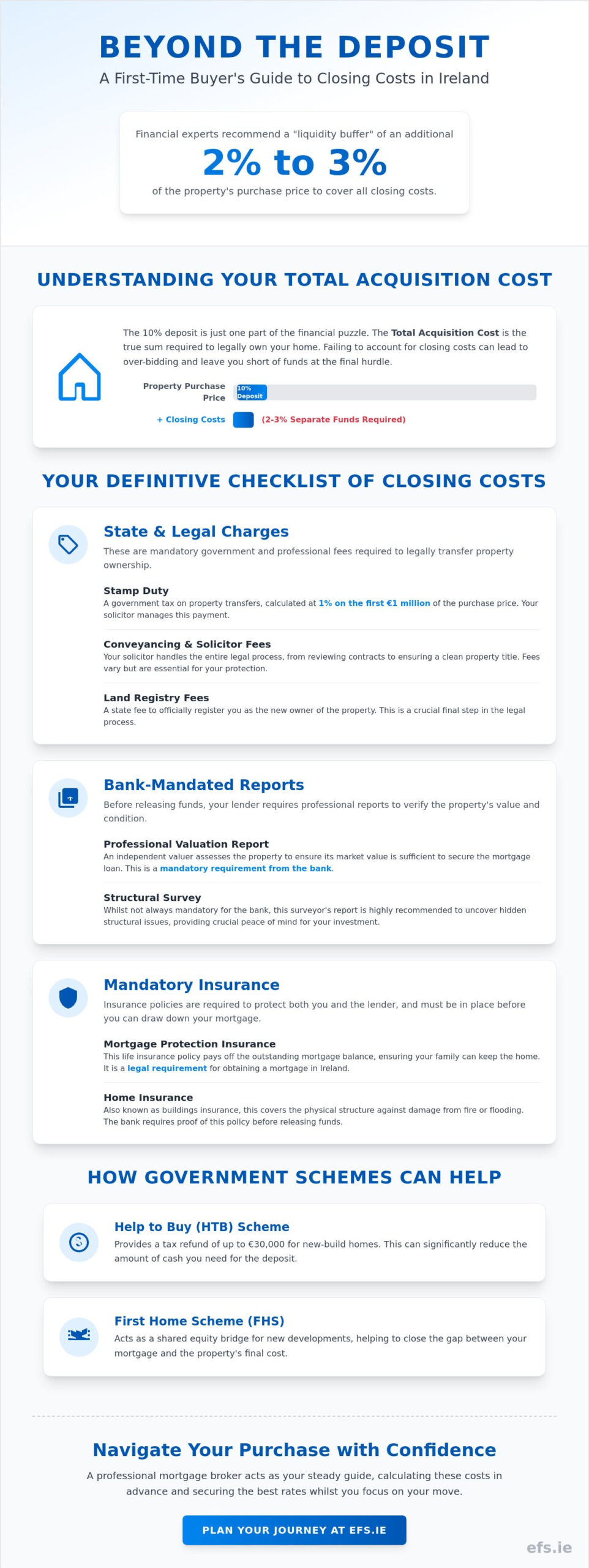

- Learn why maintaining a liquidity buffer of 2% to 3% of the purchase price is essential to cover the full spectrum of closing costs for first time home buyer Ireland.

- Understand the breakdown of mandatory state charges, including the 1% Stamp Duty rate and the vital role your solicitor plays in the conveyancing process.

- Discover the bank-mandated requirements you must satisfy before drawdown, from professional valuation reports to the security provided by a structural survey.

- Identify the mandatory insurance policies, such as Mortgage Protection and Home Insurance, that safeguard your future and ensure the seamless release of your loan funds.

- See how a professional mortgage broker acts as a steady guide, navigating the complexities of the market to secure the best rates whilst you focus on your move.

Beyond the Deposit: Understanding the Real Cost of Buying in Ireland

It’s a common misconception that your deposit is the only cash you’ll need to save before you can collect your keys. In reality, closing costs for first time home buyer Ireland encompass the mandatory professional, legal, and tax fees required to transfer a property title into your name. Without these funds, the legal process cannot conclude, and the purchase will stall. Understanding these costs early ensures you aren’t caught off guard by the financial realities of the Irish property market.

We recommend maintaining a “liquidity buffer” of 2% to 3% of the property’s purchase price in a separate savings account. This fund covers everything from your solicitor’s bill to the taxman’s cut. It also provides a safety net while understanding property value fluctuations, ensuring that a slight shift in market conditions doesn’t derail your plans. Being fully budgeted before you even attend a viewing provides a level of emotional stability that makes the entire process feel straightforward and managed.

At Engage Financial Solutions, we act as your steady guide, helping you calculate these figures long before you sign a contract. This proactive planning provides immense relief, ensuring you won’t be the buyer scrambling for funds at the last minute whilst others are ready to close. Our goal is to make your transition to homeownership as seamless as possible.

The 10% Rule vs. Total Acquisition Cost

Most buyers focus entirely on the 10% deposit required by lenders, but that’s only one part of the financial equation. The Total Acquisition Cost is the comprehensive sum of the property purchase price, stamp duty, and all professional fees required to complete the legal transfer. If you bid on a home based solely on your deposit savings, you risk the common mistake of over-bidding. Failing to account for closing expenses can leave you with a signed contract but no way to pay your solicitor or the Revenue Commissioners. By calculating the total cost first, you can bid with confidence, knowing exactly what you can afford to pay at the final hurdle. Before you start bidding, it’s equally important to understand how much can I borrow first time buyer Ireland, so your budget is grounded in your actual lending capacity.

How Government Schemes Impact Your Cash Flow

Government supports can significantly alter your cash flow and reduce the immediate pressure on your savings. The Help to Buy (HTB) scheme is a vital tool that often assists with the deposit requirements for new-build homes by providing a tax refund of up to €30,000. Similarly, the First Home Scheme (FHS) serves as a shared equity bridge specifically for new developments, helping you close the gap between your mortgage and the property’s cost. These schemes are designed to make entry into the market more accessible, but they require careful integration into your overall budget. To understand how to apply these incentives to your specific situation, see our First Time Buyer Mortgage Ireland: The Comprehensive 2026 Guide.

Mandatory State and Legal Charges: Stamp Duty and Conveyancing

Once you’ve secured your property, the focus shifts to the legalities of ownership. These mandatory charges represent a significant portion of the closing costs for first time home buyer Ireland. The most substantial of these is Stamp Duty, a government tax on the transfer of property. In Ireland, residential properties attract a Stamp Duty rate of 1% on the first €1 million of the purchase price. Whilst this sounds straightforward, the timing and calculation can vary depending on the type of home you’re purchasing. Your solicitor will manage this payment to the Revenue Commissioners as part of the conveyancing process, which is the formal legal transfer of the property title from the seller to you.

Choosing a solicitor early in your journey is a proactive step that ensures a seamless transition from bidder to owner. A steady legal partner doesn’t just push paper; they protect your interests by investigating the property’s history and ensuring there are no hidden legal encumbrances. For a more detailed breakdown, the Citizens Information Board provides a comprehensive guide to home-buying costs that complements our professional advice.

Calculating Stamp Duty for New Builds vs. Second-Hand Homes

The calculation of Stamp Duty differs slightly depending on whether you’re buying a brand-new home or a second-hand property. For new builds, the tax is calculated on the base price of the house excluding VAT, which is currently 13.5%. Conversely, if you purchase a second-hand home, the 1% tax applies to the full purchase price. For example, on a standard €350,000 second-hand property, you must budget exactly €3,500 for Stamp Duty. Understanding this distinction prevents you from over-allocating funds and ensures your liquidity buffer remains intact for other essential expenses.

Solicitor Fees and Land Registry Outlays

Legal costs typically fall into two categories: the solicitor’s professional fee and “outlays”. Professional fees can be a flat rate, often ranging between €1,500 and €3,000, or a percentage of the property value. It’s important to remember that 23% VAT applies to this professional fee portion. Outlays are payments your solicitor makes to third parties on your behalf. These include Land Registry fees, which can range from €400 to €800 depending on the property value; Commissioner for Oaths fees; and various search fees to verify the property’s legal standing. By accounting for these early, you can move forward with the confidence that your budget is robust. If you’re ready to start your journey, our team at Engage Financial Solutions can help you align your mortgage strategy with these legal realities.

Bank-Mandated Requirements and Property Due Diligence

Beyond the legal transfer of the property title, your lender requires specific checks to ensure the house is a sound investment. These professional assessments form another layer of the closing costs for first time home buyer Ireland. While some of these requirements are strictly for the bank’s benefit, others serve as your primary protection against future financial shocks. Gaining clarity on these steps is vital for understanding mortgage costs and ensuring your budget remains intact during the final weeks of the purchase.

Most of these fees are paid directly to the professionals at the time of service, rather than being settled at the very end of the process. This is why having your liquidity buffer ready early is so important. A professional mortgage broker can help coordinate these moving parts, keeping the process straightforward and ensuring you meet the bank’s deadlines without unnecessary stress. By managing these requirements proactively, you maintain the momentum needed to reach drawdown smoothly.

The Mortgage Valuation Report

Before an Irish lender issues a formal loan offer, they must confirm that the property’s market value supports the amount you’re borrowing. The bank will typically select a valuer from their own pre-approved panel, but as the borrower, you are responsible for the cost of the report. It’s important to understand that this valuation is strictly for the bank’s security; it confirms the price but doesn’t provide detail on the property’s physical condition. You should also remember that valuations have a limited shelf life, usually between four and six months. If your closing process is delayed, you might need to pay for a refreshed report to keep your loan offer valid.

Independent Structural Surveys

Whilst a valuation tells the bank what the house is worth, a structural survey tells you if the house is actually sound. For second-hand homes, this is an essential step that you should never skip. An independent surveyor will look for significant issues that could cost thousands to repair, such as dampness, subsidence, or specific material concerns like pyrite and mica. These issues are unfortunately common in certain Irish properties and can significantly impact your ability to insure or resell the home in the future. Investing in a survey provides the professional reassurance that your first home won’t become a financial burden, allowing you to move forward with optimism and security.

The Final Stretch: Insurance, Taxes, and Moving Logistics

The final weeks before you receive your keys are often the most active. Whilst you’ve already accounted for the heavy lifting of legal fees and stamp duty, these concluding expenses act as the essential “triggers” for your lender to release funds. Managing these final closing costs for first time home buyer Ireland requires a proactive approach to ensure that your move-in date remains on schedule. By addressing these requirements early, you can avoid the common stress of last-minute delays and focus on the excitement of your new beginning.

Mandatory Insurance: Mortgage Protection and Buildings Cover

Before any Irish bank releases mortgage funds to your solicitor, they require proof that their investment is protected. This involves two specific types of cover. Firstly, mortgage protection Ireland is a legal requirement for most borrowers; it’s a life insurance policy designed to pay off your mortgage balance if you pass away. Secondly, you must have a Home Insurance (Buildings Cover) policy in place. The lender will ask for a “letter of indemnity” from your insurer to confirm the property is adequately covered against risks like fire or storm damage.

We recommend starting your insurance applications as soon as you have a signed contract. Delays in medical underwriting for mortgage protection can sometimes take weeks, which might stall your closing date. You should also consider the difference between this mandatory cover and optional Income Protection, which provides a safety net if you’re unable to work due to illness. If you’re feeling overwhelmed by the sequence of these final steps, our team can help you organise your mortgage protection and ensure every box is ticked for a smooth drawdown.

Local Property Tax (LPT) and Utility Transitions

A often overlooked part of the closing process is the “apportionment” of Local Property Tax. Since LPT is usually paid by the seller at the start of the year, you’ll likely need to reimburse them for the portion of the year you’ll actually own the property. Your solicitor will calculate this figure and add it to your final completion statement. Alongside this tax adjustment, you’ll need to manage the logistics of moving day itself. We suggest keeping a small “rainy day” fund aside for these immediate needs:

- Utility Deposits: Some providers require a deposit or connection fee when setting up new electricity and gas accounts.

- Meter Readings: Take clear photos of all meters on the day you get the keys to ensure you aren’t billed for the previous owner’s usage.

- Broadband Setup: Installation fees for high-speed internet can range from €50 to €150 depending on the provider.

- Moving Logistics: Professional van hire or removal services typically cost between €600 and €1,500 depending on your location and the volume of furniture.

By preparing for these final details, you ensure that your first night in your new home is defined by peace of mind and comfort. This meticulous planning is what allows for a truly seamless transition into homeownership.

Navigating Your First Home Purchase with Expert Guidance

Buying a first home is a landmark life event, but the complexity of the Irish property market can often feel overwhelming. We act as a professional buffer between you and these intricacies, ensuring that your transition from renter to homeowner is defined by stability and optimism. By understanding the full spectrum of closing costs for first time home buyer Ireland, you’ve already taken a vital step toward long-term security. Our role is to provide the calm competence required to navigate the remaining hurdles, allowing you to focus on the move whilst we manage the financial architecture behind the scenes.

Why a Professional Guide Matters

We follow a methodical Need-Solution-Benefit approach to homeownership. We identify your specific financial needs, introduce expert interventions like sourcing the most competitive first-time buyer mortgage rates, and conclude with the peace of mind you experience on moving day. Having a single point of contact for your mortgage, mortgage protection, and long-term financial planning removes friction from the process. We meticulously monitor every detail, ensuring you are never surprised by a hidden fee or a missed deadline. This proactive stewardship is designed to make you feel looked after and understood throughout the entire journey.

Your Next Steps to Homeownership

With the right preparation, the keys to your first home are well within your reach. Now that you understand the mandatory outlays and the timing of payments, you can bid with the confidence of a buyer who is fully prepared. We invite you to reach out for a personalised consultation where we can map out a tailored budget specifically for your circumstances. Whether you are just beginning to save or are ready to make an offer, our team is here to provide the steady guidance you need. We believe in building a partnership that lasts long after you have moved in, supporting your life-long financial health. Contact Engage Financial Solutions today for tailored mortgage advice and take the final step toward your future with confidence.

Step into Your New Home with Absolute Clarity

Owning your first home is a landmark achievement that marks the start of a secure future. By mastering the details of closing costs for first time home buyer Ireland, you’ve transitioned from a hopeful bidder to a fully prepared homeowner. You now understand that success lies in maintaining a dedicated liquidity buffer for legal outlays and ensuring your mandatory insurance is organised well in advance. This proactive approach removes the friction often associated with the final weeks of a purchase, allowing you to focus on the joy of your new beginning.

At Engage Financial Solutions, we specialise in first-time buyer and switching mortgages. As a firm regulated by the Central Bank of Ireland, we provide the personalised guidance needed for a truly seamless property transition. We act as your steady guide, navigating the complexities of the market whilst you prepare for moving day. With the right support and meticulous budgeting, the keys to your new property are firmly within reach. We look forward to helping you build a foundation of long-term financial health and stability.

Secure your first home with expert mortgage advice from Engage Financial Solutions

Frequently Asked Questions

How much should a first-time buyer budget for closing costs in Ireland?

You should aim to budget between 2% and 5% of the property’s purchase price to cover all associated fees. For a home valued at €350,000, this means having a liquidity buffer of approximately €7,000 to €17,500 in addition to your 10% deposit. This fund ensures you can comfortably manage the closing costs for first time home buyer Ireland, including legal fees, stamp duty, and immediate moving expenses.

Is stamp duty different for first-time buyers in Ireland?

No, there is currently no special exemption or reduced stamp duty rate specifically for first-time buyers in the Irish market. You’ll pay the standard residential rate of 1% on the first €1 million of the property’s value. Whilst some other countries offer relief for new entrants, the Irish system applies this tax uniformly to ensure a stable and predictable revenue stream from property transfers.

When do I have to pay my solicitor when buying a house?

You typically settle the majority of your solicitor’s professional fee on the day of completion, just before the property keys are released. However, you’ll likely be asked to provide funds for “outlays” much earlier in the process. These outlays cover third-party costs like Land Registry fees and property searches that your solicitor must perform to protect your interests during the conveyancing phase.

Do I really need a structural survey for a new build home?

Whilst a full structural survey isn’t usually mandatory for a new build, it’s highly recommended to commission a professional “snag list” instead. This specialised report identifies minor defects or unfinished work that the builder is obligated to rectify before you take possession. It provides the same peace of mind as a traditional survey, ensuring your new home is delivered to the highest possible standard.

What happens if I don’t have mortgage protection insurance?

Your lender will refuse to release the mortgage funds if you don’t have a valid mortgage protection policy in place at the time of drawdown. This insurance is a legal requirement for most borrowers in Ireland, designed to pay off the mortgage balance if you pass away. Without a letter of indemnity from your insurer, the legal process will stall, and you won’t be able to complete your purchase.

Can I include closing costs in my mortgage loan?

No, you generally cannot add these expenses to your mortgage loan; they must be paid from your own cash savings. Irish lenders provide a percentage of the property’s value, but professional fees and taxes are considered separate transaction costs. This is why building a dedicated savings buffer is a vital part of your preparation, ensuring a seamless transition without the need for last-minute loans. To understand exactly what your lender will offer based on your income, our guide on how much can I borrow first time buyer Ireland provides a clear breakdown of the Central Bank’s lending limits and exemptions.

How much is the average valuation fee in 2026?

In 2026, the average valuation fee typically ranges from €150 to €300, depending on the property’s location and the lender’s specific panel requirements. This fee is paid directly to a professional valuer who confirms for the bank that the property is worth the purchase price. It’s an essential step in the loan offer process and is usually paid at the time the valuation is requested.

Are there any grants that cover closing costs for first-time buyers?

There are no government grants that specifically pay for closing costs, but schemes like Help to Buy (HTB) and the First Home Scheme (FHS) provide significant indirect support. By assisting with your deposit or providing a shared equity bridge, these initiatives free up your personal savings. This allows you to reallocate your cash toward mandatory outlays like stamp duty and legal fees, making the overall purchase more manageable.

Disclaimer

Engage Financial Services LTD T/A Engage Financial Solutions is regulated by the Central Bank of Ireland CRO 764570. Director David Moore. Suite 2 First Floor, 14 -18 Main street, Blackrock, Co Dublin A94 W0Y3