What if the legal fees you’re dreading are actually a small entry price for a five-figure return on your home? It’s understandable to feel a sense of hesitation when considering legal fees for switching mortgage Ireland, especially when you’re already managing a busy household budget. You might worry that the cost of solicitors and property valuations will swallow up any potential gains, or that the paperwork involved in moving deeds is simply too complex to handle alone.

We’re here to reassure you that a transition to a better rate can be both straightforward and incredibly rewarding. We understand that you want a partner who is one step ahead, anticipating these stresses so you don’t have to. In this comprehensive 2026 guide, you’ll discover how to manage solicitor costs and outlays whilst securing long-term stability. We’ll provide a clear breakdown of potential expenses, explain how bank cashback can neutralise your fees, and show you the path to a seamless transition that prioritises your future peace of mind.

Key Takeaways

- Understand the legal necessity of a solicitor when transferring a mortgage charge to ensure your property’s security is managed with professional care.

- Get a transparent breakdown of legal fees for switching mortgage Ireland, including essential outlays such as Land Registry fees and property valuations.

- Discover how to leverage 2026 lender cashback offers to neutralise your upfront costs and secure immediate financial relief.

- Follow a straightforward, step-by-step roadmap for instructing solicitors and moving title deeds to remove the friction from your mortgage switch.

- Recognise how tailored professional support can streamline the coordination between all parties for a more efficient and stress-free experience.

Understanding Legal Fees for Switching Mortgage in Ireland

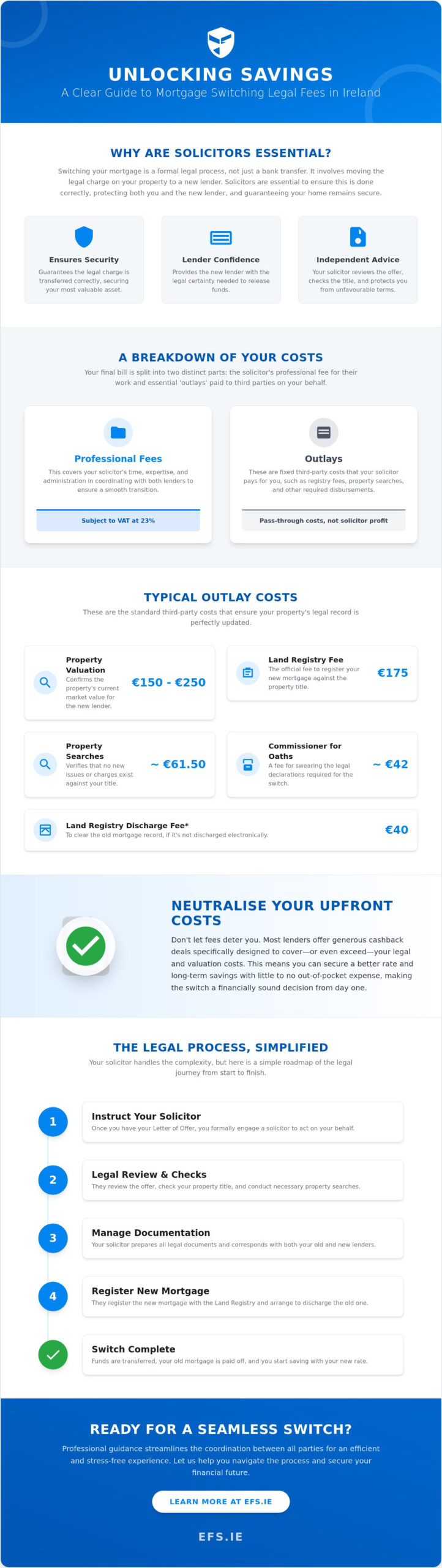

You might think of switching your mortgage as a simple bank transfer, but it’s actually a formal legal transaction. When you decide to move your home loan to a new lender, you aren’t just changing where your monthly payment goes; you’re essentially rearranging the legal charge held against your property. This is why legal fees for switching mortgage Ireland are a necessary part of the journey. While the prospect of solicitor costs might feel like a hurdle, these fees represent the professional stewardship required to ensure your most significant asset remains secure throughout the transition.

Lenders in Ireland insist on solicitor involvement to guarantee that the new mortgage is properly registered. Precision is non-negotiable. Unlike a standard property purchase, you already own the home, which removes the stress of property chains or bidding wars. However, the legal complexity remains significant because the new lender needs absolute certainty that their interest is protected. This framework is governed by Irish mortgage law, which ensures that every transfer of interest is recorded accurately and transparently. Having an expert manage this process provides a layer of reassurance that your deeds are handled with the highest level of care.

Why Lenders Require Independent Legal Advice

A solicitor does more than just manage paperwork. They act as your safeguard, meticulously reviewing the Letter of Offer to ensure you fully understand the commitment you’re making. They’ll check that the title is clean and free from any unexpected encumbrances that could cause future headaches. By providing independent advice, they protect you from unfavourable terms and ensure that the transition to your new rate is as straightforward as possible. This professional oversight is what allows the bank to release funds with confidence.

The Difference Between Professional Fees and Outlays

It helps to view your final bill in two distinct parts to avoid confusion. Professional fees cover the solicitor’s time, expertise, and the administrative burden of coordinating with two different financial institutions. Outlays, on the other hand, are third-party costs that your solicitor pays on your behalf. These include property searches and Land Registry filings. Don’t forget that professional fees are subject to VAT at the standard rate of 23%. It’s always wise to clarify whether your initial quote includes this tax so you can plan your budget with total clarity. If you’re looking for a partner to help manage these moving parts, visiting efs.ie can help you see how the entire process fits into your long-term financial health.

A Detailed Breakdown of Solicitor Costs and Outlays

Understanding the components of your final bill is the best way to remove the anxiety of hidden costs. When you’re calculating the legal fees for switching mortgage Ireland, you’ll notice the total is split between the solicitor’s time and the outlays they pay to external bodies on your behalf. Think of outlays as essential “pass-through” costs. Your solicitor doesn’t keep this money; they simply manage the payments to ensure your property’s legal record is updated correctly. By seeing these items clearly, you can plan your transition with total confidence.

Most switchers will encounter a standard set of charges that facilitate the move from one lender to another. For instance, a property valuation is a core requirement for your new bank, typically costing between €150 and €250. You’ll also need to account for property searches, which verify that no new issues have arisen with the title since you first bought the home. These searches usually cost around €61.50. Additionally, several documents must be sworn in the presence of a Commissioner for Oaths, a process that carries a modest fee of approximately €42. These small, specific steps are what create the “calm competence” of a legally sound mortgage switch.

Standard Legal Outlays to Expect

The largest outlay is almost always the Land Registry fee. As of June 2026, the fee for registering a new mortgage charge is €175. If your old mortgage isn’t discharged electronically, an additional €40 fee may apply to clear the old record. Your solicitor will also handle administrative tasks like secure deed storage and courier services. Whilst these costs are small, they’re vital for the safe transport of your title deeds between financial institutions. This meticulous attention to detail ensures that your home’s security is never in question.

Factors Influencing the Total Cost

Not every mortgage switch is identical. If your property is a leasehold rather than a freehold, the legal work can be slightly more involved, which might influence the professional fee. Similarly, if you’re choosing to release equity or “top up” your loan amount during the switch, the solicitor must perform additional checks to satisfy the lender’s requirements. Most solicitors offer fixed-fee quotes for standard switches, which provides excellent budget certainty. If you’re unsure how these costs fit into your wider financial plan, exploring your options with a specialist can help you see the bigger picture of your long-term savings.

How to Minimise and Cover Your Switching Costs

The prospect of paying out-of-pocket expenses can often feel like a barrier to financial progress. However, the 2026 Irish mortgage market is designed to reward proactive homeowners. When you’re calculating the legal fees for switching mortgage Ireland, it’s vital to view them as a strategic entry fee rather than a lost cost. Most modern lenders now offer significant incentives that don’t just cover your legal bill; they often leave you with a surplus to invest back into your home or savings.

Lenders currently use two primary cashback models to attract switchers. Some provide a flat upfront payment, which can reach up to €3,000, whilst others offer tiered amounts based on the size of the loan. Alternatively, percentage-based models can be even more lucrative for those with higher property values. For instance, a 2% cashback offer on a €300,000 mortgage results in a €6,000 payment. This lump sum is usually paid into your account within two months of drawing down your new loan, effectively neutralising your solicitor’s bill and property valuation costs in one stroke.

Whilst a large cash injection is attractive, a professional broker helps you look past the initial bonus to the long-term APRC (Annual Percentage Rate of Charge). A slightly lower interest rate often saves you far more over five years than a large upfront payment. We focus on the “net benefit” of your switch, ensuring that the move makes sense for your specific lifestyle and long-term security. The goal is a seamless transition where the savings on your monthly repayments far outweigh the initial investment in professional advice.

The Role of Cashback in Neutralising Legal Fees

Cashback serves as a powerful tool for stewardship of your finances. By timing your switch correctly, you can ensure that the bank’s incentive arrives just as your final legal bill is due. It’s a straightforward way to remove the friction of moving lenders. You should be aware, however, that some “green” mortgages or specific fixed-rate products might offer lower rates but smaller cashback amounts. We’ll help you weigh these options to ensure you aren’t sacrificing thousands in interest for the sake of a smaller upfront cheque.

Choosing the Right Solicitor for Your Switch

Efficiency is the enemy of high costs. Choosing a solicitor who specialises in conveyancing rather than a generalist often results in a faster, more cost-effective process, helping you manage the legal fees for switching mortgage Ireland with greater efficiency. These specialists are already familiar with the digital systems used by major lenders, which reduces the time spent on administrative back-and-forth. For more detailed insights on how to prepare for this move, you can read our Switching Mortgage Ireland: The 2026 Guide to Seamless Savings. Selecting a partner who understands the “big picture” of your financial health ensures that every step adds value to your future.

How to Switch Mortgage Ireland: The Legal Step-by-Step

Once you’ve secured your new mortgage approval, the focus shifts from financial planning to legal execution. This is the stage where your solicitor steps in to bridge the gap between your old lender and the new one. Whilst much of the administrative work happens in the background, knowing the exact sequence of events helps you maintain a sense of control. Your investment in legal fees for switching mortgage Ireland ensures that every document is handled with meticulous care, protecting your ownership rights throughout the entire transition.

The legal journey typically follows a logical, five-step progression designed to safeguard all parties involved:

- Step 1: Instructing your solicitor. As soon as your mortgage is approved, you’ll formally appoint your legal representative to act on your behalf.

- Step 2: Requesting title deeds. Your solicitor contacts your current lender to request your title deeds. This is a vital phase that requires professional follow-up to avoid unnecessary delays.

- Step 3: Signing the new deed. You’ll meet with your solicitor to review the new Letter of Offer and sign the mortgage deed, ensuring you’re comfortable with all terms.

- Step 4: Drawdown. The new lender releases the funds directly to your solicitor’s secure client account.

- Step 5: Registration. Your solicitor pays off the old loan, discharges the previous charge, and registers the new lender’s interest with the Land Registry.

Navigating the Deed Transfer Process

The deed request phase is often where switchers experience the most friction. Existing banks can sometimes take several weeks to release these documents, which can feel frustrating when you’re eager to start saving. We act as your proactive partner during this time, coordinating closely with your solicitor to ensure the request is prioritised. This stewardship prevents your application from stalling and maintains the “calm competence” required to move the process toward a successful conclusion.

Completion and Drawdown

The moment of drawdown is when the “seamlessness” we promise becomes a reality. Your solicitor manages the movement of funds with precision, settling the final balance with your previous lender and ensuring the transition happens on a specific, agreed-upon date. Once the old mortgage is cleared, your new, lower monthly repayments begin. It’s a straightforward conclusion to a process that sets the foundation for your long-term financial stability. If you’re ready to take the first step toward these savings, start your mortgage switch with us today and let our team manage the complexity for you.

Why Professional Guidance Makes the Transition Seamless

Imagine the peace of mind that comes from knowing your financial house is in order, not just for next month, but for the next decade. Whilst the technical details of legal fees for switching mortgage Ireland can feel overwhelming, you don’t have to navigate them alone. We act as the essential buffer between you and the complexities of the banking and legal worlds. Our role is to provide the “calm competence” you need to move from a high-interest rate to a more flexible, cost-effective solution without the usual friction.

We take stewardship of your timeline by coordinating directly with your solicitor. This proactive approach ensures that deed requests are followed up and that the “old” bank’s requirements are met promptly. By anticipating potential stresses before they occur, we allow you to focus on the outcome: a significantly reduced monthly repayment and a clearer path to financial freedom. This partnership turns a complex legal requirement into a straightforward step toward long-term security.

A Holistic Approach to Your Mortgage

Whether you’re a first-time switcher looking for immediate relief or an experienced investor managing a portfolio, your mortgage is just one piece of your financial puzzle. A change in your loan terms is the perfect time to ensure your mortgage protection is still fit for purpose. If your new loan has a different term or a lower balance, your insurance should reflect that to ensure you aren’t overpaying for cover you no longer need.

We also look at how these savings integrate with your retirement planning. Every Euro saved on interest today is a Euro that can be diverted into your pension or savings, growing your wealth for the future. By using a “future-back” perspective, we help you see that switching today is a deliberate choice to safeguard your lifestyle in the years to come. It’s about more than just a better rate; it’s about life-long financial health.

Your Next Steps to Savings

The journey to a better mortgage rate starts with a clear, honest assessment of your current situation. We provide a tailored analysis of your switching potential, helping you weigh the upfront legal costs against the long-term APRC benefits. You deserve a partner who is meticulous, attentive, and deeply invested in your individual needs. We’re here to remove the stress and replace it with a clear, actionable plan for progress. To get started on your journey, organise a consultation with Engage Financial Solutions today and discover how simple a better financial future can be.

Take the Next Step Toward Long-Term Security

You’ve seen how the right strategy can turn a complex legal requirement into a powerful financial opportunity. By understanding the breakdown of legal fees for switching mortgage Ireland, you can move forward with confidence, knowing that modern cashback offers are designed to neutralise your upfront outlays. Whether you’re seeking immediate monthly relief or a more stable foundation for your retirement, the transition is a straightforward path to significant lifetime savings. Every decision you make today builds the security you’ll enjoy tomorrow.

As a firm regulated by the Central Bank of Ireland, we specialise in mortgage switching and protection with a unique “future-back” perspective. We act as your proactive partner, managing the coordination with solicitors and lenders to ensure every detail is handled with meticulous care. You don’t have to manage the paperwork alone; we’re here to provide the steady guidance you deserve. Our expertise ensures that your transition is as smooth and efficient as possible, leaving you to enjoy the benefits of your new rate.

Start your seamless mortgage switch with Engage Financial Solutions today. Your future self will thank you for the stability and peace of mind you’ve secured.

Frequently Asked Questions

How much are the typical legal fees for switching a mortgage in Ireland in 2026?

Solicitor professional fees for a standard switch usually range between €1,000 and €1,500 including VAT. You should also budget for essential outlays like property valuations, which cost between €150 and €250, and property searches. Having a clear understanding of these legal fees for switching mortgage Ireland allows you to plan your transition with total confidence and financial clarity.

Do I need to find a new solicitor when I switch my mortgage?

You’re free to choose any solicitor you like; you aren’t obligated to use the firm that handled your original property purchase. Many homeowners opt for solicitors who specialise in conveyancing because they’re often more efficient with the digital platforms used by modern lenders. Selecting a partner who understands the “big picture” of your financial health ensures a more straightforward and professional experience.

Can I add the legal fees to my new mortgage balance?

Most lenders in Ireland require you to pay legal fees and outlays upfront rather than rolling them into your new mortgage loan. While this requires some initial cash flow, the significant cashback incentives available in 2026 are designed to reimburse these costs shortly after you draw down the funds. This strategy ensures your mortgage balance remains as low as possible whilst securing your long-term savings.

How long does the legal part of the switching process take?

The legal phase of a mortgage switch typically takes between six and eight weeks to reach completion. The most time-consuming element is often the transfer of title deeds from your old lender to your solicitor. We act as a proactive buffer during this time, coordinating with all parties to ensure the process remains on track and free from unnecessary administrative friction.

What happens to my title deeds when I switch lenders?

Your title deeds are physically and legally transferred from your current bank to your new lender’s custody. Your solicitor manages this stewardship, ensuring the old mortgage charge is formally discharged and the new lender’s interest is correctly registered. This meticulous process safeguards your ownership rights and ensures that your property’s legal record is perfectly aligned with your new financial arrangements.

Is there a fee for requesting my deeds from my current bank?

Most Irish banks charge a modest administrative fee for the release and transport of title deeds, which typically falls between €35 and €63. This is a standard third-party outlay that your solicitor will settle on your behalf during the switching process. It’s a small but vital step in the journey toward a more competitive interest rate and better monthly flexibility.

What are Land Registry outlays and why do I have to pay them?

Land Registry outlays are statutory fees paid to the Property Registration Authority to update the legal charge held against your home. For a mortgage switch in 2026, the standard fee for registering a new charge is €175. These payments are essential because they provide the legal security your new lender requires to release the funds, ensuring your transition is fully compliant with Irish property law.

Will the bank’s cashback offer always cover my solicitor’s bill?

For the vast majority of homeowners, a cashback offer will more than cover the legal fees for switching mortgage Ireland. With flat payments of €3,000 or percentage-based offers reaching up to 3% of the loan value, these incentives usually provide a significant surplus. This extra cash can be used to bolster your savings or integrate into your wider retirement planning for enhanced future stability.

Disclaimer

Engage Financial Services LTD T/A Engage Financial Solutions is regulated by the Central Bank of Ireland CRO 764570. Director David Moore. Suite 2 First Floor, 14 -18 Main Street, Blackrock, Co Dublin A94 W0Y3