What if securing your first home wasn’t just about the sprint to save a deposit, but about mastering a marathon of financial organisation? For many, the journey toward a first time buyer mortgage Ireland feels like an uphill battle against rising rents and complex lending criteria. You aren’t alone if you feel that the more you save, the further the finish line seems to move.

It’s understandable to feel anxious about the competitive property market or confused by the latest Central Bank lending limits. Whether you are currently renting whilst trying to build your 10% deposit or you’re unsure how to maximise your borrowing power, we’re here to provide the stability and clarity you need. This guide will help you navigate the 2026 environment with confidence, ensuring you understand exactly how much you can borrow and which government supports you can leverage.

We’ll break down the 4 times income rule, explain how to combine the Help to Buy scheme with the First Home Scheme, and outline the steps for a seamless application. By the end, you’ll have a straightforward roadmap to turn your homeownership aspirations into a secure reality.

Key Takeaways

- Master the Central Bank’s 2026 lending rules, including how to navigate the four times income limit and meet the standard 10% deposit requirement.

- Identify how to leverage government supports like the Help to Buy incentive and the First Home Scheme to bridge the affordability gap on new-build properties.

- Learn the exact sequence of documentation needed to secure an Approval in Principle, giving you a competitive edge in Ireland’s property market.

- Understand the strategic advantage of using a professional broker to navigate your first time buyer mortgage Ireland, ensuring you access the most favourable rates across multiple lenders.

- Develop a proactive plan to manage hidden costs such as stamp duty and legal fees, ensuring your transition to homeownership is straightforward and secure.

Understanding the First Time Buyer Mortgage in Ireland

Securing a first time buyer mortgage Ireland is a significant milestone that requires a blend of financial discipline and strategic timing. In the current market, being a first-time buyer isn’t just a life stage; it’s a specific regulatory category defined by the Central Bank of Ireland. This status grants you access to certain lending advantages, but it also comes with strict criteria that you must meet to qualify for the most favourable terms.

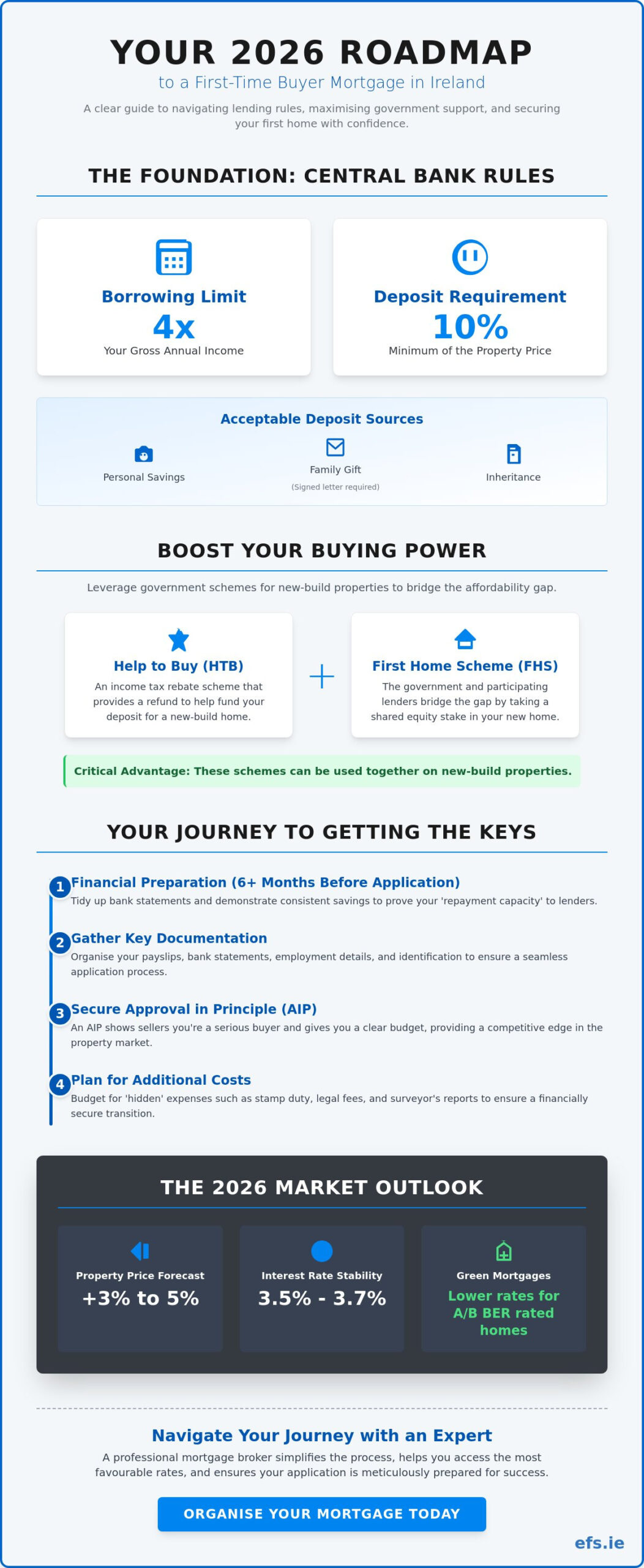

Financial preparation should ideally begin at least six months before you approach a lender. Banks don’t just look at your current savings; they scrutinise your “repayment capacity,” which is your ability to prove you can handle future mortgage repayments based on your current rent and savings patterns. Starting early allows you to tidy up your bank statements and demonstrate the consistent financial behaviour lenders value. Making the right mortgage choice now is fundamental to your long-term security, as the structure of your first loan will dictate your financial flexibility for years to come.

The Definition of a First-Time Buyer

The Central Bank generally defines a first-time buyer as someone who has never previously taken out a housing loan. However, the “Fresh Start” principle provides an essential exception. This rule allows individuals who are divorced, separated, or have gone through personal insolvency to be treated as first-time buyers again, provided they no longer hold an interest in their previous family home. It’s a vital pathway for those seeking to rebuild their lives with a sense of stability.

It’s vital to understand that owning property outside of Ireland can impact your status. If you have previously purchased a home in another country, even if you’ve never owned property in Ireland, you’ll likely be classed as a second-time buyer. This distinction is important because first-time buyer status is a valuable asset, often allowing for higher borrowing limits and access to specific government incentives that aren’t available to others in the Irish economic landscape.

Why 2026 is a Pivotal Year for New Homeowners

The 2026 property market presents a unique set of circumstances. National property prices are forecasted to increase by 3-5% this year, making a proactive strategy more important than ever. Whilst interest rates have stabilised between 3.5% and 3.7% for many products, the market is seeing a significant shift toward energy efficiency. “Green Mortgages” are becoming the standard for new builds, offering lower interest rates for properties with a Building Energy Rating (BER) of A or B.

At Engage Financial Solutions, we help you navigate this evolving environment by identifying which lenders offer the best terms for your specific situation. Whether you are looking at a modern energy-efficient apartment or a traditional starter home, we act as your steady guide. Our role is to remove the friction from the process, ensuring your application is meticulously prepared to meet the latest 2026 lending standards without unnecessary stress.

Navigating Central Bank Lending Rules and Deposit Requirements

Understanding the mechanics of a first time buyer mortgage Ireland begins with the foundational rules set by the regulator. These measures provide a framework of stability, ensuring that your journey into homeownership is sustainable in the long term. The primary pillar is the Loan-to-Value (LTV) ratio, which for first-time buyers currently sits at 90%. This means you are generally required to provide a minimum deposit of 10% of the property’s purchase price.

Lenders are often flexible about the source of this deposit. Whether your funds come from personal savings, a gift from a family member, or an inheritance, the key is transparency. If you are receiving a gift, you’ll need a signed letter from the donor confirming the money is a gift and does not need to be repaid. This ensures the lender that you aren’t taking on an undisclosed debt that could compromise your future financial security. The Central Bank lending rules act as a safeguard for the entire Irish housing market, preventing the kind of over-extension that leads to stress.

Calculating Your Maximum Borrowing Power

First-time buyers can typically borrow up to 4.0 times their gross annual income. While this is the standard limit, lenders have the discretion to grant exceptions, potentially allowing eligible applicants to borrow up to 4.75 times their income. However, these exceptions are limited and highly competitive. When calculating your limit, banks will deduct existing financial commitments such as car loans, credit card balances, and even childcare costs. For a detailed breakdown of exactly how much can I borrow first time buyer Ireland, including how the 15% exemption allowance works and how bonuses are assessed, our dedicated 2026 guide provides a comprehensive roadmap. If you’re unsure how your current expenses might affect your borrowing limit, speaking with an expert can help you organise your finances before you start your application.

Proving Repayment Capacity to Lenders

An underwriter’s primary concern is your “demonstrated repayment capacity.” This is the proof that you can comfortably afford the monthly mortgage cost plus a “stress test” buffer of about 2%. Your best evidence for this is a consistent history of rent and savings. If your combined monthly rent and savings equal or exceed your projected mortgage repayment, you demonstrate a low-risk profile.

Consistency is everything. Lenders require a clean six-month bank statement history. They look for “unusual” behaviour like large unexplained cash withdrawals, missed payments, or evidence of online gambling. A methodical approach to your spending in the months leading up to your application makes the process far more straightforward. By maintaining a predictable financial rhythm, you show the lender that you are a reliable partner for a long-term mortgage commitment.

Maximising Government Support: Help to Buy and the First Home Scheme

Bridging the gap between your hard-earned savings and the purchase price of a new home is often the most challenging part of the journey. Fortunately, the 2026 Irish property market offers robust supports designed to make homeownership more accessible. Applying for a first time buyer mortgage Ireland often involves leveraging specific government incentives that can significantly reduce the amount of cash you need to provide upfront. These schemes are primarily focused on new-build properties, aiming to stimulate the construction of energy-efficient homes whilst helping you secure your future.

The two primary pillars of support are the Help to Buy (HTB) incentive and the First Home Scheme (FHS). While they serve different purposes, they can often be used in tandem to create a comprehensive financing package. It’s vital to understand the price caps and eligibility rules for the 2026 tax year, as these schemes are restricted to properties costing no more than €500,000, and your mortgage must be at least 70% of the property’s value.

The Help to Buy (HTB) Scheme Explained

The HTB scheme acts as a tax rebate, giving you back a portion of the income tax and Deposit Interest Retention Tax (DIRT) you’ve paid over the last four years. You can claim up to 10% of the purchase price, capped at a maximum of €30,000. To claim this, you’ll need to apply through the Revenue Commissioners’ online service to receive a summary of your maximum relief. This amount is then paid directly to the builder as part of your deposit, or to your solicitor if you are embarking on a self build mortgage Ireland project.

- Step 1: Ensure your tax affairs are fully in order for the previous four years.

- Step 2: Apply via the Revenue MyAccount or ROS portal to receive your application number and access code.

- Step 3: Provide these details to your developer or solicitor once you’ve signed your contract.

Common pitfalls often lead to delays or rejections. Applications are frequently stalled because of outstanding tax returns or because the mortgage loan-to-value ratio is slightly below the required 70%. Meticulous attention to these details ensures your path to approval remains straightforward.

The First Home Scheme: Bridging the Gap

The First Home Scheme is a shared equity initiative where the State and participating lenders take a percentage stake in your new home. This bridges the “affordability gap” between your deposit plus your maximum mortgage and the actual price of the property. If you use the HTB scheme, the FHS can provide up to 20% of the equity; if you don’t use HTB, this can rise to 30%.

A significant update in January 2026 saw price caps increased in 17 local authority areas, reflecting the evolving property landscape. While there is no fee for this equity stake for the first five years, a service charge applies from year six onwards, starting at 1.75% per annum. You have the flexibility to buy back (redeem) this equity at any time, either in full or in partial payments, allowing you to eventually own 100% of your home as your financial situation strengthens.

For those currently renting, a “Tenant Home Purchase” variant of the FHS exists, specifically designed to help you buy the home you are currently living in if your landlord decides to sell. Whether you are buying a fresh new-build or purchasing from a landlord, these supports provide a layer of security that makes the transition to homeownership feel manageable and optimistic.

The Step-by-Step Journey to Mortgage Approval

The path to your first home is less about a single leap and more about a series of methodical steps. Once you’ve understood the lending rules and identified your government supports, it’s time to organise your formal application. Securing a first time buyer mortgage Ireland requires precision in your paperwork to ensure a seamless transition from bidder to owner. By treating the process as a sequence of manageable milestones, you can replace anxiety with a sense of calm competence.

Lenders look for a clear, uninterrupted narrative of your financial life. This means your documentation must be current, accurate, and meticulously prepared. Any friction at this stage, such as a missing payslip or an outdated statement, can lead to delays that might cost you your preferred property in a competitive market.

From Saving to Approval in Principle

An Approval in Principle (AIP) is your most powerful tool when house hunting. It’s a statement from a lender indicating how much they’re willing to lend you based on a preliminary review of your finances. In the 2026 market, most estate agents won’t even accept a bid unless you can produce a valid AIP. To secure this, you’ll need to provide a checklist of essential documents:

- Proof of Income: Your Employment Detail Summary (formerly the P60) and your three most recent payslips.

- Salary Certificate: A standard form stamped and signed by your employer confirming your role and earnings.

- Bank Statements: Six months of personal bank statements for every account you hold, including savings and credit cards.

- Identification: Valid passport or driving licence and recent utility bills as proof of address.

Most AIPs remain valid for six months. If your search takes longer, don’t worry; you’ll simply need to provide your most recent payslips and bank statements to refresh the approval. This proactive approach ensures you’re always ready to move when the right home appears.

Sale Agreed to Drawdown: The Legal and Technical Stage

Going “Sale Agreed” is a significant emotional milestone, but it’s where the technical work intensifies. At this point, your lender will instruct a professional valuation to confirm the property is worth the price you’ve agreed to pay. Whilst the bank requires this valuation, you should also commission a private structural survey. This protects your interests by identifying any potential issues with the building before you are legally committed.

Your solicitor plays a vital role here, handling the conveyancing process. They’ll investigate the property’s title, ensure there are no legal impediments to the sale, and manage the exchange of contracts. Simultaneously, you must organise mortgage protection Ireland homeowners rely on and home insurance. These are mandatory requirements for drawdown, providing the long-term security that your investment is safeguarded. On the final “closing day,” your lender transfers the funds to your solicitor, who then pays the seller. Once the paperwork is finalised, you receive the keys to your new home.

To ensure your application is meticulously prepared for every stage of this journey, speak with our expert advisors today for tailored support.

How a Mortgage Broker Organises Your Path to Homeownership

Choosing the right path for your first time buyer mortgage Ireland often depends on the guide you select to walk beside you. Whilst walking into a local bank branch might seem like the obvious first step, it limits your options to a single set of products and criteria. A mortgage broker provides access to a broad panel of lenders, ensuring you aren’t trying to fit your life into a bank’s rigid box. Instead, we find the lender that fits you, offering a level of choice that a single institution simply cannot match.

At Engage Financial Solutions, we act as a vital buffer between you and the inherent complexity of the mortgage market. Our role is to absorb the stress of the process, managing the communication with lenders and solicitors so you can focus on the excitement of your new home. By providing a single point of contact, we remove the friction of repeating your story to multiple institutions, offering a methodical and logical progression from your first inquiry to the day you receive your keys.

The Benefits of Independent Financial Advice

A broker’s value lies in seeing the details that others might miss. We understand which lenders are currently offering the most favourable terms for “Green Mortgages” or which ones are more flexible with specific income structures. Our expertise allows us to “package” your application meticulously, presenting your financial history in the best possible light to bank underwriters. This proactive preparation reduces the likelihood of queries or delays, making the approval process far more straightforward and predictable.

Our commitment to your financial health doesn’t end when you move in. We view our client relationships as long-term partnerships. As market conditions shift and interest rates evolve, we remain your steady guide, ready to help you adapt your financial strategy to meet your changing life goals. Whether you are looking to protect your family or grow your wealth, our authoritative expertise is always available to you.

A Seamless Transition to Your New Home

A truly secure homeownership journey looks at the big picture. Beyond the mortgage itself, we help you integrate essential safeguards like mortgage protection Ireland policies and income protection into your plan. These aren’t just boxes to tick for the bank; they are the foundations of your long-term stability, ensuring that your home remains a safe haven regardless of what the future holds. We take a “future-back” perspective, starting with your goal of total security and working toward the present action.

As you settle into your new property, it’s also worth looking ahead. Our Switching Mortgage Ireland guide illustrates how proactive management of your loan can lead to significant savings in the years to come. Taking the first step towards a stress-free application is simple. You can book an initial consultation with our expert team to discuss your aspirations and begin your journey with confidence. We are here to ensure your transition to homeownership is as smooth and optimistic as possible.

Securing Your Future with Confidence

Homeownership in 2026 is an achievable goal when you approach the market with a clear, methodical plan. By mastering the 4.0 times income limit and leveraging vital supports like the Help to Buy incentive, you’re already halfway there. Whether you’re navigating the complexities of the First Home Scheme or organising your six months of bank statements, remember that the process doesn’t have to be overwhelming. Your journey towards a first time buyer mortgage Ireland is about finding a partner who values your long-term security and peace of mind.

We are regulated by the Central Bank of Ireland and offer access to a wide panel of Irish lenders, alongside deep expertise in HTB and First Home Scheme applications. Our role is to act as your steady guide, ensuring every detail is meticulously handled so you can focus on the excitement of your new home. Start your first-time buyer journey with a personalised consultation to ensure your application is tailored to your unique life goals.

With the right stewardship, the path to your new front door is straightforward and full of promise. We look forward to helping you turn your house-hunting aspirations into a secure and optimistic reality.

Frequently Asked Questions

How much deposit do I really need as a first-time buyer in Ireland?

You generally need a minimum deposit of 10% of the property’s purchase price. For a home costing €400,000, this equates to €40,000. Whilst you can provide more to reduce your monthly repayments, this 10% baseline is the standard requirement under current Central Bank rules. This can be comprised of personal savings, family gifts, or tax rebates through government incentives like the Help to Buy scheme.

Can I get a mortgage if I am self-employed in Ireland?

You can certainly secure a mortgage if you’re self-employed, provided you can demonstrate a stable income history. Most lenders require at least two years of audited accounts or Revenue-certified Chapter 4 settlements. Underwriters will look at your average profit over this period to determine your borrowing power. It’s helpful to have your tax affairs fully up to date before starting the application to ensure a straightforward process.

What is the Help to Buy scheme and how do I apply for it in 2026?

The Help to Buy scheme is a tax rebate designed to help you with your deposit for a new-build home or self-build. In 2026, you apply through the Revenue Commissioners’ online portal, MyAccount. It allows you to claim back up to €30,000 of the income tax and DIRT you’ve paid over the previous four years, provided the property value doesn’t exceed €500,000 and you meet the 70% loan-to-value requirement. If you are considering building your own home, our guide to self build mortgage Ireland options explains how to combine this incentive with stage-payment financing.

How long does the mortgage application process typically take from start to finish?

The journey from initial application to receiving your keys typically takes between three and six months. This timeline includes securing your Approval in Principle, which usually happens within weeks, followed by the property search and the legal conveyancing stage. Whilst some applications move faster, allowing for this window ensures a more methodical and less stressful experience as you transition to your new home.

What are the main extra costs when buying a house besides the deposit?

You should budget an additional 2% to 5% of the purchase price to cover closing costs for first time home buyer Ireland beyond your deposit. The largest expense is typically stamp duty, which is 1% of the property value up to €1 million. Other essential costs include solicitor fees, which often range from €1,500 to €3,000 plus VAT, as well as valuation fees, structural survey costs, and mandatory mortgage protection insurance.

Can I still be considered a first-time buyer if I owned property abroad?

Generally, you aren’t considered a first-time buyer if you’ve previously owned property anywhere in the world. The Central Bank rules are strict on this point to ensure benefits are reserved for those truly entering the market for the first time. However, you might still qualify under the “Fresh Start” principle if you are divorced, separated, or have undergone personal insolvency and no longer have an interest in your previous home.

How does the First Home Scheme affect my mortgage repayments?

The First Home Scheme reduces your monthly mortgage repayments because you are borrowing a smaller amount from the bank. Since the government takes an equity stake to bridge the affordability gap, your loan-to-income ratio is lower. It’s important to remember that whilst there is no charge for the first five years, a service fee applies from year six onwards, which you should factor into your long-term financial planning.

Is it better to go to a bank directly or use a mortgage broker?

Using a mortgage broker is often the more efficient choice because it provides access to multiple lenders through a single application. Whilst a bank can only offer its own products, a broker can compare rates and terms across the entire market to find the best fit for your goals. This stewardship removes the friction of managing multiple applications and ensures your first time buyer mortgage Ireland is handled with professional care.

Disclaimer

Engage Financial Services LTD T/A Engage Financial Solutions is regulated by the Central Bank of Ireland CRO 764570. Director David Moore. Suite 2 First Floor, 14 -18 Main street, Blackrock, Co Dublin A94 W0Y3