What if the biggest threat to your family home isn’t a rising interest rate, but a sudden medical diagnosis that stops your salary in its tracks? In a country where the high cost of living makes every euro count, the fear of being unable to pay the mortgage is a heavy burden for many Irish households. When you’re trying to weigh up income protection vs critical illness Ireland policies, it’s easy to feel overwhelmed by the choice between a one-off lump sum and a steady monthly payment. You want to ensure your family remains secure, but the technical jargon often makes the path forward feel anything but straightforward.

We believe that financial security should feel seamless rather than stressful. This article provides the clarity you need to understand which policy truly fits your lifestyle and long-term goals. You’ll discover the vital differences between these two safeguards, including how income protection covers almost any illness that prevents work, whilst critical illness focuses on specific, defined conditions. We’ll also explain how you can benefit from tax relief at your marginal rate of 20% or 40% on your premiums. By the end, you’ll have the confidence to select a tailored plan that protects your income and your peace of mind.

Key Takeaways

- Learn why relying solely on employer sick pay or the State Illness Benefit can leave a significant gap in your monthly budget during a long-term recovery.

- Understand the mechanism of income protection, which offers a long-term salary safety net by replacing up to 75% of your gross earnings for almost any medically recognised condition.

- Discover the tactical role of critical illness cover in providing a tax-free lump sum to manage immediate costs, such as clearing debts or modifying your home.

- Compare the distinct tax implications and payout structures of income protection vs critical illness Ireland to ensure your chosen policy aligns with your financial goals.

- Gain a straightforward framework for auditing your current benefits and identifying whether your priority is maintaining your daily lifestyle or securing a one-off emergency fund.

Safeguarding Your Lifestyle: Why Financial Protection Matters in Ireland

Maintaining your lifestyle in Ireland isn’t just about what you earn today; it’s about how you safeguard that earning potential for tomorrow. Most of us work hard to build a life we love, yet many families are only a few missed paycheques away from significant stress. This is where the debate of income protection vs critical illness Ireland begins. At its heart, financial protection isn’t about the unlikely event of an illness; it’s about ensuring your standard of living remains constant, even if your ability to work is interrupted. These policies act as a strategic buffer, preventing a medical setback from becoming a financial crisis.

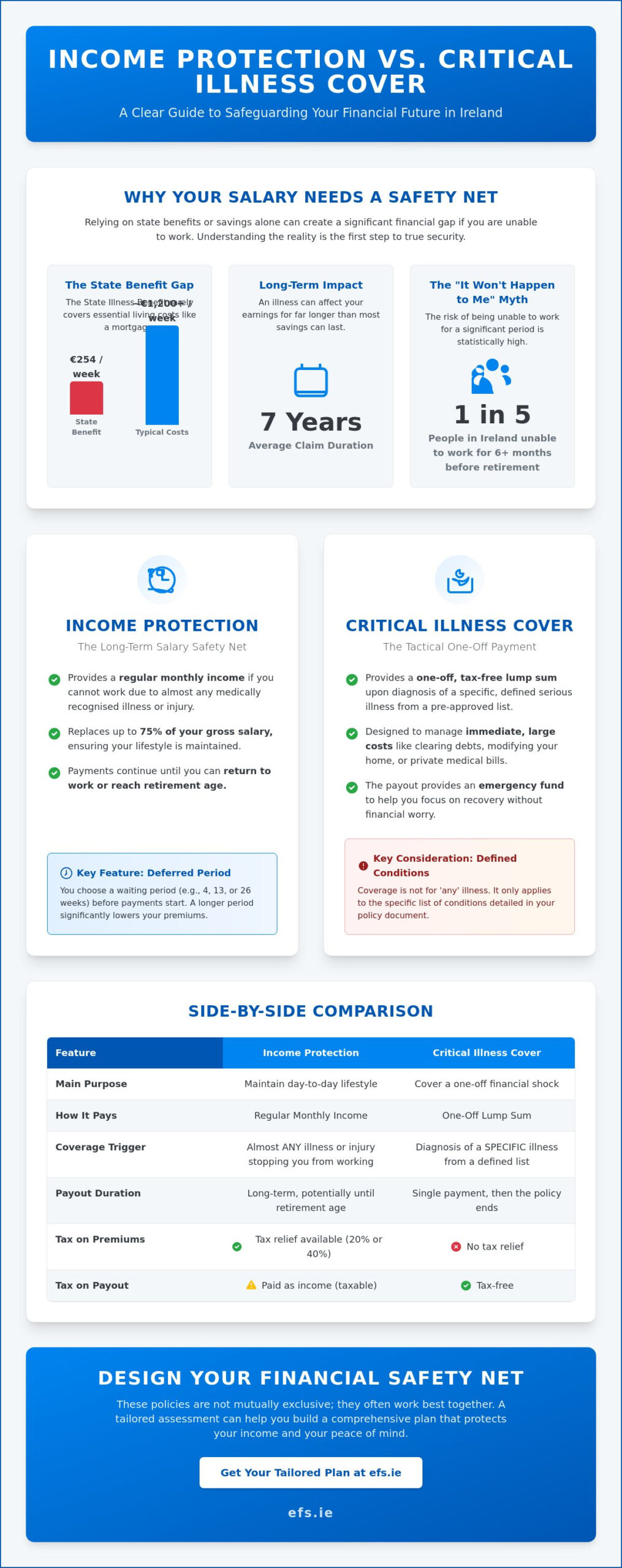

Many people fall into the trap of the “Sick Pay Myth.” You might assume your employer will cover you indefinitely or that the State Illness Benefit will be enough to get by. However, the reality is often stark. The State Illness Benefit currently stands at €254 per week, which rarely covers a modern Irish mortgage, let alone the rising cost of utilities and groceries. Private Income Protection Insurance serves as a vital safety net here. Statistics from providers like Aviva show that the average claim lasts for seven years, a duration that would exhaust almost any personal savings pot. Without a dedicated policy, the gap between what you need and what you have can widen rapidly.

The Financial Risk of Lost Earnings

Have you ever calculated your “financial runway”? It’s a simple but sobering exercise: if your salary stopped tomorrow, how many months could your household survive on savings alone? For many, the answer is measured in weeks rather than years. When illness strikes, the impact on mortgage repayments and household bills is immediate. The “it won’t happen to me” mentality is a common human trait, but with one in five people in Ireland unable to work for at least six months before they reach 65, the risk is statistically significant. Choosing between income protection vs critical illness Ireland allows you to decide how that risk is managed, providing the stability needed to focus on recovery rather than debt.

A Holistic Approach to Security

We view insurance as a fundamental pillar of your broader financial plan, not just an optional extra. For those navigating a first time buyer mortgage Ireland journey, protection is often a mandatory requirement for the loan, but it should also be a personal priority. Integrating these covers into your life ensures that your new home remains a sanctuary, regardless of what life throws your way. A professional, tailored assessment helps you understand these nuances, allowing you to move forward with the calm competence of someone who is truly prepared for the future.

Income Protection Explained: The Long-Term Salary Safety Net

Income protection is designed to act as a financial mirror to your career. Its primary mechanism is straightforward: if you’re unable to work due to illness or injury, the policy provides a monthly payment that replaces up to 75% of your gross salary, less any state benefits. This ensures that your household’s essential rhythm remains undisturbed. Unlike other forms of cover that provide a one-off payment, this is a long-term salary safety net that continues until you’re fit to return to work or reach your chosen retirement age. When weighing up income protection vs critical illness Ireland, the most significant advantage here is the “any illness” clause. You don’t need to suffer a specific, named condition to claim; any medically recognised reason for being unable to work is generally valid.

A vital component in tailoring your policy is the deferred period. This is the “waiting time” between your first day of illness and when the payments begin. You can typically choose between:

- 4 weeks

- 8 weeks

- 13 weeks

- 26 weeks

- 52 weeks

Choosing a longer deferred period, such as 26 or 52 weeks, can significantly lower your monthly premiums. It’s often wise to align this period with your employer’s existing sick pay benefits to ensure a seamless transition from your salary to your insurance payments.

How Income Protection Actually Works

The strength of your cover often depends on the definition of “disability” within the policy. We generally recommend an “Own Occupation” definition. This means the policy pays out if you’re unable to perform the specific duties of your current job, rather than any job. This distinction is crucial for professionals with specialised skills. Before your cover begins, you’ll undergo medical underwriting, a process where the insurer assesses your health to provide a fair and accurate premium. This proactive step ensures that when you need to claim, the process is straightforward and reliable. If you’re unsure how your current role might be classified, you can explore our tailored protection options to find the right fit.

Tax Relief: The Hidden Benefit

One of the most compelling reasons to choose income protection is the generous tax relief offered by Revenue. Unlike Serious Illness Insurance, your premiums for income protection qualify for tax relief at your marginal rate, which is either 20% or 40%. You can claim this relief through your annual tax return or, in many cases, directly through your employer’s payroll system for immediate savings. For a policyholder paying the higher rate of income tax, a monthly premium of €100 effectively costs only €60 after tax relief is applied. This makes comprehensive cover far more accessible, allowing you to secure your future income with minimal impact on your current monthly budget. To ensure you’re selecting the most suitable option, reviewing a detailed best income protection policy Ireland comparison can help you identify the right provider and plan for your occupation and circumstances.

Critical Illness Cover: The Tactical Lump Sum for Specific Diagnoses

Critical illness cover, which is often called “Serious Illness Cover” by Irish providers, serves as a tactical financial tool designed for immediate impact. Instead of providing a monthly salary, it delivers a tax-free lump sum upon the diagnosis of a specified condition. This one-time payment is intended to help you navigate the sudden, often expensive, lifestyle changes that follow a major health event. When comparing income protection vs critical illness Ireland, it’s vital to recognise that this policy is triggered by the diagnosis itself, providing you with a financial injection regardless of your ability to return to work.

Most policies in the Irish market cover a core list of serious conditions, such as cancer, heart attack, stroke, and multiple sclerosis. However, the “List” limitation is a fundamental distinction you must understand. Unlike the broader “any illness” coverage of income protection, critical illness cover only pays out if your condition is explicitly named in your policy documents. This specificity makes it a powerful but narrowly focused safeguard, often acting as a complementary pillar to a more comprehensive protection strategy.

The Role of a Lump Sum Payment

The versatility of a tax-free lump sum is its greatest strength. You might choose to clear your mortgage, fund specialized medical travel, or adapt your home for accessibility. It’s important to distinguish this from standard mortgage protection; whilst mortgage protection pays the bank to clear your debt, critical illness cover pays the money directly to you. This gives you the autonomy to decide where the funds are most needed. You should also be mindful of the “survival period,” a standard clause requiring the policyholder to survive for a set time, usually 14 days, post-diagnosis before the claim is settled.

Where Serious Illness Cover Can Fall Short

Whilst a lump sum offers immediate relief, it can leave gaps in your long-term security. Common reasons for being unable to work, such as chronic back pain or mental health struggles, are rarely included on the specified illness list. As highlighted in this Income protection insurance explained guide, these broader risks are generally better managed through regular salary replacement. Furthermore, a one-off payment might not be sufficient to support a family through a disability that lasts for a decade or more. We always advise clients to review the “severity” definitions in their policy, as some conditions only trigger a payout once they reach a specific clinical stage. Understanding these boundaries ensures your safety net is robust and reliable.

Side-by-Side Analysis: Comparing Payouts, Tax Relief, and Eligibility

Choosing between income protection vs critical illness Ireland policies requires a clear understanding of how they behave when you actually need them. The most immediate difference lies in the payout structure: income protection provides a regular monthly stream that mimics your salary, whilst critical illness cover delivers a one-off, tax-free lump sum. This distinction determines how you manage your finances during a recovery. Whether you need to replace your ongoing monthly earnings or require a significant injection of cash to clear a specific debt, the right choice depends on your existing financial obligations and household budget.

The taxation of these policies is another area where they diverge significantly. Income protection premiums are highly efficient because you receive tax relief at your marginal rate of 20% or 40%. However, the monthly benefits you receive during a claim are treated as income and are subject to PAYE, USC, and PRSI. In contrast, critical illness cover does not offer tax relief on your monthly premiums, but the payout you receive upon diagnosis is entirely tax-free. This trade-off between “relief now” or “tax-free later” is a pivotal factor in determining the long-term value of each plan.

Eligibility for a claim is also governed by different rules. Income protection is inherently more flexible, as it pays out for any medically recognised condition that prevents you from working. Critical illness cover is more rigid, triggered only by conditions that meet the specific severity definitions listed in your policy. Additionally, you can claim on an income protection policy multiple times throughout your career, whereas a critical illness policy typically concludes once the full sum assured has been paid out. This makes income protection a more persistent safeguard for your earning potential over several decades.

Which Policy Offers Better Value?

To evaluate the “true cost” of your cover, you must look beyond the initial quote. For a higher-rate taxpayer, the 40% relief on income protection premiums makes comprehensive cover surprisingly affordable. This is particularly vital for the 340,000 self-employed individuals in Ireland who pay Class S PRSI and don’t qualify for the State Illness Benefit of €254 per week. Income Protection covers any medical reason for absence, whereas Critical Illness is restricted to a predefined list. For many, the ability to claim for mental health issues or back pain makes income protection the more valuable long-term investment for daily survival.

The “Both” Strategy: When a Hybrid Approach Wins

You don’t always have to choose one over the other. A hybrid strategy often provides the most robust safety net, using income protection to cover daily living expenses and a smaller critical illness policy to handle major debts or medical costs. By balancing the levels of cover, you can create a tailored plan that fits your monthly budget without leaving dangerous gaps in your security. A professional review can help you identify these needs and ensure you aren’t paying for redundant cover. If you’re ready to see how these policies can work together for you, you can request a personalised protection review today.

Designing Your Safety Net: How to Choose the Right Protection Strategy

Building a robust financial safety net begins with a clear-eyed look at your current situation. We believe that the most effective protection strategies are built on facts rather than assumptions. Your first step should always be a thorough audit of your existing benefits. Many employees in Ireland discover that their company sick pay is far less extensive than they imagined, perhaps covering only a few weeks of absence. Employers looking to strengthen their staff benefits package beyond individual policies may also wish to explore a group protection scheme Ireland to provide Death in Service and long-term sick pay benefits across their entire workforce. By reviewing your employer’s handbook and any existing life cover, you can pinpoint exactly where your family is vulnerable. This clarity allows you to build a tailored plan that fills those gaps without paying for unnecessary overlaps.

Once you understand your baseline, you need to identify your primary financial fear. For some, the greatest stress is the thought of being unable to meet monthly mortgage repayments over several years. For others, it’s the sudden need for a capital sum to fund private medical treatment or home modifications. Deciding between income protection vs critical illness Ireland often comes down to this distinction: do you need a replacement salary to maintain your daily life, or a tactical lump sum to win a specific medical battle? A regulated advisor can help you navigate the full stack of Irish providers to find the most competitive and comprehensive options for your specific needs.

Tailoring Your Cover to Your Life Stage

Your protection requirements will naturally evolve as you move through different life stages. A young family with a large mortgage and young children typically requires the maximum possible cover to safeguard their future. Conversely, those nearing retirement might prioritise a shorter policy term designed to bridge the gap until their pension or annuities begin. If your budget feels tight, you might consider switching mortgage Ireland to a lower rate. The savings generated from a more efficient mortgage can often be redirected to fund high-quality income protection or critical illness cover, ensuring your home is protected without increasing your monthly outgoings.

Next Steps: Taking Action Today

The most significant risk to your financial stability is often the danger of delaying. Because premiums are calculated based on your age and health status at the time of application, securing your cover today is almost always more cost-effective than waiting until tomorrow. We’re here to make this process as straightforward and stress-free as possible. Our team provides a personalised suitability statement that explains exactly why a specific plan fits your life, giving you the confidence that your future is secure. Taking action now means you can move forward with the peace of mind that comes from knowing your family is looked after, regardless of what life throws your way.

Securing Your Financial Legacy with Confidence

Deciding between a monthly safety net and a tactical lump sum is about more than just picking a policy; it’s about safeguarding your family’s daily reality. You now understand that whilst income protection offers a versatile replacement for your salary, critical illness cover provides the targeted funds needed to tackle specific medical challenges. Navigating the choice of income protection vs critical illness Ireland becomes much simpler when you align your cover with your actual household expenses and long-term aspirations.

We’re here to help you navigate these complexities with calm competence. As a firm regulated by the Central Bank of Ireland, our expert advisors possess deep knowledge of the local insurance market. We provide every client with a personalised suitability statement, ensuring your protection strategy is meticulously tailored to your needs. You don’t have to face these transitions alone.

Secure your family’s future with a tailored protection review from Engage Financial Solutions. By taking this proactive step today, you’re building a foundation of stability and optimism for the years ahead.

Frequently Asked Questions

Can I have both income protection and critical illness cover in Ireland?

Yes, you can certainly hold both policies simultaneously, and many Irish families choose this hybrid approach for maximum security. Whilst income protection replaces your monthly salary, critical illness cover provides a one-off lump sum for immediate expenses. This combination ensures that whether you face a long-term absence or a specific major diagnosis, your financial plan remains robust and flexible.

Is income protection tax-deductible for the self-employed?

Yes, income protection premiums are eligible for tax relief at your marginal rate of 20% or 40%, which is particularly beneficial for the self-employed. This relief is capped at 10% of your total annual income. It’s a highly efficient way to safeguard your earnings, as the government effectively subsidises a significant portion of the policy cost, making comprehensive cover more accessible.

What happens if I have a pre-existing condition?

Pre-existing conditions don’t necessarily prevent you from getting cover, but they will be assessed during the medical underwriting process. The insurer might exclude that specific condition or apply a higher premium based on the risk. It’s vital to be completely transparent during your application to ensure that your policy remains valid and provides the protection you expect when you need to claim.

Does critical illness cover pay out more than once?

Typically, a critical illness policy pays out once and then ceases, as the full sum assured is delivered upon a valid diagnosis. In contrast, income protection allows for multiple claims throughout your career. If you return to work and later fall ill again, you can claim once more, provided you meet the policy criteria. This makes the choice between income protection vs critical illness Ireland a matter of long-term sustainability versus immediate tactical needs.

What is the difference between serious illness cover and mortgage protection?

The fundamental difference is who receives the money. Mortgage protection is designed specifically to pay off your outstanding loan to the bank if you pass away. Serious illness cover pays a lump sum directly to you, giving you the freedom to use the funds for medical bills, home adaptations, or daily living costs. It provides personal autonomy that standard mortgage protection doesn’t offer.

How long do I have to be out of work before income protection starts paying?

The timing depends on the “deferred period” you choose when setting up your policy, which can be 4, 8, 13, 26, or 52 weeks. Payments begin once this waiting period has passed. Most people align this with their employer’s sick pay scheme to ensure there’s no gap in their income. Choosing a longer period, such as 26 or 52 weeks, will lower your monthly premiums significantly.

Is the payout from critical illness cover taxable in Ireland?

No, the lump sum payout from a critical illness policy in Ireland is currently paid tax-free to the policyholder. This makes it a very effective tool for handling large, immediate expenses. However, if you’re comparing income protection vs critical illness Ireland, remember that income protection benefits are treated as earned income and are subject to standard PAYE, PRSI, and USC deductions upon payout.

Do I need income protection if I have a good employer sick pay scheme?

Even with a generous employer scheme, income protection is often necessary because most workplace sick pay only lasts for three to six months. If your illness persists beyond that window, your income could drop to the State Illness Benefit of €254 per week. A private policy bridges this gap, ensuring you can continue to meet your mortgage and household commitments until you’re fit to return to work.

Disclaimer

Engage Financial Services LTD T/A Engage Financial Solutions is regulated by the Central Bank of Ireland CRO 764570. Director David Moore. Suite 2 First Floor, 14 -18 Main street, Blackrock, Co Dublin A94 W0Y3