What if your retirement fund could continue to grow and offer complete flexibility even after you have finished your career? For many, the transition from saving to spending is fraught with worry about outliving their capital or being caught out by complex imputed distribution rules. Choosing an approved retirement fund Ireland allows you to keep your money invested, giving you the freedom to withdraw cash as you need it whilst maintaining the potential for fund growth.

It is completely understandable to feel anxious about balancing your own lifestyle needs with the desire to preserve a legacy for your family. You want a solution that feels stable and secure, without the friction of rigid structures. This guide simplifies the 2026 landscape, covering everything from the updated €2.2 million Standard Fund Threshold to the tax-efficient ways your beneficiaries can inherit your fund. We will walk you through the practical steps to manage your ARF effectively, ensuring your post-work years are defined by comfort and confidence.

Key Takeaways

- Understand how an ARF provides flexibility over your pension capital whilst allowing for continued investment growth throughout your retirement.

- Learn why an approved retirement fund Ireland is a preferred vehicle for maintaining control over your assets and securing a tailored post-work income.

- Navigate the complexities of imputed distributions to ensure you satisfy Revenue mandates while protecting the long-term longevity of your fund.

- Evaluate the trade-offs between fixed annuities and flexible ARFs to determine which option provides the most peace of mind for your specific lifestyle.

- Discover how active stewardship can help preserve your fund’s value, allowing for a more seamless and tax-efficient inheritance for your loved ones.

What is an Approved Retirement Fund (ARF) in Ireland?

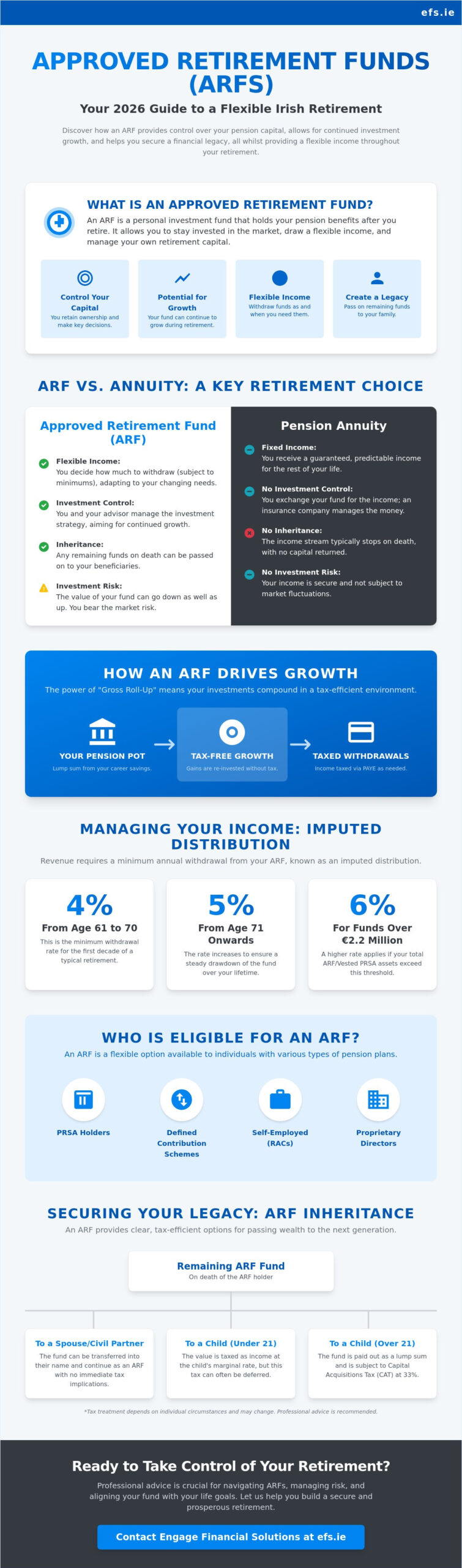

An approved retirement fund Ireland is essentially a personal investment account that holds your pension benefits after you retire. Think of it as the vehicle that takes over once you’ve finished the “accumulation” phase of your working life. Within the broader Irish pension system, the ARF offers a level of flexibility that was previously more restricted. Since January 2022, the landscape has become even more straightforward following the abolition of the Approved Minimum Retirement Fund (AMRF). All existing AMRFs were converted into ARFs, removing the requirement to “lock away” a portion of your savings. This shift reflects a move towards giving retirees greater autonomy over their own capital.

The core purpose of an ARF is to provide you with a regular income whilst keeping your remaining funds invested. This means your capital has the potential to continue growing, even as you draw from it. It’s a fundamental shift in mindset. You’re moving from a period of disciplined saving to one of active stewardship. Instead of handing over your pot to an insurance company in exchange for a fixed payment, you retain ownership of your money. This allows for a more personalised approach to your post-work finances, ensuring your income can adapt as your lifestyle needs change over time.

Eligibility: Who can open an ARF?

The path to an approved retirement fund Ireland depends on the type of pension you’ve built. If you hold a Personal Retirement Savings Account (PRSA), you can transition into an ARF structure quite seamlessly once you reach retirement age. This is particularly beneficial for those who want to avoid the rigid nature of an annuity. Members of defined contribution (DC) schemes and holders of retirement bonds also have this option. Additionally, proprietary directors and self-employed individuals with Retirement Annuity Contracts (RACs) often find that an ARF aligns best with their complex financial needs. At Engage Financial Solutions, we help you determine if your specific pension type qualifies for this flexible drawdown route.

The Role of the Qualifying Fund Manager (QFM)

Setting up an ARF isn’t something you do entirely on your own. You’re legally required to appoint a Qualifying Fund Manager (QFM). The QFM acts as the custodian of your funds, ensuring that your money stays within a tax-efficient environment. One of the greatest benefits of this structure is “gross roll-up,” where any investment gains within the fund are not subject to immediate tax. Your QFM handles all the necessary reporting to Revenue and manages the tax deductions on your withdrawals. Choosing the right manager is vital. You need a partner who understands your risk tolerance and can tailor the investment strategy to suit your long-term goals.

How an ARF Works: Investment, Growth, and Tax

Once you’ve established your approved retirement fund Ireland, it functions as a highly tax-efficient environment for your capital. The standout feature of this structure is “gross roll-up.” This means any dividends, interest, or capital gains earned within the fund are reinvested without being eroded by immediate taxation. According to Revenue’s official ARF guidelines, this tax-free status remains as long as the funds stay within the ARF wrapper. This compounding effect acts as a powerful engine, helping your savings work harder even whilst you are drawing an income.

Investment flexibility is what truly sets the ARF apart. You aren’t tied to a single asset class or a rigid payment schedule. You can choose from a vast range of options, from low-risk cash accounts and government bonds to diversified equity portfolios and property funds. We often encourage a “future-back” perspective. This involves looking at your projected income requirements 20 years from now and working backward to decide how much growth you need today. It’s about finding a strategy that provides enough liquidity for your current lifestyle while keeping enough growth-oriented assets to combat the rising cost of living. A well-structured approach to retirement planning Ireland ensures that your ARF investment strategy is aligned with your broader financial goals from the outset.

Managing this growth requires a steady hand and proactive planning. One of the biggest threats to a successful retirement is “sequencing risk.” This is the danger of a significant market downturn occurring early in your drawdown phase. If you’re forced to sell assets at a loss to fund your mandatory withdrawals, your capital can deplete much faster than originally planned. Professional stewardship helps you build a buffer, perhaps through a tiered approach, to safeguard your income during volatile periods. If you’re unsure how to structure these layers, consulting with a retirement specialist can help clarify the best approach for your specific circumstances.

The Tax-Free Lump Sum and the Remainder

Most pension holders opt to take their 25% tax-free lump sum at the point of retirement. The remaining 75% then transfers directly into your approved retirement fund Ireland. This transfer doesn’t trigger a tax charge, allowing the full balance to start working for you immediately. Whilst the investment grows tax-free, withdrawals are subject to PAYE. This includes Income Tax, USC, and PRSI where applicable, so it’s vital to plan your drawdown strategy to remain as tax-efficient as possible over the long term.

Balancing Risk and Reward in Post-Work Life

It’s tempting to move everything into cash once you stop working to avoid market fluctuations. However, being “too safe” carries its own risks. Inflation can quietly erode your purchasing power over a 30-year retirement. An ARF allows you to find a sensible middle ground. By maintaining a portion of your fund in growth assets, you give your capital the opportunity to outpace rising costs. The goal is to create a stable income stream that doesn’t sacrifice your future security for present-day caution.

ARF vs. Annuity: Choosing the Right Path for 2026

Choosing between an annuity and an approved retirement fund Ireland is one of the most significant decisions you’ll make at the point of retirement. An annuity acts as an insurance policy against living a very long time; it provides a guaranteed income for life, regardless of how markets perform. In contrast, an ARF is an investment vehicle that gives you full control over your capital. While the annuity offers “peace of mind” through certainty, the ARF is often favoured in 2026 for its ability to combat inflation and its superior death benefits. Many retirees now opt for a hybrid approach, using a portion of their fund to purchase a baseline annuity for essential bills while keeping the remainder in an ARF for lifestyle flexibility and growth potential.

Deciding which path to take depends on your personal risk tolerance and your long-term goals for your family. If your primary concern is ensuring you never run out of money, an annuity provides a stable floor. However, if you value the ability to adjust your income or leave a residual fund to your heirs, the ARF structure is typically more appropriate. It’s about balancing the need for security with the desire for autonomy. We often see clients choose the ARF because it feels less like a final transaction and more like a continuing partnership with their wealth.

The Flexibility Factor: Accessing Your Capital

The “locked-in” nature of an annuity means that once you’ve purchased it, your capital is gone in exchange for that regular payment. An ARF offers a far more “on-demand” experience. Whether you’re planning a special family wedding or finally taking that dream trip around the world, an ARF allows for ad-hoc withdrawals beyond your regular income. This level of control ensures your money remains responsive to your life’s changing chapters. For a deeper look at the alternative, our Annuity Ireland guide provides a comprehensive breakdown of how guaranteed income structures work.

Inheritance and Death Benefits

One of the most compelling reasons to choose an approved retirement fund Ireland is the preservation of your legacy. If you pass away, the remaining value of your fund doesn’t disappear; it forms part of your estate. As noted in the Citizens Information guide to personal pensions, the transfer of an ARF to a surviving spouse or civil partner is typically tax-free, allowing them to continue drawing an income seamlessly. If the fund passes to children over the age of 21, it is subject to a flat 30% income tax rate rather than Capital Acquisitions Tax. This stewardship aspect ensures that your years of hard work continue to benefit your loved ones long after you’re gone. It provides a level of financial continuity that a standard annuity simply cannot match.

Managing Your Income: Withdrawals and the Imputed Distribution

Whilst an approved retirement fund Ireland offers incredible flexibility, it’s important to understand that Revenue doesn’t allow the funds to sit untouched indefinitely. To ensure a steady flow of tax revenue, the “Imputed Distribution” rule requires you to withdraw a minimum percentage of your fund’s value every year once you reach a certain age. From the year you turn 61, you must take a minimum withdrawal of 4%. This requirement increases to 5% once you reach the age of 71. If your total ARF and vested PRSA holdings exceed €2 million, the mandatory withdrawal rate rises to 6% per year. These rules apply regardless of whether you actually need the income at that time.

Every withdrawal you make is treated as earned income and is subject to the standard PAYE system. This means you’ll pay Income Tax and Universal Social Charge (USC) on the gross amount. If you’re under the age of 66, you’ll also typically pay Class S PRSI, which is currently set at 4.2%. Once you reach 66, you’re generally exempt from PRSI on these payments. Managing these layers of taxation requires careful foresight to ensure you don’t inadvertently push yourself into a higher tax bracket during a single financial year.

Calculating Your Net Retirement Income

Understanding the difference between your gross withdrawal and the net amount that lands in your bank account is vital for accurate budgeting. When you request a withdrawal from your approved retirement fund Ireland, your Qualifying Fund Manager (QFM) calculates the tax due based on your current tax credits and cut-off points. They then deduct these amounts before transferring the balance to you. If you’re still in the process of building your pot, you might find our PRSA Ireland guide helpful for understanding how your savings phase impacts these eventual payments. If you want to ensure your withdrawal strategy is as tax-efficient as possible, you can speak with our advisory team for a personalised review.

Avoiding the “Fund Depletion” Trap

The greatest risk with an ARF is withdrawing too much too early, which can cause your capital to run dry later in life. While the mandatory minimums are set by Revenue, you have the freedom to take more if you wish. However, high withdrawals in the early years of retirement can significantly reduce the “compounding engine” we discussed earlier. The imputed distribution is effectively a “use it or lose it” tax mechanism that ensures the state receives its share of your pension pot throughout your retirement. To protect your long-term security, we recommend a “smoothing” strategy. This involves taking enough to live comfortably whilst leaving enough invested to allow for potential growth and inflation protection over a 20 or 30 year period.

Securing Your Legacy: Why Professional ARF Advice Matters

Managing an approved retirement fund Ireland is not a “set and forget” task. While online calculators provide a rough estimate, they cannot account for the nuances of your personal life or the shifting economic environment. A steady guide is essential to help you navigate the complexities of market volatility and regulatory changes. At Engage Financial Solutions, we provide a “full-stack” advisory service. This means we support you through every stage, from the initial accumulation of your pension to the strategic drawdown of your ARF. We act as the buffer between you and the complexities of the financial world, ensuring your transition into retirement is as smooth as possible.

Annual reviews are a cornerstone of effective stewardship. These meetings allow us to rebalance your portfolio, ensuring your asset allocation still aligns with your long-term goals. If the markets have been particularly strong, we might suggest locking in some gains to protect your future income. Conversely, if there has been a downturn, we adjust your strategy to mitigate the sequencing risk discussed earlier. An ARF shouldn’t exist in isolation. It works best when integrated into a wider financial security plan that includes life cover and other investments, providing a holistic buffer for you and your family.

Tailored Portfolios for Every Lifestyle

We don’t believe in generic risk scores that treat every retiree the same. Instead, we organise your approved retirement fund Ireland based on your specific future aspirations. Whether you’re planning to downsize, travel extensively, or leave a significant inheritance, your portfolio should reflect those intentions. Having a consultant who understands the Irish regulatory landscape intimately is a distinct advantage. We stay ahead of changes to the Standard Fund Threshold and inheritance tax rules so you don’t have to. For a personalised consultation that focuses on your unique needs, you can contact Engage Financial Solutions today.

A Seamless Transition to Retirement

The transition from a working life to retirement should be a time of celebration, not a period buried in paperwork and Revenue compliance. Our team takes over the heavy lifting, managing the technical requirements of setting up your ARF and ensuring all tax reporting is handled correctly. We pride ourselves on “calm competence,” removing the friction from financial processes so you can focus on enjoying your post-work years. By proactively anticipating potential stresses, we safeguard your future and provide the peace of mind you’ve earned. Ensure your hard-earned pension works as hard as you did.

Crafting a Secure and Flexible Future

Mastering your post-work income is about more than just numbers; it’s about the freedom to live life on your terms. By choosing an approved retirement fund Ireland, you’ve opted for a path that prioritises flexibility and growth. Whether you’re navigating the mandatory imputed distribution rules or planning a seamless legacy for your children, the right strategy ensures your capital remains a robust engine for your lifestyle. You don’t have to manage these transitions alone.

At Engage Financial Solutions, we provide the expert guidance needed to manage these complexities with confidence. As a firm regulated by the Central Bank of Ireland, we specialise in bespoke financial planning tailored to your unique goals. Whether you need clarity on ARF, PRSA, or Annuity structures, our team offers steady, professional support. Book a Personalised Retirement Consultation with Engage Financial Solutions today and ensure your peace of mind for the years ahead. You’ve worked hard for your savings; it’s time to make them work for you.

Frequently Asked Questions

Can I change my mind and buy an annuity after starting an ARF?

Yes, you can choose to purchase an annuity using your ARF funds at any point in the future. This provides a valuable “exit ramp” if your priorities shift from capital growth to a guaranteed lifetime income. Whether you want to secure a baseline income for essential costs or simply prefer the certainty of fixed payments as you get older, the transition is straightforward and flexible.

What is the minimum amount required to start an Approved Retirement Fund?

There is no legal minimum set by Revenue to establish an approved retirement fund Ireland, but most individual providers set their own thresholds. Typically, you might need a fund value of at least €20,000 to €50,000 to make the structure cost-effective after management fees. It’s best to check with your specific provider to ensure the fund size justifies the ongoing administrative costs.

How is an ARF taxed if I leave it to my children?

If you leave your ARF to children over the age of 21, the fund is subject to a flat income tax rate of 30%. Crucially, these funds are generally exempt from Capital Acquisitions Tax (CAT) for adult children. If the beneficiaries are under 21, the inherited fund is treated as a standard inheritance and falls under the normal CAT rules and thresholds instead.

What happens to my ARF if the stock market crashes?

Because your ARF remains invested, its value will fluctuate in line with market performance. A significant downturn can reduce your capital, especially if you’re forced to make mandatory withdrawals while prices are low. This is why we emphasise a diversified portfolio and active stewardship to help buffer your income against short-term volatility and protect your long-term security.

Can I have more than one ARF at the same time?

Yes, you’re permitted to hold multiple ARF accounts simultaneously, perhaps with different providers or investment strategies. However, the imputed distribution rules will apply to the total value of all your qualifying funds combined. Managing multiple accounts can sometimes add administrative complexity, so many retirees prefer to consolidate their funds for a more seamless overview of their post-work income.

Do I have to take a withdrawal from my ARF every year?

You are legally required to take a minimum withdrawal once you reach the year you turn 61. This “imputed distribution” starts at 4% and increases to 5% from age 71. If you don’t take the withdrawal, Revenue will still tax you as if you had, making it a “use it or lose it” scenario that requires proactive annual planning.

Is an ARF better than a PRSA for retirement income?

Neither is objectively “better,” as the right choice depends on your original pension type and your specific goals. While a vested PRSA now offers similar drawdown flexibility to an approved retirement fund Ireland, an ARF remains the standard destination for many company pension schemes. We evaluate your existing structures to ensure you’re using the most tax-efficient vehicle for your unique circumstances.

How do I choose the best funds for my ARF portfolio?

Choosing the right funds involves balancing your need for immediate income with the necessity of long-term capital growth. We look at your risk tolerance, your 20-year income requirements, and the impact of inflation on your purchasing power. A tailored approach usually involves a mix of equities, bonds, and cash to ensure your fund outlives your retirement needs. If you are still in the accumulation phase of your career, our guide to self employed pension Ireland options can help you build the strongest possible foundation before transitioning into an ARF.

Disclaimer

Engage Financial Services LTD T/A Engage Financial Solutions is regulated by the Central Bank of Ireland CRO 764570. Director David Moore. Suite 2 First Floor, 14 -18 Main street, Blackrock, Co Dublin A94 W0Y3