What if your retirement plan was as dynamic as your career, moving with you from one role to the next without the friction of being locked into a rigid, outdated scheme? You’ve likely felt the weight of confusion when faced with complex pension terminology or the fear that a personal retirement savings account Ireland might be too complicated to manage alone. It’s perfectly natural to want a retirement strategy that offers both security and the freedom to adapt as your life evolves. Whether you’re starting your first professional role or you’re an experienced executive looking to maximise your savings, you deserve a solution that feels like a partnership rather than a transaction.

This guide explains how a PRSA provides a tax-efficient foundation for your future whilst allowing you to maintain total control over your contributions. We’ll explore how these accounts work, the generous tax relief available in 2026, and how they help you stay ahead of the new auto-enrolment requirements. By the end of this article, you’ll understand how to safeguard your lifestyle and ensure your transition into retirement is as seamless as possible.

Key Takeaways

- Learn how a personal retirement savings account Ireland offers you complete ownership and control, ensuring your pension remains your asset regardless of your employer.

- Understand the differences between Standard and Non-Standard PRSAs so you can tailor your investment strategy to match your specific risk appetite and future goals.

- Discover how to maximise your financial efficiency through immediate tax relief on contributions and tax-free investment growth within your fund.

- Explore the seamless portability of a PRSA, which allows you to carry your pension progress through every career move and consolidate multiple old pension pots with ease.

- Gain the confidence to navigate complex retirement decisions with a steady guide that prioritises your long-term security and peace of mind.

What is a Personal Retirement Savings Account (PRSA) in Ireland?

A Personal Retirement Savings Account (PRSA) is essentially a long-term investment vehicle designed to help you build a secure financial future. Unlike traditional occupational pensions, which are often tied to a specific company, a PRSA is a contract between you and an authorised provider. This means you own the account entirely. It’s yours to keep, manage, and grow, regardless of where your career takes you. For many, a personal retirement savings account Ireland provides the ultimate sense of stewardship over their wealth, removing the friction often associated with switching jobs or changing employment status.

The stability of this scheme is backed by strict oversight. Every PRSA is regulated by the Pensions Authority and the Revenue Commissioners, ensuring that your savings are managed within a clear legal framework. One of the most inclusive features of the PRSA is its accessibility. You don’t need to be in a specific type of job to open one; it’s available to employees, the self-employed, homemakers, or even those who are currently between roles. This universal design ensures that no one is left behind as they plan for their later years.

Who should consider a PRSA?

While the PRSA is open to almost everyone, it’s particularly valuable for those who lack access to a standard workplace scheme. If you’re self-employed, you likely don’t have an employer-sponsored pension, making the PRSA a vital tool for creating your own safety net. It’s also an excellent choice for contract workers or part-time staff who might move between various employers frequently. If your current workplace doesn’t offer an occupational pension, or if you simply want a portable personal retirement savings account Ireland that follows you through every career transition, this account offers the peace of mind you need.

The core benefits of a PRSA

The primary appeal of the PRSA lies in its adaptability. Life rarely follows a straight line, and your pension should be able to keep pace with your changing circumstances. These accounts offer several distinct advantages:

- Unmatched Flexibility: You have the freedom to increase, decrease, or even pause your contributions if your financial priorities shift. There are no penalties for making these adjustments, which removes the anxiety of being locked in during leaner months.

- Seamless Portability: Since the account is yours, it moves with you. You won’t have to worry about leaving pension pots behind at former companies or dealing with the stress of complex transfers every time you change roles.

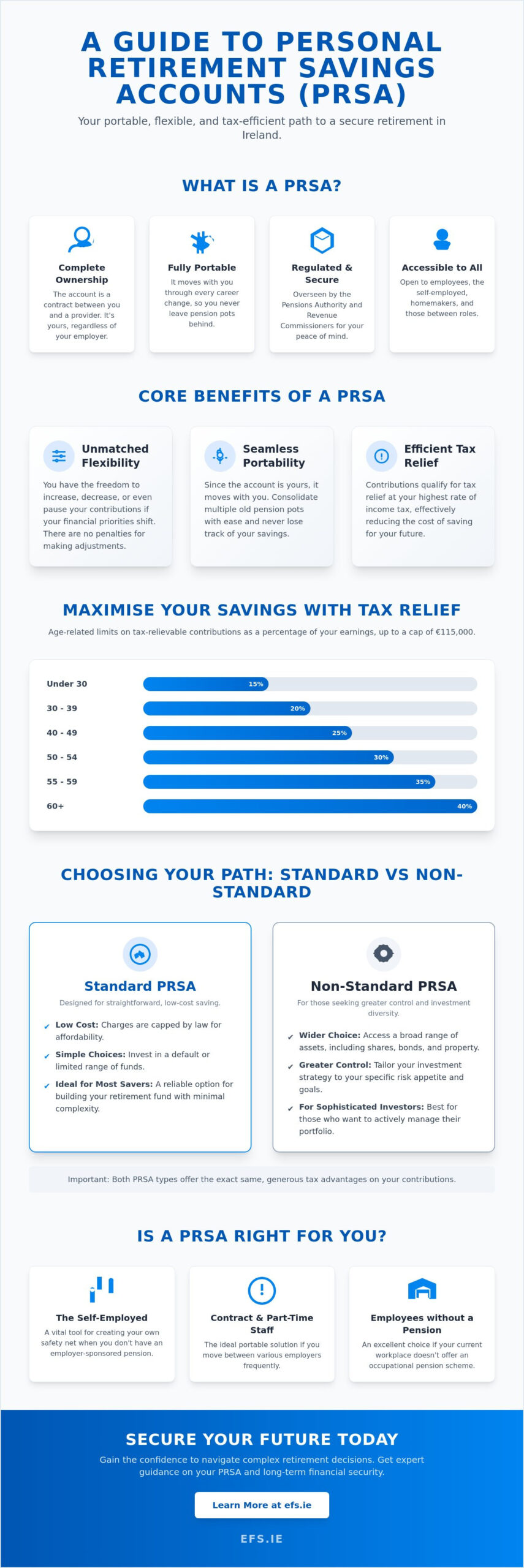

- Efficient Tax Relief: Every contribution you make qualifies for tax relief at your highest rate of income tax, up to an earnings cap of €115,000. Depending on your age, you can claim relief on 15% to 40% of your earnings. This effectively reduces the cost of saving, as money that would have gone to the taxman is instead redirected into your own future.

By focusing on these practical advantages, you can build a retirement fund that feels like a supportive partner in your professional journey. It’s about creating a foundation that is as steady as it is versatile.

Standard vs Non-Standard PRSAs: Choosing the Right Path

Deciding between a Standard and Non-Standard personal retirement savings account Ireland is one of the most significant steps in tailoring your financial future. While both options share the same core DNA, the “engine” under the hood operates differently. It’s reassuring to know that both types offer the exact same tax advantages; your choice won’t affect your ability to claim relief on your contributions. Instead, the decision hinges on your personal risk appetite, your investment goals, and how much control you want over your specific assets.

Selecting the wrong path can have a quiet but profound impact on your long-term growth. For instance, paying higher fees for a Non-Standard account without actually utilising its wider investment features could unnecessarily eat into your final fund. Conversely, opting for a Standard account when you have sophisticated investment needs might leave you feeling restricted. Professional guidance is often the buffer that prevents these misalignments, ensuring your pension plan remains a source of stability rather than stress.

The Standard PRSA: Low Cost and Capped Charges

The Standard PRSA is designed for those who value simplicity and cost-certainty. By law, the charges on these accounts are strictly capped. You’ll never pay more than 5% on your contributions, and the annual management charge is limited to 1% of the fund’s value. These accounts generally invest in a range of pooled funds, such as managed or tracker funds. It’s a straightforward, “no-surprises” approach that works exceptionally well for the majority of savers who want a reliable, low-maintenance foundation for their retirement.

The Non-Standard PRSA: Greater Investment Choice

If you’re looking for more bespoke options, the Non-Standard personal retirement savings account Ireland provides a much broader canvas. Unlike the Standard version, there are no legal caps on charges, so fees can vary significantly amongst different providers. However, in exchange for these potentially higher costs, you gain access to a vast array of assets. This might include individual stocks, international equities, or even direct commercial property. This path is often favoured by sophisticated investors or business owners who want their pension to reflect a specific, diversified portfolio. If you’re unsure which path fits your lifestyle, speaking with a retirement specialist can provide the clarity you need to move forward with confidence.

Maximising Tax Relief and Financial Efficiency

One of the most compelling reasons to establish a personal retirement savings account Ireland is the immediate boost it gives to your take-home financial efficiency. Every Euro you contribute is deducted from your gross income before income tax is applied. This means that if you’re a higher-rate taxpayer, a €100 contribution effectively costs you just €60. It’s a rare opportunity where the government actively helps you build your wealth; turning what would have been a tax liability into a cornerstone of your future security. By prioritising these contributions, you’re not just saving for the future; you’re optimising your current income in the most professional way possible.

Understanding age-related contribution limits

Revenue allows you to claim relief based on your age, recognising that your capacity to save often increases as you progress through your career. These limits ensure that you can accelerate your savings as you approach retirement. Revenue determines the maximum tax-relievable contribution you can make based on a percentage of your gross earnings that increases as you get older.

- Under 30: 15% of your gross earnings

- 30 to 39: 20% of your gross earnings

- 40 to 49: 25% of your gross earnings

- 50 to 54: 30% of your gross earnings

- 55 to 59: 35% of your gross earnings

- 60 and over: 40% of your gross earnings

The total amount of annual earnings you can claim tax relief on is currently capped at €115,000. If you earn more than this, you can still contribute to your PRSA, but you won’t receive tax relief on the portion of your contribution that relates to earnings above this threshold.

The long-term impact of tax-free growth

Unlike a standard bank account where interest is subject to Deposit Interest Retention Tax (DIRT), or personal investments subject to Capital Gains Tax, your PRSA fund grows in a completely tax-free environment. This lack of friction allows the power of compounding to work much harder for you. Over several decades, the difference between a taxed investment and a tax-exempt personal retirement savings account Ireland can be staggering. This efficiency is why we often view the PRSA as a central pillar in a wider savings and investments Ireland strategy, providing a protected space for your capital to flourish without the drag of annual taxation.

When you eventually reach retirement, the benefits continue through a tax-free lump sum. You can typically take up to 25% of your fund as a tax-free payment, up to a lifetime limit of €200,000. This provides a significant injection of liquidity just when you need it most, whether you’re clearing a remaining mortgage or funding a new lifestyle goal. For those seeking to convert the remainder of their fund into a predictable income stream, understanding your annuity Ireland options is an essential next step in securing guaranteed retirement income. Alternatively, transferring the balance into an approved retirement fund Ireland allows you to keep your capital invested whilst drawing a flexible income that adapts to your lifestyle needs. By future-proofing your finances today, you’re ensuring that your transition into retirement is defined by choice and comfort rather than compromise.

Portability and Flexibility: Adapting to Your Career

A common misconception is that starting a pension involves entering a rigid, lifelong contract that lacks the agility of modern professional life. In reality, a personal retirement savings account Ireland is specifically designed to be the opposite. It functions as a “pension for life” that anchors your financial security whilst allowing you to move freely between roles, industries, or even countries. This portability removes the friction of leaving behind multiple small, forgotten pension pots every time you switch employers. Instead of managing a fragmented trail of old schemes, you have the power to consolidate your savings into one single, streamlined account that grows with you.

The flexibility of a PRSA also extends to your lifestyle choices. Whether you’re planning a sabbatical to travel, taking a career break to raise a family, or transitioning into consultancy, your PRSA adapts to your rhythm. You have the total freedom to stop, start, increase, or decrease your contributions without facing penalties or administrative hurdles. This level of control ensures that your retirement planning remains a supportive part of your life rather than a source of financial stress during periods of transition.

Changing jobs and moving employers

One of the most reassuring aspects of the PRSA structure is that you don’t need to start from scratch every time you sign a new employment contract. Your account is owned by you, not your boss. If you move to a firm that doesn’t offer an occupational scheme, Irish law requires your employer to provide you with access to at least one Standard PRSA. At Engage Financial Solutions, we specialise in making this transition feel entirely seamless. We act as the steady guide, helping you navigate the paperwork to ensure your contributions continue without interruption, providing you with a sense of “calm competence” throughout your career journey.

Employer contributions and the PRSA

Whilst a PRSA is a personal account, it’s important to recognise that your employer can also contribute to it. Since the Finance Act 2024, employer contributions are highly efficient, with companies able to contribute up to 100% of an employee’s salary into a PRSA without it being treated as a Benefit in Kind (BIK) for the staff member. This makes it an incredibly attractive alternative to a traditional company pension Ireland structure. Employers benefit from Corporation Tax relief on these payments, creating a mutually beneficial arrangement that strengthens your long-term stability. If you’re ready to consolidate your old pensions into one manageable account, contact our team today to explore your options.

Securing Your Future with Engage Financial Solutions

Choosing to open a personal retirement savings account Ireland is a significant milestone, but it’s only the first step in a much larger journey toward lifelong security. Our role at Engage Financial Solutions is to act as your steady guide, providing the calm competence needed to filter through the noise of the financial markets. We understand that the transition from active earning to retirement can feel daunting. By positioning ourselves as your long-term partner, we aim to replace that uncertainty with a sense of stability and optimism. You aren’t just another transaction to us; you’re a client whose future deserves meticulous stewardship and proactive management.

We don’t believe in a one-size-fits-all approach. Whether you’re a first-time saver looking for a low-maintenance Standard PRSA or a senior professional seeking the sophisticated investment options of a Non-Standard account, we tailor our advice to your specific life stage. Our goal is to ensure that your retirement plan is a seamless part of your broader lifestyle aspirations, providing the peace of mind that comes from being truly looked after by experts who anticipate your needs before they become stresses.

Our personalised advisory process

Our journey together begins with a deep dive into your current financial standing and your long-term aspirations. We take the time to understand your risk appetite and your vision for the future, ensuring that the provider and investment strategy we select amongst the many options available is perfectly aligned with your goals. This isn’t a fragmented service. We look at the big picture, ensuring your personal retirement savings account Ireland is fully integrated with other vital safeguards, such as your income protection Ireland plans. This holistic approach ensures that your wealth is protected from every angle, allowing you to focus on your career whilst we manage the complexities of your portfolio.

Take the first step toward stability

Moving from a state of uncertainty to one of prepared optimism is a powerful shift. Retirement planning isn’t a “set and forget” task; it requires ongoing reviews to ensure your plan stays on track as your life evolves and regulations change. We provide the reliability you need to stay ahead of these shifts, making adjustments whenever necessary to keep your trajectory toward success. By working backward from your desired retirement lifestyle, we make the present actions feel logical and goal-driven. If you’re ready to build a foundation that is as flexible as it is secure, speak with our retirement planning experts today to begin your journey toward a seamless financial future.

Building Your Foundation for Long-Term Security

Planning for your later years doesn’t have to be a source of friction or anxiety. By choosing a personal retirement savings account Ireland, you’re opting for a retirement solution that adapts to your life instead of forcing you to conform to a rigid scheme. You’ve seen how these accounts offer unmatched portability between jobs and how the power of tax-free growth can significantly enhance your final fund. Whether you’re just starting your career or consolidating existing pension pots, the focus is always on creating a seamless path toward your desired future.

Engage Financial Solutions is here to provide the steady guidance you need to navigate these choices with confidence. As a firm regulated by the Central Bank of Ireland, we offer expert guidance from qualified financial advisors who specialise in tailoring strategies to your specific life stage. We pride ourselves on a meticulous, client-centric approach that removes the stress from complex financial transitions. Secure your financial future with a tailored PRSA from Engage Financial Solutions. You deserve the peace of mind that comes from knowing your future is in safe hands, allowing you to move forward with prepared optimism.

Frequently Asked Questions

What is the difference between a PRSA and a personal pension?

A PRSA is a more modern, flexible contract between you and a provider, whereas a traditional personal pension is an older structure often used by the self-employed. Unlike personal pensions, a personal retirement savings account Ireland allows for employer contributions without complex administrative hurdles. This makes it a superior choice for individuals who value seamless transitions between different employment types and want a fund that stays under their total control.

Can I have a PRSA and a company pension at the same time?

Yes, you can contribute to a PRSA alongside an occupational scheme, often to top up your benefits or consolidate old funds from previous roles. This is a common strategy for professionals who have reached the contribution limits of their workplace scheme or want to maintain a separate, portable fund. Your total tax relief remains subject to the age-related percentage limits across all your combined pension arrangements.

How much are the typical charges on a Standard PRSA in Ireland?

For a Standard PRSA, the law strictly caps charges at 5% of each contribution and an annual management fee of 1% of the total fund value. These caps ensure that your savings aren’t eroded by high costs, providing a straightforward and predictable fee structure. Non-Standard versions don’t have these caps, allowing for wider investment choice but requiring more careful fee comparison to ensure long-term stability.

What happens to my PRSA if I move abroad?

Your PRSA remains your personal property if you leave Ireland, and you can generally leave the funds invested to grow until you reach retirement age. Depending on the country you move to, you may be able to transfer the value of your fund to an overseas pension arrangement that meets Revenue requirements. It’s a highly portable solution that ensures your hard-earned progress isn’t lost simply because your life takes you across borders.

Can I withdraw money from my PRSA before I retire?

In most cases, you cannot access your PRSA funds until you reach age 60, though certain exceptions exist for early retirement or ill health. If your fund value is small and you haven’t contributed for at least two years, you might be eligible for a refund, though this is subject to tax. Generally, the fund is designed to stay locked away to safeguard your future security and benefit from tax-free compounding.

Does my employer have to contribute to my PRSA?

While employers must provide you with access to a PRSA if they don’t offer an occupational scheme, they aren’t always mandated to contribute. However, since the introduction of auto-enrolment in January 2026, many employers must now contribute to a qualifying scheme to avoid enrolling staff in the “My Future Fund.” Many proactive employers choose to contribute to their staff’s personal retirement savings account Ireland to attract talent whilst benefiting from Corporation Tax relief.

What options do I have for my PRSA fund when I reach retirement age?

Upon retirement, you can usually take up to 25% of your fund as a tax-free lump sum, with the remainder used to provide a steady income. You have the flexibility to purchase an annuity Ireland retirees rely on for a guaranteed lifelong payment or transfer the balance into an approved retirement fund Ireland that keeps your capital invested whilst providing flexible drawdown income. This allows you to keep your capital invested whilst drawing down a flexible income that suits your specific lifestyle needs and goals.

How do I start a PRSA if I am self-employed?

Starting a PRSA as a self-employed person is a straightforward process that begins with selecting a provider and an investment strategy that matches your risk appetite. You can set up regular monthly payments or make one-off contributions to offset your tax bill before the annual October deadline. Working with a qualified advisor ensures that your plan is tailored to your business’s cash flow whilst maximising the generous tax relief available to you.

Disclaimer

Engage Financial Services LTD T/A Engage Financial Solutions is regulated by the Central Bank of Ireland CRO 764570. Director David Moore. Suite 2 First Floor, 14 -18 Main street, Blackrock, Co Dublin A94 W0Y3