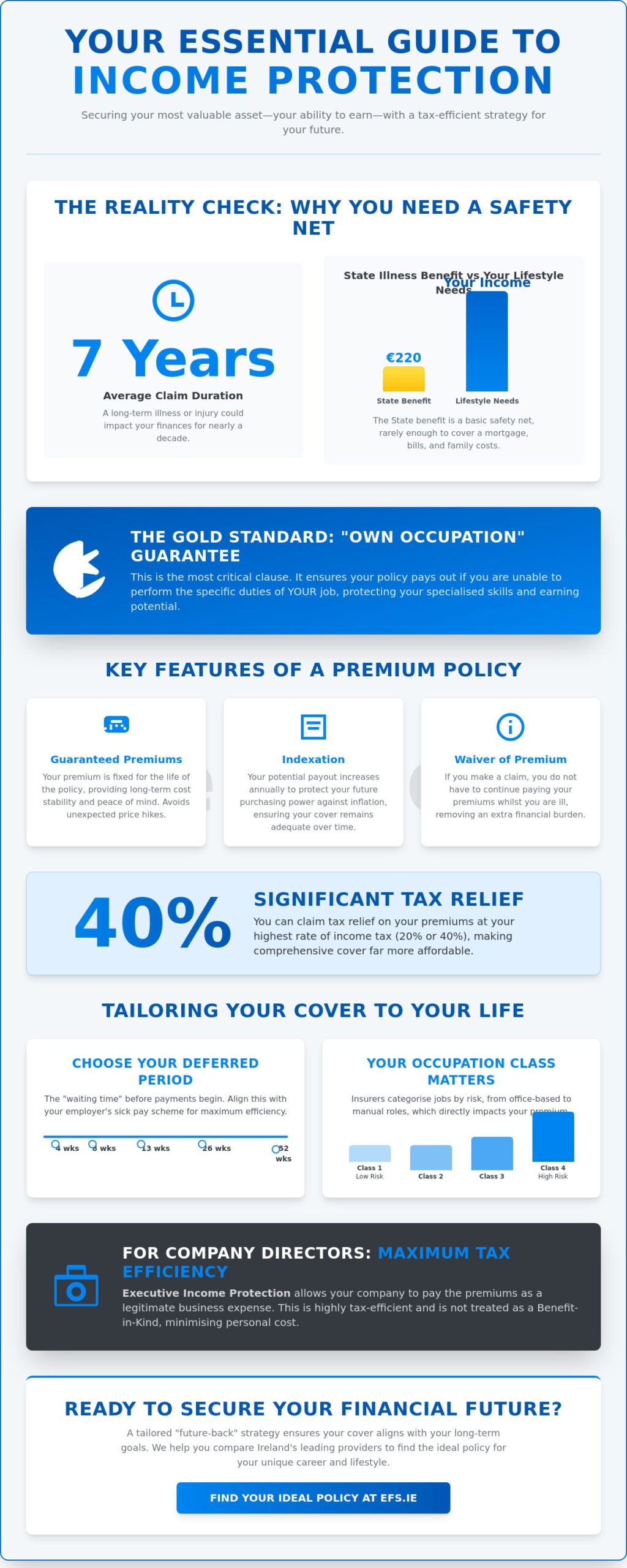

Did you know that the average income protection claim in Ireland lasts for approximately seven years? While the State Illness Benefit provides a basic safety net of €220 per week in 2026, it is rarely enough to maintain your current lifestyle or cover a mortgage. Finding the best income protection policy Ireland has to offer isn’t just about picking the cheapest premium. It’s about ensuring your specific occupation is correctly classified and that you’re making the most of the 40% tax relief available to you.

We understand that the fine print can feel overwhelming, especially when you’re trying to distinguish between income protection and serious illness cover. You want the peace of mind that comes from knowing a claim won’t be rejected due to a simple misunderstanding during the application process. This guide will help you identify the ideal policy for your career and lifestyle for the year ahead. We’ll compare the leading providers, explain how to secure tax-efficient financial security, and show you how to balance comprehensive benefits with affordable long-term costs. By the end, you’ll have a clear path to a more stable financial future.

Key Takeaways

- Understand why the specific definition of “disability” is the most critical factor in ensuring your policy actually pays out for your unique professional role.

- Learn how to choose between different deferred periods to find the perfect balance between affordable premiums and immediate financial security.

- Compare the “Big Five” providers to identify which company offers the best income protection policy Ireland has for your specific career path.

- Discover how company directors can utilise Executive Income Protection to secure their future with maximum tax efficiency and minimal personal cost.

- See how a tailored “future-back” strategy simplifies the application process and keeps your cover aligned with your long-term lifestyle goals.

##Table of Contents

-

Defining the "Best" Income Protection Policy in Ireland for 2026

-

Essential Features that Separate Premium Policies from Basic Cover

-

Comparing Ireland’s Leading Providers: Which One Fits Your Profile?

-

Tailoring Your Cover: Self-Employed vs Employee Requirements

##Defining the "Best" Income Protection Policy in Ireland for 2026

Your ability to earn an income is, without question, your most significant financial asset. Over a forty-year career, even a modest salary represents a multi-million-euro lifetime value. When searching for the best income protection policy Ireland can provide, you aren’t just looking for a low-cost premium; you’re looking for a contract that guarantees financial stability if you’re unable to work due to illness or injury. The "best" policy is one that aligns perfectly with your specific professional duties, ensuring that if you cannot do your job, the insurer steps in to provide a replacement salary. At Engage Financial Solutions, we help you identify the nuances that make a policy truly reliable.

The gold standard in this market is the "Own Occupation" definition. This specific clause ensures that the policy pays out if you’re unable to perform the specific duties of your own job, rather than any job you might be suited for. Income protection insurance is designed to safeguard your lifestyle, not just provide a bare minimum existence. In Ireland, these policies are exceptionally tax-efficient. You can claim tax relief on your premiums at your highest rate of income tax, whether that is 20% or 40%, making high-quality cover far more accessible than many people realise.

Why One-Size-Fits-All Doesn’t Work

A policy that offers excellent value for a software developer might be completely unsuitable for a site foreman. Insurers categorise jobs into occupation classes, typically ranging from Class 1 (clerical and administrative) to Class 4 (manual or high-risk roles). These classes dictate your premium costs and the terms of your cover. It’s vital to organise your policy based on what you actually do every day. If your job title says "Manager" but you spend half of your time on a construction site, a generic policy might fail you at the point of claim. Precision in your application is the key to a seamless payout.

Income Protection vs Other Covers

It’s common to confuse income protection with mortgage protection, but they serve very different purposes. Whilst mortgage protection specifically clears your debt if you pass away, income protection keeps your household running while you’re still here but unable to earn. It covers your groceries, utilities, and lifestyle costs. For a deeper dive into how this differs from other safety nets, you might find our guide on Income Protection vs Critical Illness Ireland: Which One Truly Safeguards Your Future? helpful. Income protection is the foundation of a robust plan because it protects the source of all your other financial goals.

##Essential Features that Separate Premium Policies from Basic Cover

Not all policies are created equal. When identifying the best income protection policy Ireland offers for 2026, you must look beyond the monthly cost. Premium policies include specific safeguards that basic cover often lacks. For instance, indexation is a vital "future-back" feature. It ensures that your potential payout increases annually, protecting your future purchasing power against inflation. Without it, a benefit that seems sufficient today might fail to cover your basic expenses in ten or fifteen years. We believe a policy should be a dynamic contract that grows alongside your career.

Another hallmark of a high-quality policy is the "Waiver of Premium." This feature ensures that if you’re ill and claiming your benefit, you don’t have to continue paying your policy premiums. It removes a layer of financial friction at a time when you’re most vulnerable. You should also prioritise "Guaranteed" premiums over "Reviewable" ones. Whilst reviewable premiums might start cheaper, the insurer can increase them as they see fit. Guaranteed premiums remain fixed for the life of the policy, providing the long-term stability we value at Engage Financial Solutions.

The Impact of the Deferred Period

The deferred period is the "waiting time" between your first day of illness and when the insurer starts paying out. You can typically choose between 4, 8, 13, 26, or 52 weeks. Choosing the right one requires a look at your employer’s sick pay scheme. If your company pays full salary for six months, a 26-week deferred period is often the most logical choice. This CCPC guide to income protection highlights how this period acts as a lever for your costs; the longer you can wait, the lower your premium will be. We recommend aligning this with your personal emergency fund to ensure you don’t face a cash-flow gap.

Additional Benefits to Look For

Look for "Partial Return to Work" benefits. These are essential for a seamless transition back to your career, allowing you to receive a reduced benefit whilst you build back up to full-time hours. Some providers also include "Hospital Cash" for short stays or "Life Events" options. These allow you to increase your cover without new medical checks after significant milestones, such as a marriage or the birth of a child. Ultimately, the best income protection policy Ireland provides is one that adapts as your life changes. if you’re unsure which features fit your lifestyle, we can help you with tailoring your financial security to meet your long-term aspirations.

##Comparing Ireland’s Leading Providers: Which One Fits Your Profile?

Choosing the right provider is a pivotal step in securing your financial future. In the Irish market, five major insurers dominate the landscape: Aviva, Zurich, Royal London, New Ireland, and Irish Life. While each offers the core promise of replacing your salary, they differ significantly in their medical support services and claims philosophies. Finding the best income protection policy Ireland has to offer requires looking at how these companies support you beyond the monthly payout. We see our role as helping you navigate these differences to find a partner that values your long-term security as much as you do.

Aviva and Zurich are often praised for their clinical interventions. Aviva’s "Best Doctor" service provides access to a second medical opinion from world-leading specialists, which is invaluable when facing a complex diagnosis. In contrast, Zurich focuses on active recovery by providing dedicated rehabilitation nurses to help you return to health. Royal London differentiates itself through its "Helping Hand" service, which offers emotional and practical support to both you and your family during a difficult period. Meanwhile, Irish Life has invested heavily in a digital-first approach, making the application process remarkably straightforward for standard risks. New Ireland remains a stalwart in the market, frequently favoured for their flexible policy options and strong presence amongst professional brokers.

Provider Strengths at a Glance

-

Aviva stands as a versatile market leader, offering robust terms for a vast range of diverse occupation classes.

-

Zurich has earned a strong reputation for its proactive claims management and specialist medical support teams.

-

Royal London often provides highly competitive pricing for specific age brackets and non-smokers, making them a favourite for budget-conscious professionals.

Underwriting Nuances: Why the "Cheapest" Isn’t Always the Best

The underwriting stage is where your medical history meets the insurer’s rulebook. Different companies view pre-existing conditions, such as back pain or mental health history, through very different lenses. One insurer might offer a standard rate, whilst another might apply a significant exclusion or a premium "loading." Chasing the lowest quote can be a risky strategy if it leads to a policy with exclusions that render it useless for your specific health risks. We often advise clients to use a broker to "pre-screen" their medical history amongst multiple providers before a formal application is made. This proactive step ensures a more seamless experience and helps you secure the best income protection policy Ireland can provide for your unique health profile.

##Tailoring Your Cover: Self-Employed vs Employee Requirements

Whether you’re a sole trader or a PAYE employee, your employment status is the single biggest factor in how you should structure your cover. The best income protection policy Ireland offers for a freelancer looks very different from one designed for a corporate executive. At Engage Financial Solutions, we focus on these distinctions to ensure your safety net has no gaps. We believe that true financial security is built from the ground up, starting with a clear understanding of your current entitlements and tax status.

The Self-Employed Safety Net

If you’re self-employed, you’re particularly vulnerable. Whilst changes in recent years mean those paying Class S PRSI can now access the State Illness Benefit, the 2026 rate of €220 per week is rarely enough to sustain a business or a household. For you, private cover isn’t just a luxury; it’s an essential business continuity tool. When calculating your requirements, it’s vital to focus on your net profit rather than gross turnover. Insurers will look at your average earnings over the last few years, so we recommend a policy that offers flexibility for fluctuating incomes. This ensures you aren’t paying for cover you cannot claim, whilst keeping your lifestyle protected during leaner periods.

Executive Income Protection for Directors

For company directors, the best income protection policy Ireland provides is often "Executive Income Protection." This is a highly tax-efficient arrangement where the company pays the premiums on your behalf. Because the business owns the policy, the premiums are treated as a deductible business expense, which reduces your Corporation Tax bill. Unlike many other benefits, this does not typically trigger a Benefit-in-Kind (BIK) charge for the director. This "Double Tax Relief" can result in an effective saving of up to 52% when you factor in Income Tax, USC, PRSI, and Corporation Tax allowances. It’s easily the most cost-effective way to secure high-level cover without using your own post-tax salary.

Employees should take a different approach by first reviewing their existing "Death in Service" or group risk benefits. Many large employers offer some form of sick pay, but it’s often capped at six months. Employers looking to strengthen these workplace benefits for their entire workforce should explore how a group protection scheme Ireland businesses are adopting can provide tax-deductible "Death in Service" and sick pay benefits at scale. You don’t want to pay for overlapping cover, so we help you integrate a personal policy that begins exactly when your employer’s support ends. This seamless transition prevents any cash-flow friction during a recovery. If you’re ready to see how these tax efficiencies apply to your specific role, you can request a tailored quote to begin securing your professional future.

##Navigating the Market with Engage Financial Solutions

Finding the best income protection policy Ireland provides can feel like a daunting task. Between comparing occupation classes and deciphering deferred periods, the complexity often leads to inertia. At Engage Financial Solutions, we act as the buffer between you and the technical friction of the insurance market. We believe your focus should remain on your career and family, while we handle the meticulous task of tailoring a plan that fits your life perfectly. We handle the friction. As a regulated consultancy, our advice is anchored in your best interests, ensuring that every recommendation is objective and geared towards your long-term stability.

Our "future-back" methodology sets us apart from generic comparison sites. We don’t just look at your current salary; we look at your aspirations, your family’s future, and the legacy you want to build. This holistic perspective allows us to create a flexible strategy that grows as you do, whether you’re moving up the corporate ladder or expanding your own business. By starting with your desired end-state, we ensure the policy you choose today remains relevant for the milestones of tomorrow.

Our Seamless Advisory Process

We’ve refined our process to remove as much stress as possible. Medical underwriting is often the most taxing part of an application, but we simplify this by liaising directly with providers to manage expectations and secure the best possible terms. Our stewardship doesn’t end once your policy is in force. We provide ongoing support to ensure your security remains robust:

-

Whole-of-Market Comparison: We scan the entire Irish market in one sitting to find the provider that best fits your specific occupation and health profile.

-

Liaison and Underwriting: We manage the communication with insurers, saving you hours of administrative work and helping to avoid rejected claims through precise disclosure.

-

Annual Reviews: We review your cover every year to ensure it remains the best income protection policy Ireland can offer as market rates and your personal circumstances evolve.

Start Your Journey to Security

There’s a simple truth in the insurance world: the best time to secure your future is whilst you’re healthy. Premiums are at their lowest when you’re fit, and securing cover now protects you against any future health changes that might make insurance more expensive or difficult to obtain later. We invite you to experience a straightforward, professional consultation where we can map out your financial safety net together. It’s time to replace worry with the quiet confidence of being truly protected.

Book a consultation with Engage Financial Solutions today to find your perfect policy.

##Securing Your Professional Future with Confidence

Identifying the best income protection policy Ireland offers for 2026 is about more than just comparing premiums. It’s about ensuring your contract includes "Own Occupation" cover and indexation to protect your lifestyle against inflation. Whether you’re a company director seeking tax-efficient executive cover or an employee bridging the gap in your sick pay, the right policy provides a foundation of stability for your family. You’ve worked hard to build your career, and safeguarding that effort is a vital step in your financial journey.

At Engage Financial Solutions, we remove the friction from this process. As a firm regulated by the Central Bank of Ireland, we offer access to all major Irish insurance providers and provide personalised guidance from experienced financial consultants. We help you navigate the complexities of medical underwriting so you can focus on what matters most. It’s a straightforward path to long-term security that adapts as your life evolves.

Secure your future with a tailored income protection quote from Engage Financial Solutions. Your future self will thank you for the peace of mind you build today.

##Frequently Asked Questions

Is income protection insurance worth it in Ireland?

Income protection is highly valuable in Ireland because it provides long-term financial security that the State Illness Benefit cannot match. With the 2026 state rate at just €220 per week, most households would face a significant shortfall. A private policy ensures you can maintain your mortgage payments and lifestyle whether you’re recovering from a minor injury or a long-term illness. It’s the only cover that replaces your most valuable asset: your ability to earn.

How much does the best income protection policy cost?

The cost of the best income protection policy Ireland has to offer depends on several personal factors, such as your age, smoker status, and occupation class. Generally, a younger non-smoker in a clerical role will pay less than an older individual in a manual trade. Your choice of deferred period also plays a major role; opting for a longer waiting time can significantly reduce your monthly premium whilst still providing essential long-term cover.

Can I claim tax relief on my income protection premiums?

You can claim tax relief on your premiums at your highest rate of income tax, which is either 20% or 40%. This relief is capped at 10% of your total annual income. For many, this effectively reduces the cost of the policy by nearly half. If you’re a company director, your business can pay the premium as a deductible expense, which often results in even greater tax efficiencies through corporation tax savings and personal tax relief.

What is the difference between guaranteed and reviewable premiums?

Guaranteed premiums remain fixed for the entire duration of your policy, whilst reviewable premiums can be increased by the insurer at set intervals. Reviewable options often start cheaper, but they carry the risk of becoming significantly more expensive as you get older. We generally recommend guaranteed premiums for those seeking long-term stability and predictable costs. This choice ensures your financial plan remains secure without any unexpected price hikes in the future.

Does income protection cover stress and mental health issues?

Yes, most modern policies in Ireland cover stress and mental health issues, provided they prevent you from performing the duties of your specific occupation. These claims are amongst the most common in the Irish market. However, it’s vital to ensure your policy uses the "Own Occupation" definition. This ensures you receive a payout if you’re unable to do your job, regardless of whether you could technically perform a different, less stressful role.

What happens to my policy if I change jobs or move abroad?

Your policy is generally portable if you change jobs within Ireland, but moving abroad requires careful checking of your insurer’s specific terms. Most providers allow you to maintain cover if you move within the EU or to specific countries like the UK, provided you remain a resident of Ireland at the time of application. If you’re planning a permanent move overseas, we recommend reviewing your contract with us to see if a specific "territorial limit" applies to your benefit.

Can I have multiple income protection policies at once?

You can hold multiple policies, but the total benefit you receive is capped at 75% of your gross earned income. This limit exists to ensure you don’t receive more money whilst on claim than you would whilst working. If you have a group scheme through your employer and a personal policy, the insurers will coordinate the payments. We help you organise your cover to ensure you’re not paying for protection you cannot legally claim.

How long do I have to be off work before my policy pays out?

The time you must be off work is determined by your "deferred period," which you choose when you first set up the policy. Common options include 4, 8, 13, 26, or 52 weeks. If you have a 13-week period, your payments will begin after you’ve been unable to work for three months. Aligning this period with your employer’s sick pay scheme or your personal savings is the most efficient way to structure your cover.

Disclaimer

Engage Financial Services LTD T/A Engage Financial Solutions is regulated by the Central Bank of Ireland CRO 764570. Director David Moore. Suite 2 First Floor, 14 -18 Main street, Blackrock, Co Dublin A94 W0Y3