Did you know that the maximum State Pension in 2026 is just €299.30 per week? For many, this figure represents a significant drop from their hard-earned professional income, leaving a gap that could compromise the lifestyle you’ve worked so hard to build. If you feel a sense of unease about your long-term security or find the rules around tax relief a little overwhelming, you aren’t alone. It’s natural to feel that researching a self employed pension Ireland is a task that keeps slipping down your to-do list whilst you focus on the daily demands of running your business.

We’re here to show you that securing your future doesn’t have to be a source of friction. You can actually transform your annual tax bill into a powerful retirement fund, ensuring that your transition into your later years is as rewarding as your career has been. Whether you’re just starting your first venture or you’re an established professional looking to protect your legacy, we’ll help you find a path that feels right for you. This guide provides a clear roadmap for 2026, covering everything from Personal Retirement Savings Accounts (PRSAs) to the latest tax relief limits and the most effective ways to safeguard your financial stability.

Key Takeaways

- Understand the “State Pension Gap” and why a private structure is vital for safeguarding your future lifestyle.

- Identify the most suitable self employed pension Ireland structure by comparing the unique benefits of Personal Pensions and PRSAs.

- Maximise your annual tax efficiency by aligning your contributions with the specific age-related relief limits.

- Establish a clear, straightforward roadmap to assess your cash flow and set achievable retirement milestones.

- Explore how an Approved Retirement Fund (ARF) provides the control and flexibility needed for a seamless transition into retirement.

Understanding the Self-Employed Pension Landscape in Ireland

When you work for yourself, your business is often your primary focus. However, a self employed pension Ireland is a dedicated private structure designed specifically for sole traders and partners to ensure their hard work eventually leads to a comfortable retirement. Unlike employees who might have a company scheme managed for them, you’re the architect of your own future. This independence offers great freedom, but it also requires a proactive approach to avoid the “State Pension Gap.”

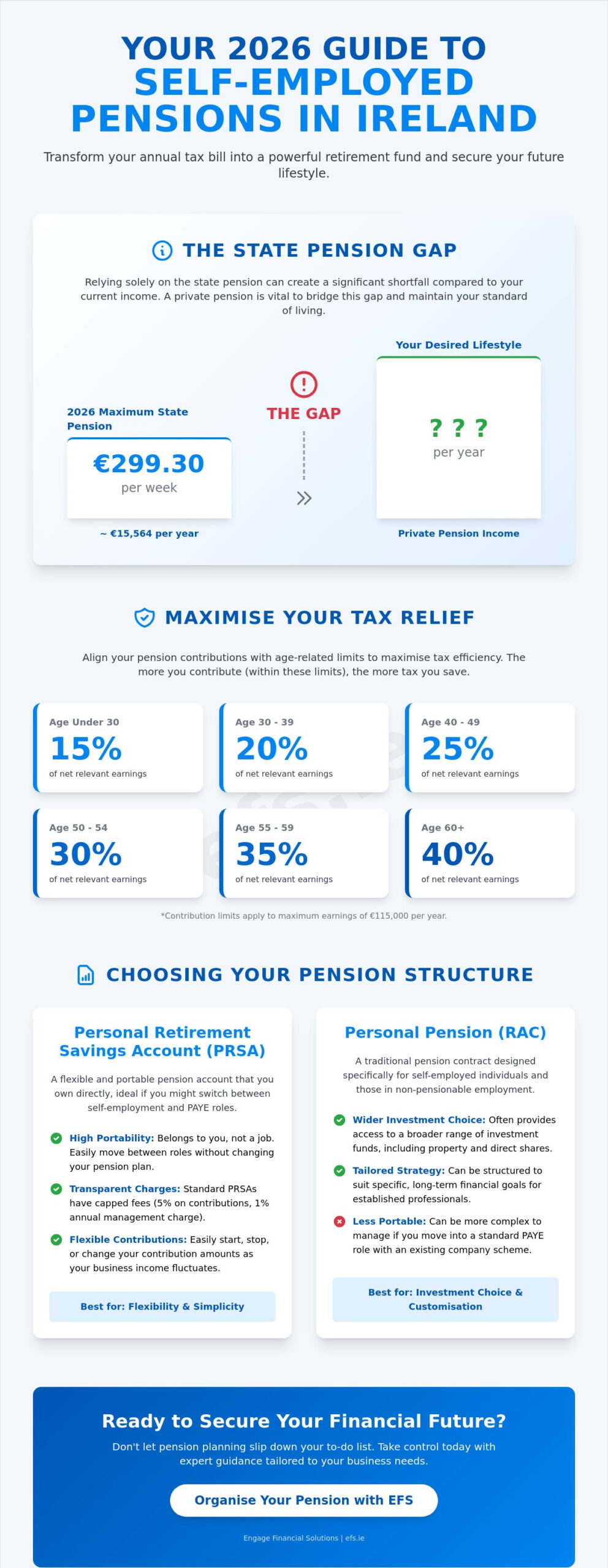

The gap is a very real financial hurdle. In 2026, the maximum contributory State Pension is €299.30 per week, which totals roughly €15,564 per year. For most professionals, this figure is significantly lower than their working income. Relying solely on this basic payment creates a risk to the lifestyle you’ve spent years building. By establishing a private pension, you create a secondary, flexible income stream that acts as a bridge between the state’s basic support and the standard of living you actually desire.

As a self-employed individual, your Class S PRSI contributions are what qualify you for the state’s payment. Whilst these contributions are essential, the Irish pension system is built on the assumption that individuals will supplement this with private savings. Without a personal structure in place, you may find yourself with limited options when you decide to step back from your business.

The State Pension Reality for Business Owners

For those reaching age 66 in 2026, the calculation for your pension is currently in a transition phase. It uses a blend of the “Yearly Average” and the “Total Contributions Approach,” making it vital to have at least 520 contributions to qualify for any payment at all. Whilst Class S contributions provide access to the basic pension, they don’t offer the comprehensive benefits found in other classes. Starting your private fund early allows compound growth to do the heavy lifting, turning modest regular contributions into a substantial safety net over time.

Why Stewardship Matters for the Self-Employed

It’s helpful to move away from viewing a pension as just another tax-deductible expense. Instead, think of it through the lens of stewardship. A pension acts as a vital buffer between your business risks and your personal future. It ensures that your personal wealth is decoupled from the daily volatility of your trade. At Engage Financial Solutions, we act as your steady guide, helping you transition from a transactional view of finance to a holistic strategy that prioritises your long-term stability and peace of mind.

Choosing Your Structure: Personal Pensions vs PRSAs

Deciding how to organise your retirement savings is a pivotal step in your journey as a business owner. In Ireland, you generally choose between two primary vehicles: the Personal Pension Plan, also known as a Retirement Annuity Contract (RAC), and the Personal Retirement Savings Account (PRSA). Both offer significant tax advantages, but they cater to different professional needs and long-term goals.

Selecting the right self employed pension Ireland structure depends largely on your plans for the future. If you value flexibility and the ability to move between self-employment and a traditional PAYE role, one option may stand out. Conversely, if you’re an established professional looking for a highly tailored investment strategy, the traditional route might be more appealing. It’s about finding the balance that provides you with the most peace of mind and financial security.

The Personal Retirement Savings Account (PRSA)

The Personal Retirement Savings Account (PRSA) is often the favourite amongst those who prioritise seamless portability. It belongs to you rather than being tied to a specific employment status. This means you can take it with you if you ever decide to return to a traditional company role. In 2026, Standard PRSAs remain popular due to their capped charges. Legally, these are limited to 5% on each contribution and a 1% annual management fee on the total fund value. This transparency makes it a straightforward choice for many sole traders.

If you require a wider range of investment options, a Non-Standard PRSA might be more appropriate, though these typically come with different fee structures. For a deeper dive into these options, you can read our Personal Retirement Savings Account Ireland: The Comprehensive PRSA Guide.

Personal Pension Plans (Retirement Annuity Contracts)

Personal Pension Plans have long been the traditional route for the self-employed in Ireland. These plans are designed specifically for individuals who have “relevant earnings” from a trade or profession. They remain a robust choice in 2026 for established professionals who want a high degree of investment control. Unlike some standard products, an RAC often allows you to tailor your portfolio to your specific risk appetite more precisely.

Whilst they lack some of the “contract-to-contract” portability of a PRSA, they offer a stable and focused environment for long-term growth. Evaluating the fee structures and investment choices amongst different providers is essential to ensuring your fund isn’t eroded by unnecessary costs. If you aren’t sure which path aligns with your specific business goals, reviewing your options with a trusted guide can help clarify your next steps and ensure your strategy is built for long-term stability.

Maximising Tax Relief: The Financial Advantage of Pension Planning

One of the most compelling reasons to establish a self employed pension Ireland is the immediate financial boost provided by the Irish tax system. Unlike standard savings accounts where you save from your net income, the government essentially subsidises your retirement fund by allowing you to claim relief at your highest rate of tax. This means that a portion of the money you would otherwise pay to Revenue is redirected into your own private fund, allowing your wealth to grow more efficiently than almost any other investment vehicle.

When you contribute to your fund, you are Maximising Tax Relief at either 20% or 40%, depending on your earnings bracket. A unique advantage for the self-employed is the ability to “backdate” contributions. You can make a lump-sum payment before the tax filing deadline in October or November 2026 and elect to have it offset against your 2025 tax bill. This strategy provides a practical way to manage your business cash flow whilst significantly reducing your previous year’s tax liability. It’s a proactive approach that turns a standard tax obligation into a cornerstone of your long-term stability.

Age-Related Contribution Limits Explained

The amount of tax relief you can claim is governed by your age and your net relevant earnings. For 2026, the maximum earnings taken into account for relief purposes is capped at €115,000. The percentage of your income that you can contribute tax-effectively increases as you get older. If you’re under 30, the limit is 15% of your earnings; this rises steadily to 25% for those in their 40s and reaches 40% for individuals aged 60 or over. If you pay tax at the higher rate of 40%, a €100 pension contribution effectively only costs you €60. This immediate 40% “return” on your investment is a powerful tool for building a secure future without the friction of traditional saving methods.

The Benefits of the Tax-Free Lump Sum

Accumulating wealth within a pension structure also offers the benefit of tax-free growth. Any investment gains your fund achieves are not subject to Capital Gains Tax or DIRT, which allows your pot to compound much faster over time. When you eventually reach retirement, you’re entitled to take a 25% tax-free lump sum from your fund, up to a lifetime limit of €200,000. Whether you choose to clear a mortgage, reinvest in a new venture, or simply enjoy the fruits of your career, this lump sum provides a flexible and secure foundation for your post-work life. If you’d like to see how these limits apply to your specific business income, speaking with a professional advisor can help you tailor a plan that maximises every available euro.

How to Organise Your Self-Employed Pension: A Step-by-Step Guide

Setting up a self employed pension Ireland is often viewed as a complex hurdle, yet it is simply a series of logical steps that lead to long-term peace of mind. By breaking down the process into a clear roadmap, you can ensure your financial future is as well-managed as your daily business operations. This methodical approach removes the friction from financial planning, allowing you to focus on your trade whilst your wealth grows in the background.

- Step 1: Conduct a thorough assessment of your current business cash flow. Look at your net relevant earnings after all business expenses to understand what is truly available for your future.

- Step 2: Determine your retirement goals. Utilise a “future-back” perspective to decide when you want to stop working and calculate the annual income you’ll need to maintain your lifestyle.

- Step 3: Choose the structure that aligns with your career trajectory. Consider whether the portability of a PRSA or the tailored nature of a Personal Pension Plan fits your long-term aspirations.

- Step 4: Select an investment strategy. You need to find a balance between growth potential to combat inflation and your personal comfort for market risk.

- Step 5: Consult with a regulated advisor. A steady guide can help you finalise the setup, ensure you are maximising tax relief, and keep your plan compliant with Revenue rules.

Analysing Your Cash Flow for Contributions

Deciding between regular monthly contributions and annual lump sums depends largely on the nature of your trade. If your income is seasonal or project-based, making a lump-sum payment before the tax deadline offers the most flexibility. However, if your revenue is steady, regular monthly payments create a seamless habit of saving without the stress of a large one-off cost. It’s a straightforward approach that allows you to adjust your commitment as your business grows. Balancing business reinvestment with personal retirement safeguarding is key; your pension should act as a secure buffer, not a drain on your working capital.

Selecting Your Investment Strategy

Your strategy should reflect your specific life stage and goals. Younger business owners might prioritise higher growth potential, whilst those closer to retirement often seek to protect their accumulated wealth. Most providers offer “Default Investment Strategies” that automatically reduce risk as you age, but bespoke portfolio management provides a more personalised experience. Regular reviews are essential to ensure your fund stays on track for 2026 and beyond. For a broader view of this process, you can explore our guide on Retirement Planning Ireland: The Comprehensive 2026 Guide to Financial Security.

Taking the first step toward a secure retirement doesn’t have to be overwhelming. If you’re ready to build a tailored roadmap for your future, you can organise your pension setup with a steady guide today.

Planning Your Exit: ARFs, Annuities, and Future Security

The transition from building your wealth to drawing an income is perhaps the most significant milestone in your professional journey. After years of diligent saving into your self employed pension Ireland, you reach a point where your focus shifts from accumulation to sustainable stewardship. Whether you choose to step back at age 60 or wait until 65, the decisions you make now will determine the quality of your retirement for decades to come. This stage is about more than just numbers; it is about ensuring that your exit from the business is as rewarding as your entry was.

In 2026, the two primary paths for your retirement fund are Approved Retirement Funds (ARFs) and Annuities. Each offers a different experience of financial security. One provides the freedom to manage your own capital, whilst the other offers the absolute certainty of a lifelong payment. At Engage Financial Solutions, we act as your steady guide through this logical conclusion of your planning, helping you weigh these options against your personal goals and lifestyle aspirations.

The Flexibility of the ARF

Many self-employed individuals prefer the ARF because it offers a seamless transition from the independence of business ownership to the independence of retirement. An ARF allows you to keep your retirement fund invested, giving you full control over how much you withdraw each year, subject to a minimum “imputed distribution” of 4% from age 61. One of the most valued features of an ARF is its inheritance potential. Unlike other structures, any remaining fund can be transferred to a spouse tax-free upon death, or inherited by children over 21 at a flat 30% tax rate. For a detailed look at managing these withdrawals, you can read our Approved Retirement Fund Ireland: The 2026 Guide to Flexible Post-Work Income.

Securing Stability with an Annuity

If your primary concern is protecting yourself against market volatility or the risk of outliving your savings, an annuity may be the right choice. An annuity involves using your pension pot to purchase a guaranteed monthly income for life. In 2026, a €300,000 fund could typically secure a yearly income of between €12,000 and €15,000 for a 66-year-old, providing a reliable foundation alongside the State Pension. Some retirees even choose a “hybrid” approach, using an annuity to cover their core living costs whilst keeping the remainder in an ARF for flexibility. You can explore these options further in our guide to Annuity Ireland: The Complete Guide to Guaranteed Retirement Income in 2026.

Navigating these choices requires a meticulous eye and a proactive partner. By tailoring a strategy that balances your need for control with your desire for stability, you can ensure your future is as secure as the business you built. We are here to help you finalise these arrangements, providing the calm competence you need to move into your next chapter with total confidence.

Building Your Legacy with Confidence

Securing your financial independence is a journey that begins with a single, proactive decision. By now, you understand that a self employed pension Ireland is more than just a savings pot; it’s a strategic tool that turns your hard-earned business income into a secure personal legacy. Whether you’re leveraging the portability of a PRSA or planning for the flexibility of an ARF, the structures you put in place today will define your standard of living in the years to come. You’ve seen how tax relief can subsidise your savings and how a methodical roadmap removes the friction from complex financial planning.

Engage Financial Solutions acts as your steady guide through every stage of this process. As specialists in seamless financial transitions, we provide expert guidance tailored to the self-employed, ensuring your strategy remains robust and compliant. We are regulated by the Central Bank of Ireland, giving you the peace of mind that comes from working with a trusted advisor. You don’t have to navigate these complexities alone. When you’re ready to move from uncertainty to calm competence, we’re here to help you protect everything you’ve built.

Ready to secure your future? Book a personalised pension consultation with Engage Financial Solutions

Frequently Asked Questions

Can I start a self-employed pension if I have just started my business?

You can establish a pension as soon as you begin trading and earning a professional income. Whether you’re in your first month or your first year of business, starting early allows you to maximise the benefits of compound growth. It’s a proactive way to safeguard your future whilst your business grows, ensuring your long-term security is built alongside your professional success.

How much tax relief can I actually claim on my pension contributions in Ireland?

You can claim relief at your highest rate of tax, either 20% or 40%, on contributions up to specific age-related limits. These limits range from 15% of your net relevant earnings if you’re under 30, up to 40% if you’re aged 60 or over. For 2026, the maximum earnings taken into account for this tax relief is capped at €115,000.

What happens to my pension if my business goes through a difficult period and I stop paying?

Your existing fund will remain invested and continue to grow, even if you need to pause your contributions during a challenging period. Most modern structures, such as a PRSA, offer the flexibility to stop and start payments without incurring penalties or losing your accumulated wealth. This ensures your self employed pension Ireland remains a stable asset that adapts to the natural fluctuations of business life.

Is a PRSA better than a Personal Pension for a sole trader?

Neither structure is objectively better; the right choice depends on your specific needs for flexibility and investment control. A PRSA is often favoured for its portability if you might return to PAYE employment, whilst a Personal Pension may offer more tailored investment options for established professionals. Both provide the same tax relief benefits, so the decision usually rests on which structure feels more seamless for your career trajectory.

What age can I access my self-employed pension funds?

You can generally access your retirement benefits from age 60, though in some specific cases, you may be able to retire as early as 55. If you’re forced to stop working due to serious ill health, you may be able to access your funds earlier. It’s a straightforward process that provides the stability you need as you transition away from your trade and into a new chapter of life.

What happens to my pension fund if I die before retirement?

The full value of your pension fund is typically paid to your estate or your named dependants if you pass away before reaching retirement. This provides a vital layer of protection for your family, ensuring that your hard work continues to safeguard their financial security. The payment is usually made as a tax-free lump sum, subject to certain lifetime limits and Revenue rules.

Can I transfer an old employee pension into my new self-employed scheme?

You can usually transfer the value of a previous employer’s pension into your new self-employed structure to keep your retirement savings in one place. This holistic approach makes it much easier to track your progress and manage your investment strategy. A steady guide can help you navigate the paperwork to ensure the transition is seamless and that you don’t lose any valuable benefits from your previous roles.

How do I claim tax relief on a lump sum pension contribution?

You claim tax relief on a lump sum contribution by including the details in your annual self-assessment tax return. If you make a payment before the 2026 tax deadline, you can choose to offset it against your 2025 earnings to reduce your previous year’s tax bill. It’s a powerful way to manage your cash flow whilst ensuring your self employed pension Ireland is working as efficiently as possible for your future.

Disclaimer

Engage Financial Services Ltd T/A Engage Financial Solutions is regulated by the Central Bank of Ireland CRO 764570. Director David Moore. Suite 2 First Floor, 14-18 Main Street, Blackrock, Co Dublin A94 W0Y3