What if you could halve the cost of your next investment while simultaneously erasing a substantial portion of your 40% income tax bill? It’s common to feel that your options for diversification are limited, particularly when property markets feel crowded or you’re already maximising your pension contributions. Making the EIIS scheme Ireland a part of your portfolio is a proactive way to reclaim control over your tax position whilst supporting the local economy. You’ve worked hard for your income. It’s only natural to want to protect it.

This guide is designed to make the process straightforward, showing you exactly how to maximise your tax efficiency through the Employment Investment Incentive Scheme. Whether you’re looking to support pre-revenue startups or established companies seeking expansion finance, we’ll break down the latest 2026 regulations and explain how to access the 50% relief rate. We’ll outline the path toward capital growth over the next four to seven years. This provides the clarity you need to move forward with confidence, ensuring your investment choices align perfectly with your long-term aspirations.

Key Takeaways

- Identify whether you qualify for the 35% or 50% income tax relief rates based on the age and commercial stage of the Irish company you choose to support.

- Navigate the EIIS scheme Ireland investment limits, which allow for tax-efficient contributions of up to €500,000 for those committed to a seven-year holding period.

- Evaluate the practical differences between managed funds and direct investments to decide which path offers the right level of diversification for your portfolio.

- Align your investment timeline with your long-term goals by using a ‘future-back’ perspective to coordinate capital returns with retirement or mortgage milestones.

- Gain a clear understanding of the risk-reward balance, including how to manage the illiquidity of your capital during the mandatory holding term.

What is the Employment Investment Incentive Scheme (EIIS)?

The EIIS scheme Ireland is a sophisticated tax-planning tool designed to foster a partnership between private investors and the nation’s most ambitious small and medium enterprises (SMEs). At its core, it’s a government-backed initiative that encourages you to provide equity capital to Irish businesses. In exchange for this support, the state provides a significant incentive in the form of income tax relief. It’s a methodical way to build a diversified portfolio whilst directly influencing the growth of the local economy.

This scheme serves a dual purpose that benefits both the individual and the state. For the business, it provides vital, non-debt capital that can be used for expansion, innovation, or hiring new talent. For you, the investor, it offers a way to reclaim up to 50% of your investment through a direct offset against your total income tax. Over the years, the scheme has evolved from a niche incentive into a cornerstone of Irish financial planning. It’s now one of the few remaining ways for high earners to substantially reduce their tax bill outside of traditional pension contributions.

By utilising this scheme, you effectively lower the ‘entry cost’ of your investment. If you invest €20,000 in a company qualifying for the maximum 50% relief, the net cost to you is only €10,000 after your tax refund is processed. This provides a significant cushion against the inherent risks of equity investment and sets a strong foundation for potential capital growth over the holding period. You can explore how these investments fit into a wider tailored financial plan to ensure your long-term security is always the priority.

The Role of EIIS in the Irish Economy

SMEs are the lifeblood of Ireland, accounting for the vast majority of private-sector employment. In a post-2025 landscape where traditional bank lending can be rigid, the EIIS scheme Ireland fills a critical funding gap. It directs capital toward high-growth sectors like Medtech, Green Energy, and ICT. By participating, you’re helping to safeguard jobs and encourage innovation that keeps Ireland competitive on a global stage. The government continues to prioritise this scheme because it recognises that private investment is the most efficient way to drive sustainable economic progress.

Key Terminology for New Investors

To navigate the scheme with confidence, it helps to understand a few specific terms used by Revenue. A ‘Qualifying Company’ is an Irish resident firm that meets strict criteria regarding its size, age, and trade activities. When you invest, you receive ‘Qualifying Shares’, which must be held for a minimum period (usually four to seven years) to retain your tax benefits. There are three main branches of relief you might encounter:

- EII (Employment Investment Incentive): The standard relief available to most individual investors.

- SCI (Start-up Capital Incentive): A specific relief geared toward family members of the company founders.

- SURE (Start-up Relief for Entrepreneurs): Designed for individuals leaving employment to start their own business ventures.

Equity finance involves providing capital to a business in exchange for a share of ownership, allowing the company to grow without the burden of monthly debt repayments.

How the EIIS Tax Relief Mechanism Works in 2026

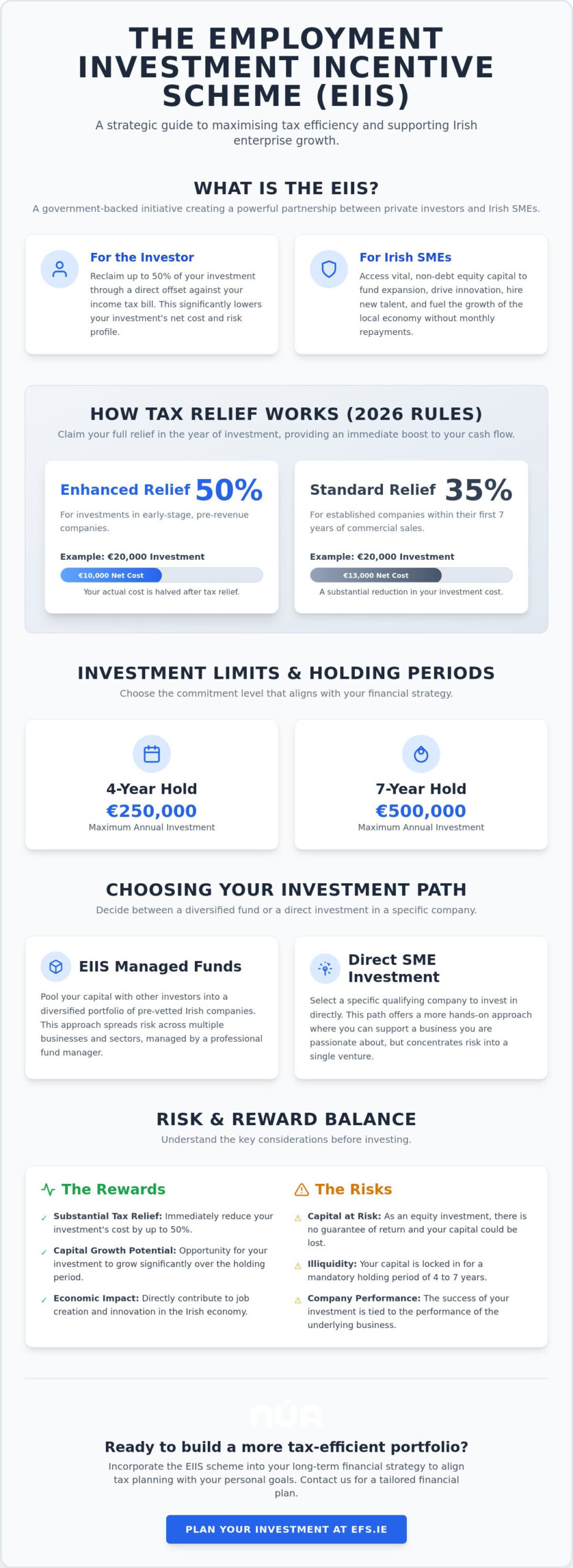

In 2026, the EIIS scheme Ireland remains a cornerstone of efficient tax planning for those looking to manage their liability whilst supporting domestic growth. A significant advantage of the current model is the “Full Relief” approach. Unlike previous versions of the scheme where tax benefits were staggered over several years, you can now typically claim your entire relief in the year the investment is made. This provides an immediate boost to your cash flow, effectively lowering the entry price of your investment from the very start.

The amount of relief you can claim depends entirely on the stage and risk profile of the company you’re backing. For investments in pre-revenue companies that haven’t yet entered any market, you can access a 50% relief rate. If the business is more established but still within its first seven years of commercial sales, the rate is generally 35%. According to the Official Revenue EIIS Guidelines, you can invest up to €250,000 annually for a four-year holding period. If you’re comfortable with a longer commitment, this limit rises to €500,000 for shares held for seven years.

Holding Periods: 4 Years vs 7 Years

Deciding between a four-year and a seven-year commitment is a matter of balancing liquidity with your long-term goals. A four-year term is often the preferred choice for those who want their capital returned sooner, perhaps to fund a specific milestone like a child’s education or a mortgage lump sum. However, the seven-year option is designed for those who want to maximise their investment capacity under the higher €500,000 limit. It’s vital to remember that if you dispose of your shares before the mandatory period ends, Revenue will claw back the relief. This makes it essential to only invest capital that you don’t expect to need in the immediate future.

Calculating Your Potential Savings

Let’s look at how the numbers work in practice. If you invest €10,000 into a qualifying startup that meets the criteria for 50% relief, you’ll receive a tax refund of €5,000. This brings your net cost down to just €5,000, effectively doubling your exposure for every Euro spent. For many high earners, a key benefit is that EIIS relief is often exempt from the High Earners Restriction, meaning it doesn’t count toward the €190,000 cap on certain tax breaks. You can claim your relief by submitting the details through the ‘Income Tax Return’ section of your Revenue MyAccount or ROS portal once you receive your certificate from the company. To see how this fits into your broader portfolio, you might want to review your investment strategy with a professional advisor who understands your specific needs.

Evaluating the Risks and Rewards of EIIS Investments

Every investment involves a careful balance between potential gains and inherent risks. The EIIS scheme Ireland is no exception. Whilst the immediate tax relief provides a significant safety net, it’s vital to remember that this is an equity investment. This means your capital is at risk. Because you’re buying shares in unquoted companies, the value of those shares can go down as well as up. In the event of a business failure, you could lose some or all of your original investment, although the tax relief you’ve already claimed usually remains intact if the company met the initial qualifying criteria.

Another factor to consider is illiquidity. Your money is essentially locked away for the duration of the four or seven-year term. There is no secondary market for these shares, so you cannot simply sell them if you need cash unexpectedly. This requires a “future-back” planning perspective, where you only commit capital that you’re certain you won’t need for the duration of the holding period. However, for those who can manage this timeline, the rewards can extend far beyond the initial tax offset. A DCU Business School analysis of EIIS highlights how this capital is essential for scaling Irish SMEs, which in turn creates the potential for significant capital gains when the company eventually exits or is sold.

Risk Mitigation Strategies

You can manage these risks through meticulous due diligence and a stewardship approach to your portfolio. Whether you’re looking at a high-growth tech startup or a more predictable social infrastructure project like a childcare facility, understanding the management team’s track record is paramount. Social infrastructure projects often carry a different risk profile compared to pre-revenue tech ventures, as they usually involve tangible assets and more predictable cash flows. By diversifying your EIIS commitments across different sectors, you can create a more stable foundation for your long-term wealth.

The Benefit of Professional Guidance

Navigating the complexities of SME valuations requires a steady guide. A professional advisor helps you filter out high-risk ventures that might not align with your stability goals, ensuring you only back companies with robust business plans. It’s also about seeing the big picture of your financial health. Balancing your investments with essential safeguards like mortgage protection Ireland ensures that while you pursue growth through the EIIS scheme Ireland, your family’s most important assets remain secure. This holistic approach allows you to anticipate market shifts with confidence, knowing your entire strategy is tailored to your specific life stages.

Choosing Your Path: EIIS Funds vs. Direct SME Investment

Once you’ve decided to utilise the EIIS scheme Ireland, your next step is choosing the right vehicle for your capital. This decision usually comes down to how much time you wish to devote to the process and your comfort level with selecting individual companies. You can either invest directly in a specific Irish SME or participate through a managed EIIS fund. Both paths offer the same tax relief benefits, but the experience of the investor varies significantly between the two.

Managed funds are a popular choice for those who prefer instant diversification. By investing in a fund, your capital is spread across a portfolio of multiple companies, which helps to mitigate the impact if one business underperforms. The fund manager takes on the role of professional steward, handling the due diligence, reporting, and eventual exit strategy. In contrast, direct investment allows you to back a specific company you believe in, perhaps within a sector you understand well. Whilst direct deals often have lower management fees, they require a more hands-on approach to monitoring your investment’s progress.

Managed Funds: The ‘Seamless’ Approach

For many, the fund model is the most straightforward way to access the scheme. It removes the friction of vetting individual business plans and managing complex paperwork. Fund managers typically handle the ‘clawback’ risk by ensuring all companies in the portfolio remain compliant with Revenue’s requirements. You should be aware of the fee structures, which often include initial commissions and annual management charges. These costs pay for the professional oversight that keeps your investment on track toward a positive outcome.

Direct Investment: For the Attentive Investor

If you’re an experienced investor who enjoys the process of ‘picking a winner’, direct investment can be highly rewarding. You avoid the annual management fees associated with funds, meaning more of your capital gain stays in your pocket upon exit. However, you must be prepared for the administrative burden. You’ll be responsible for managing your own tax certificates and navigating the exit process yourself. For those who find this level of detail overwhelming, it’s often more beneficial to look at the simplicity of broader savings and investments Ireland strategies before committing to a direct EIIS deal.

Deciding which path aligns with your lifestyle is a vital part of your financial journey. If you’re unsure which route offers the best security for your future, you can book a consultation to discuss your EIIS options with a member of our team today.

How to Incorporate EIIS into Your Long-Term Financial Strategy

Successful wealth management often requires a “future-back” perspective. Instead of focusing solely on the immediate tax refund, consider how the eventual exit from the EIIS scheme Ireland aligns with your broader life milestones. Because these investments typically mature in four to seven years, they can be timed to coincide with specific financial needs, such as clearing a mortgage balance, funding a child’s university fees, or boosting your capital just as you enter a new life stage. It’s about ensuring every Euro you invest today is working toward a specific, positive outcome for your future self.

For many Irish investors, the primary challenge is a heavy concentration in residential property. Whilst property has traditionally been a stable asset, the EIIS scheme Ireland offers a vital way to diversify into the equity of high-growth SMEs without losing the tax efficiency you’ve come to expect. Timing is also a critical factor. The final months of the tax year are invariably the busiest period for the scheme, as investors rush to offset their annual liabilities. By starting your evaluation early in the year, you gain the luxury of choice, allowing you to select the projects that best match your risk appetite rather than settling for what remains available in December.

EIIS and Retirement Planning

If you’ve already reached the annual or lifetime limits for pension contributions, the scheme serves as a powerful supplementary tool for retirement planning Ireland. It allows you to continue reducing your tax bill even when your pension “bucket” is full. A key distinction to remember is that whilst pension income is generally taxable upon withdrawal, the relief you receive from an EIIS investment is a tax-free refund of income tax you’ve already paid. This makes it an excellent way to build a pot of capital that can be accessed before your formal retirement age, providing a flexible bridge between your working life and your later years.

Next Steps with Engage Financial Solutions

The complexities of Irish tax legislation don’t have to be a source of stress. Our team acts as a steady guide, providing the calm competence you need to evaluate how these incentives fit into your overall financial health. Whether you’re just starting out and require a first time buyer mortgage Ireland, or you’re an established homeowner looking to optimise your portfolio, we’re here to help. We take a holistic view of your situation, ensuring your investment choices are always tailored to your long-term security. If you’re ready to explore how a personalised strategy can safeguard your future, you can contact us today to begin a partnership built on transparency and expertise.

Taking Control of Your Financial Legacy

Reclaiming a significant portion of your income tax whilst fostering Irish innovation is a strategic way to build long-term security. By exploring the EIIS scheme Ireland, you’ve taken the first step toward a more diversified and efficient portfolio. Whether you’re aligning an investment exit with your retirement or simply seeking to reduce your 40% tax liability, the path forward is now clearer. Success lies in balancing these high-growth opportunities with the stability of a well-rounded financial plan.

Navigating technical Revenue requirements doesn’t have to be a source of stress. As a firm regulated by the Central Bank of Ireland, we possess deep expertise in complex Irish tax-efficient structures. David Moore and the team provide the personalised guidance needed to ensure your investments match your specific life stages. We act as your steady guide, offering the calm competence required to safeguard your wealth and simplify the transition toward your goals.

The right strategy can transform your tax burden into a cornerstone of your success. Secure your financial future with a tailored consultation from Engage Financial Solutions. We look forward to helping you move forward with total confidence.

Frequently Asked Questions

Can I invest in EIIS if I am self-employed in Ireland?

Yes, you can participate in the EIIS scheme Ireland as a self-employed individual. The relief is available to any Irish taxpayer and can be offset against your total income, which includes your professional profits, rental income, and even tax due on employee share options. This makes it a flexible tool for business owners who want to manage their tax liability whilst supporting other domestic enterprises. It’s a straightforward way to diversify your wealth beyond your own business interests.

What is the maximum I can invest in the EIIS scheme in 2026?

In 2026, the maximum amount you can invest and claim tax relief on is €250,000 for shares held for four years. If you’re comfortable with a longer commitment, this limit increases to €500,000 for shares held for a minimum of seven years. These thresholds allow you to tailor your investment capacity to your specific financial goals and liquidity needs. It’s a methodical way to build significant tax-efficient capital whilst adhering to Revenue’s annual limits.

How long do I have to hold my EIIS shares to keep the tax relief?

You must hold your shares for a minimum of four years to retain your tax relief for investments up to €250,000. For larger investments reaching the €500,000 annual limit, a seven-year holding period is required by Revenue. If you dispose of the shares before this term concludes, the tax relief you’ve already claimed will be clawed back. This mandatory period ensures the capital remains with the SME long enough to facilitate genuine growth and innovation within the Irish economy.

Is EIIS tax relief available against the USC or PRSI?

No, tax relief under the EIIS scheme Ireland is only applicable against your income tax liability. It cannot be used to reduce your payments for the Universal Social Charge (USC) or Pay Related Social Insurance (PRSI). When calculating your potential savings, you should focus strictly on the income tax portion of your bill, which is typically the 40% higher rate for most participants. This clarity helps you accurately anticipate the net cost of your investment from the outset.

What happens if the company I invest in goes bust?

If the company ceases to trade, you may lose some or all of your original capital as this is an equity investment. However, you generally don’t have to repay the tax relief already claimed, provided the company was a qualifying entity at the time of investment and followed all Revenue rules. This relief acts as a vital safety net, effectively reducing your total out-of-pocket loss. It reinforces the importance of choosing companies with robust business plans and experienced management teams.

Can I use an EIIS investment to pay off my mortgage early?

You can certainly use the capital returned at the end of your investment term to pay down your mortgage. Many investors use this “future-back” approach to coordinate their EIIS exit with a specific financial milestone. Whether you choose a four-year or seven-year term, the returned funds plus any capital growth provide a tax-efficient lump sum. This can significantly reduce your long-term interest costs and provide the peace of mind that comes from owning your home outright.

How do I actually claim the tax back from Revenue?

You claim your tax back by submitting the details through Revenue’s MyAccount or ROS portal once the qualifying company issues your certificate. For shares issued after October 8, 2019, you can typically claim the full relief in the same year the investment is made. The process is designed to be seamless, with the refund either paid directly to your bank account or adjusted through your tax credits. This immediate boost to your cash flow effectively lowers the entry cost of your investment.

Is there a minimum investment amount for EIIS funds?

Minimum investment amounts for managed EIIS funds typically range between €10,000 and €25,000 depending on the specific fund manager. These thresholds are set to ensure the portfolio can be effectively diversified across multiple companies for all participants. If you’re looking for a lower entry point, some crowdfunding platforms offer qualifying investments for as little as €250. This range of options ensures the scheme remains accessible whether you’re a seasoned investor or just starting your journey toward tax efficiency.

Disclaimer

Engage Financial Services LTD T/A Engage Financial Solutions is regulated by the Central Bank of Ireland CRO 764570. Director David Moore. Suite 2 First Floor, 14 -18 Main street, Blackrock, Co Dublin A94 W0Y3