Over 64,000 first-time buyers have already used the help to buy scheme ireland to bridge the gap between their savings and their first front door. It’s understandable if you feel the pressure of saving a deposit whilst house prices continue to rise, or if you find the technical language used by Revenue more than a little confusing. You deserve a clear path to your new home without the lingering fear that a missed detail might result in a rejected application.

This guide is designed to act as your steady guide through the application process, ensuring you can claim the maximum €30,000 tax refund and accelerate your journey to homeownership. We’ll provide a straightforward breakdown of the 2026 updates, including the extension of the scheme until 2029 and the specific eligibility criteria for new-build properties. By the time you finish reading, you’ll have a tailored understanding of how to manage the five-year residency rule and align your mortgage for a seamless transition into your new property.

Key Takeaways

- Understand how the help to buy scheme ireland functions as a vital tax refund, helping you secure your deposit for a new-build or self-build property.

- Identify whether you meet the essential eligibility requirements, such as being a first-time buyer and maintaining a loan-to-value ratio of at least 70%.

- Learn to calculate your maximum refund of up to €30,000 by reviewing your Income Tax and DIRT contributions from the previous four tax years.

- Gain clarity on the application timeline, from receiving your initial access code to finalising your claim once you have signed your contracts.

- Discover how to integrate this incentive with your mortgage planning to reduce your borrowing needs and safeguard your future financial health.

What is the Help to Buy Scheme in Ireland (2026)?

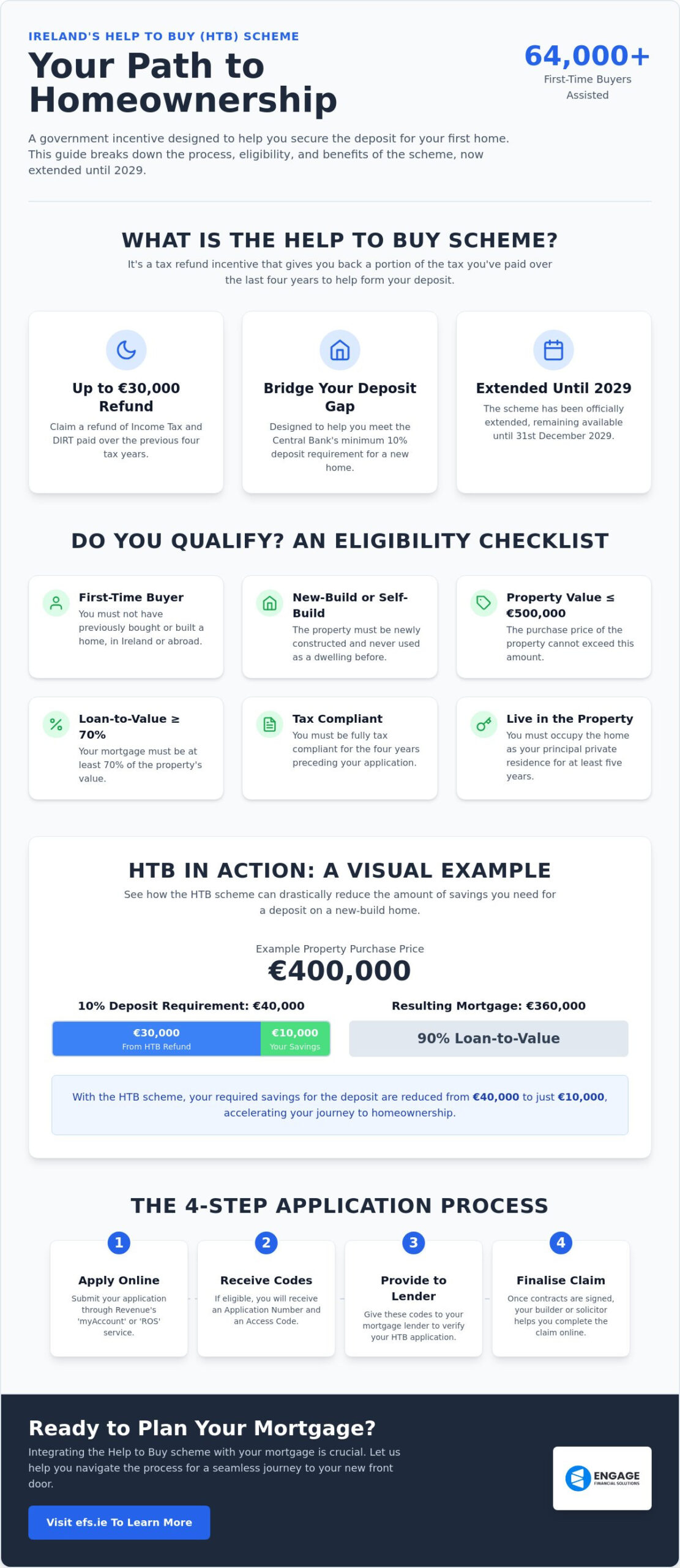

The help to buy scheme ireland is a government-backed initiative designed to turn the dream of homeownership into a tangible reality for those stepping onto the property ladder. It’s essentially a tax refund scheme that allows you to reclaim a portion of the Income Tax and Deposit Interest Retention Tax (DIRT) you’ve paid to Revenue over the previous four tax years. By June 2026, the scheme has already assisted over 64,000 individuals and couples in securing their own homes. With the recent extension confirming its availability until 31st December 2029, it remains a cornerstone of the Irish property market. It positions the refund as a strategic financial bridge, helping you meet the minimum deposit required by lenders without needing years of additional saving. This proactive support ensures you can focus on finding the right home rather than worrying about the initial financial hurdle.

The Core Purpose of the HTB Incentive

The primary reason for this incentive is to help you meet the Central Bank of Ireland’s strict deposit requirements. For most first-time buyers, saving a 10% deposit whilst paying rent can feel like an exhausting, uphill battle. The help to buy scheme ireland effectively bridges this gap, providing a financial cushion that can reach up to €30,000. Beyond just the numbers, it encourages the purchase of newly constructed, energy-efficient homes. This focus ensures that your first step on the property ladder is into a high-quality residence with lower long-term running costs. It offers you a sense of security and financial stability during the early years of your homeownership journey, making the transition to your new home much more manageable and less stressful.

New Builds vs. Self-Builds: What Counts?

To qualify for the refund, the property must be a new residential build that has never been used as a dwelling before. This means second-hand homes are excluded from this specific scheme. If you’re opting for a self-build, the process is slightly different but equally supportive. You must build the home on a site that you own, and the mortgage must still meet the specific loan-to-value requirements of at least 70%. Whether you are buying from a developer or managing your own construction project, the property must be intended as your principal private residence. It’s a long-term commitment. You’re required to live in the home for at least five years to avoid any clawback of the incentive, ensuring the scheme supports genuine homeowners. Mastering these eligibility details is the first step towards a successful claim and a more secure financial future.

Eligibility Criteria: Do You Qualify for the HTB Refund?

Qualifying for the help to buy scheme ireland involves more than just a desire to own a home. It’s a structured process with clear boundaries designed to support those who need it most. You must be a first-time buyer who has never owned, or had an interest in, a residential property in Ireland or abroad. Additionally, your prospective home cannot exceed a purchase price of €500,000. Revenue also requires you to be fully tax-compliant for the four years preceding your application. If you’ve been working abroad or have gaps in your tax history, it’s vital to resolve these early to ensure a seamless application.

The First-Time Buyer Definition in 2026

The term “first-time buyer” carries specific weight in 2026. For those who are separated or divorced, the “Fresh Start” principle may allow you to qualify even if you previously owned a home with a former partner. This is a significant relief for many navigating new life stages. Similarly, inheriting a property doesn’t always lead to an immediate disqualification. Under specific circumstances, such as if you didn’t acquire a right to reside in a dwelling, you might still retain your status. It’s a complex area, so consulting a Citizens Information guide to the Help to Buy Scheme can provide the detailed legal clarity you need. Keep in mind that for joint applications, every person involved must meet these criteria for the group to be eligible.

Understanding the 70% Loan-to-Value Rule

Perhaps the most misunderstood requirement is the 70% Loan-to-Value (LTV) rule. This regulation stipulates that your mortgage must cover at least 70% of the property’s purchase price. It’s a deliberate choice by the government to ensure the incentive supports those who genuinely need a mortgage to buy, rather than “cash buyers” who already possess significant capital. This rule heavily influences your overall first time buyer mortgage Ireland strategy. For example, if you’re buying a house for €400,000, your mortgage must be at least €280,000. Balancing this requirement with your personal savings is a delicate task. If you’re feeling overwhelmed by these calculations, speaking with an expert can help you find a tailored mortgage solution that fits your unique goals.

Calculating Your Refund: How Much Can You Claim?

Determining the exact amount you can reclaim through the help to buy scheme ireland is a vital step in your financial planning. The maximum refund you can receive is capped at the lesser of three amounts: €30,000, 10% of the purchase price, or the total amount of Income Tax and Deposit Interest Retention Tax (DIRT) you’ve paid in the four years prior to your application. It’s a generous incentive, but you’ve to remember that Universal Social Charge (USC) and PRSI contributions aren’t included in this calculation. For those buying from a developer, Revenue pays the refund directly to the contractor as part of your deposit. If you’re undertaking a self-build, the funds are deposited into your bank account after you’ve drawn down the first stage of your mortgage.

The Four-Year Tax Lookback Explained

Revenue’s assessment relies on a specific “lookback” period. They examine your tax contributions from the four years immediately preceding the year of your application. You’ll need to select the most advantageous four-year period within the Official Revenue HTB Scheme Information portal to maximise your claim. If your total tax paid during this time is less than 10% of the house price, your refund will be limited to that lower amount. This is why proactive tax planning is so beneficial. Ensuring all your tax returns are filed and up to date is the only way to safeguard your eligibility for the full amount you’re entitled to.

Property Value Caps and Limits

The scheme maintains a strict €500,000 ceiling on property values. This limit applies to both the purchase price of a new home and the completion value of a self-build. It’s a hard cap. Even if a property is valued at €500,001, you’ll face total disqualification from the incentive. With the median house price in Dublin reaching approximately €475,000 in 2026, many buyers find themselves close to this limit. Whilst focusing on the deposit, don’t forget to account for closing costs for first time home buyer Ireland. These additional expenses, such as solicitor fees and stamp duty, must be budgeted for separately to ensure your journey to homeownership remains stable and stress-free.

Navigating the Application Process and Avoiding Errors

Applying for the help to buy scheme ireland is a methodical journey that requires careful coordination between you, Revenue, and your property professionals. It’s designed to be a seamless process, provided you follow the steps in the correct order. You’ll start by using Revenue’s myAccount or ROS portals to receive your application number and a six-digit access code. This initial step confirms your eligibility and the maximum amount you can reclaim, giving you the confidence to start viewing properties with a clear budget in mind. It’s vital to ensure that the contractor or solicitor you work with is fully registered and approved by Revenue, as they play a critical role in the final verification of your claim.

The Three Stages: Application, Claim, and Verification

Success with the incentive depends on navigating three distinct phases. During the Application stage, you’ll receive a summary of the maximum relief available to you based on your previous four years of tax contributions. This summary is valid for a specific period, so keep an eye on the expiry date. Once you’ve found your new home and signed the contract, you move to the Claim stage. Here, you’ll upload the property details and the signed contract through the Revenue portal. The final step is the Verification stage, where the developer or your solicitor confirms the purchase details. This triggers the payment of the refund, either to the developer as part of your deposit or to your bank account if you’re building your own home.

Avoiding the Revenue Clawback

To safeguard your refund, you must adhere to the residency requirements set by Revenue. The property must remain your principal private residence for at least five years from the date it’s habitable. If you sell the property or move out before this period ends, Revenue may initiate a “clawback,” requiring you to repay a portion of the incentive. Maintaining your status as a tax-compliant resident is essential during this time. By staying proactive and organised, you can protect your financial security and avoid the stress of unexpected audits. If you’re looking for professional support to ensure your application aligns perfectly with your financial goals, you can explore our first-time buyer mortgage solutions for expert guidance.

Strategic Planning: Combining HTB with Your Mortgage

Success in the Irish property market often depends on how well you layer different financial supports. The help to buy scheme ireland isn’t just a standalone refund; it’s a strategic tool that works best when integrated into your broader mortgage plan. By securing this tax refund early, you can effectively increase your deposit, which may lead to more competitive interest rates from lenders. When you bring a larger deposit to the table, you reduce the bank’s risk, often unlocking “green” mortgage rates for energy-efficient new builds. This proactive approach ensures you’re not just buying a home, but building a foundation for long-term financial stability.

HTB vs. The First Home Scheme

Many buyers find that even with the maximum €30,000 refund, a gap still exists between their savings and the purchase price. This is where the First Home Scheme becomes a vital partner. Whilst the help to buy scheme ireland is a refund of your own taxes, the First Home Scheme is a shared equity program where the government takes a stake in your property to bridge the affordability gap. You can utilise both schemes simultaneously to reach a 10% or even 20% deposit mark. It’s a powerful combination that has helped thousands of buyers navigate the median house prices seen in 2026, though you must consider the long-term implications of shared equity on your future ownership.

The Value of Professional Mortgage Advice

Before you commit to a specific property, it’s essential to establish exactly how much can I borrow as a first-time buyer. A professional advisor acts as your steady guide, ensuring your paperwork is meticulous enough to pass Revenue’s strict scrutiny. They also help you navigate the 70% LTV requirement amongst various lenders, as some banks may have different interpretations of how the incentive interacts with their specific lending criteria. Moving from HTB approval to the final drawdown of your mortgage funds requires precision. Having a partner who understands the “future-back” perspective allows you to anticipate potential stresses and neutralise them before they occur, resulting in a truly seamless transition to your new home.

Your Future Home Starts with a Strategic Plan

Securing your first property is a significant milestone that requires both vision and meticulous planning. By mastering the help to buy scheme ireland, you’re not just accessing a tax refund; you’re creating a solid foundation for your long-term financial security. Whether you are navigating the 70% LTV requirement or coordinating your application with the First Home Scheme, having a clear roadmap ensures a seamless transition to homeownership.

As specialists in first-time buyer transitions, Engage Financial Solutions provides the authoritative expertise needed to safeguard your journey. We offer personalised guidance for complex tax scenarios, ensuring every detail of your application is managed with care. As a firm regulated by the Central Bank of Ireland, we prioritise your peace of mind and financial health above all else.

Secure your first home with expert guidance from Engage Financial Solutions. Your path to a new home in 2026 is closer than you think, and we’re here to help you navigate every step with confidence.

Frequently Asked Questions

Can I use the Help to Buy scheme for a second-hand home?

No, the help to buy scheme ireland is exclusively for newly constructed residential properties or self-builds. Second-hand homes do not qualify for this particular tax refund incentive. This focus is designed to stimulate the construction of new housing and ensure first-time buyers have access to modern, energy-efficient homes.

How long does the Help to Buy application take to process in 2026?

The initial application stage via Revenue’s myAccount or ROS is usually instantaneous. You’ll receive your application number and six-digit access code immediately if your tax affairs are in order. The subsequent claim and verification stages depend on your solicitor and developer, so it’s wise to ensure all tax returns from the previous four years are fully filed before you start.

What happens to my HTB refund if I am a self-builder?

For self-build projects, the refund is paid directly into your bank account rather than to a developer. This payment is typically triggered once you’ve drawn down the first stage of your mortgage. You’ll need to provide your solicitor’s details and evidence of the mortgage drawdown to Revenue to facilitate a smooth transfer of funds.

Is the Help to Buy scheme available for investment properties?

No, the scheme is strictly for properties intended as your principal private residence. You must occupy the home for at least five years from the date it’s habitable to avoid a clawback of the funds. If you decide to rent the property out or sell it before this five-year period concludes, you’ll likely have to repay a portion of the refund to Revenue.

Can I apply for Help to Buy if I previously owned a home abroad?

No, you’re not eligible if you have previously owned or had an interest in a residential property anywhere in the world. The help to buy scheme ireland is reserved for genuine first-time buyers. This global requirement ensures the incentive supports those who are truly stepping onto the property ladder for the very first time.

Do I need to have a mortgage approved before applying for HTB?

You don’t need a formal mortgage offer to complete the initial application stage. Obtaining your “Summary of Maximum Relief” first is actually beneficial, as it provides a clear picture of your budget. However, you’ll need your mortgage in place and must meet the 70% loan-to-value requirement before you can move forward to the claim stage.

What is the “Enhanced” Help to Buy scheme?

The “Enhanced” scheme refers to the current higher relief limits of €30,000 or 10% of the property value. These increased limits were originally a temporary measure but have now been extended until 31st December 2029. It offers a much larger financial bridge for first-time buyers than the original 5% or €20,000 caps.

Can I still get HTB if I have been gifted a deposit?

Yes, receiving a gift from family doesn’t disqualify you from the scheme. The critical factor is that your mortgage must still represent at least 70% of the property’s purchase price. As long as you maintain this loan-to-value ratio, you can combine your personal savings, gifted funds, and the tax refund to secure your new home.

Disclaimer

Engage Financial Services LTD T/A Engage Financial Solutions is regulated by the Central Bank of Ireland CRO 764570. Director David Moore. Suite 2 First Floor, 14 -18 Main street, Blackrock, Co Dublin A94 W0Y3