What if you viewed your pension not as a distant savings pot, but as the strategic engineering of your future salary? For many, retirement planning Ireland feels like a maze of complex acronyms and shifting regulations. With the maximum State Pension (Contributory) set at €299.30 per week for 2026, there’s a growing realisation that relying solely on government support may not sustain the lifestyle you’ve worked so hard to build.

It’s entirely natural to feel a sense of unease when faced with the “pension gap” or the alphabet soup of PRSAs, ARFs, and the now-abolished AMRF. Whether you’re decades away from finishing work or approaching your final day at the office, you deserve the peace of mind that comes from a tailored, stable plan. This guide provides the clarity you need to navigate these transitions with confidence. You’ll discover how to maximise your tax relief, understand the new “My Future Fund” auto-enrolment scheme, and choose the right structures to ensure your transition into post-work life is entirely seamless.

Key Takeaways

- Recognise why the State Pension often falls short of maintaining your desired standard of living and how to calculate your personal income goals for a comfortable future.

- Navigate the complexities of retirement planning Ireland by identifying the most suitable savings vehicles, such as PRSAs and company pensions, for your specific career stage.

- Maximise your long-term wealth by utilising the “Triple Tax Advantage” and understanding the specific age-related contribution limits permitted by Revenue.

- Simplify your financial management by consolidating fragmented pension pots into a cohesive, cost-effective portfolio that provides a clear view of your total security.

- Plan a seamless transition to your post-work lifestyle by weighing the benefits of ARFs versus annuities and understanding your tax-free lump sum entitlements.

Understanding Retirement Planning in Ireland: Beyond the State Pension

Retirement planning Ireland is often misunderstood as a simple savings exercise. In reality, it’s the process of defining the lifestyle you want to lead once you stop working and engineering the financial engine required to power it. We encourage a “future-back” approach. Instead of looking at what you can afford to save today, start by envisioning your ideal retirement age and the annual income you’ll need to feel secure. Whether you’re aiming for a quiet life in the countryside or frequent travel abroad, your plan must bridge the gap between your aspirations and your guaranteed supports.

The Irish pension system provides a foundation through the State Pension, but for many middle-to-high income earners, this is merely a starting point. If you rely solely on the state, you may find your post-work standard of living drops significantly compared to your final salary. Recognising this “State Pension Gap” early allows you to take corrective action whilst time is on your side.

The Reality of the Irish State Pension

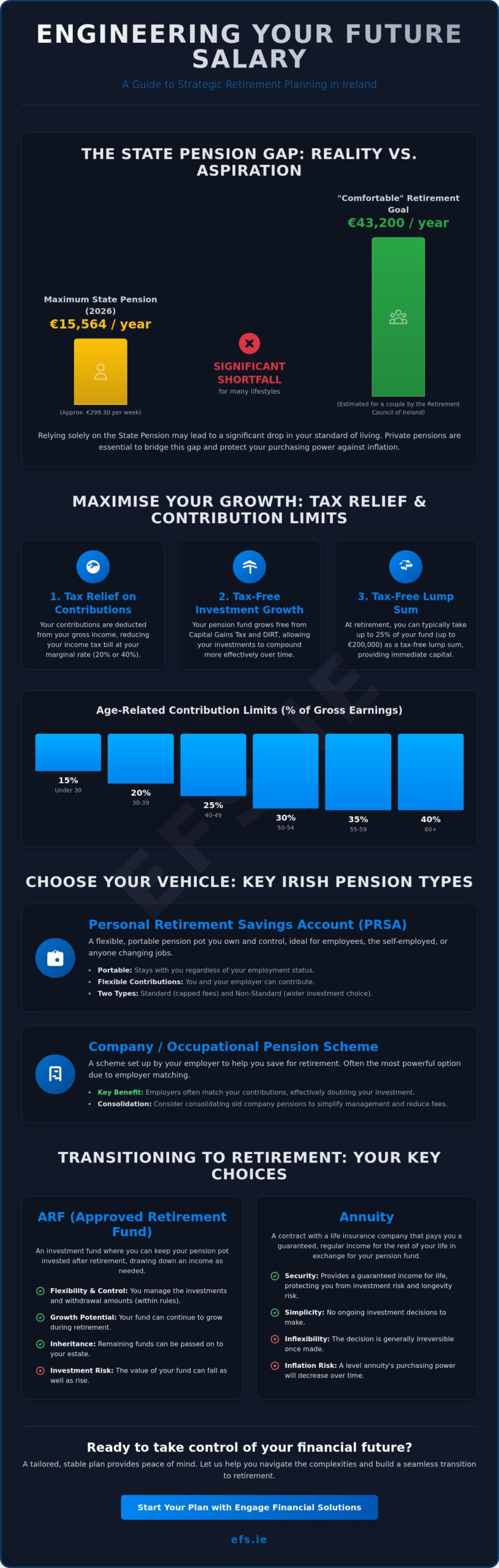

As of January 2026, the maximum personal rate for the State Pension (Contributory) is €299.30 per week for those under 80. This equates to an annual income of approximately €15,563.60. When you consider that the Retirement Council of Ireland estimates a comfortable retirement for a couple requires around €43,200 per year, the shortfall becomes clear. Inflation also plays a silent but significant role. Over a 20-year retirement, the purchasing power of a fixed income can erode, making private pensions and investments essential for long-term stability. For younger generations, the rising dependency ratio makes relying on the state an increasingly risky strategy.

Statutory vs. Mandatory Retirement Age

There is often confusion regarding when you can actually finish work. Whilst the State Pension age is 66, individuals born after January 1, 1958, can now choose to start receiving their pension at any age between 66 and 70. However, your employment contract might still specify a mandatory retirement age. You must understand this distinction, as retiring early can impact your PRSI record and social welfare entitlements. Choosing your own retirement date, rather than having it dictated by a contract or a state timeline, offers a psychological and financial freedom that is central to modern retirement planning Ireland. By taking a proactive stance now, you ensure that your transition is dictated by your goals rather than your circumstances.

Navigating the Irish Pension Landscape: PRSAs, Company, and Personal Pensions

Choosing the right vehicle for retirement planning Ireland is less about picking a product and more about selecting a structure that mirrors your professional life. Whilst the terminology can feel like an alphabet soup of acronyms, the underlying mechanics remain consistent. Every pension is designed to shield your savings from tax as they grow, ensuring that more of your hard-earned money stays working for your future. Whether you’re a salaried employee, a business owner, or a freelancer, identifying the correct framework is the first step toward engineering a stable post-work salary.

The goal is to move from a place of confusion to one of calm competence. By understanding the specific benefits of each “pot,” you can ensure your money is managed with the level of stewardship it deserves. Selecting the wrong structure won’t just cause administrative friction; it could mean missing out on significant employer contributions or paying unnecessary fees that erode your wealth over decades.

Personal Retirement Savings Accounts (PRSA)

The PRSA is perhaps the most flexible tool in the Irish pension toolkit. It’s a portable pot that stays with you regardless of how many times you change employers or if you move between being self-employed and a PAYE worker. For a detailed breakdown of how these function, you can explore our Personal Retirement Savings Account Ireland guide.

You’ll generally choose between a Standard and a Non-Standard PRSA. Standard versions have capped charges, whilst Non-Standard versions offer a wider range of investment options but often come with higher costs. If you value flexibility and want a pension that’s entirely under your control, the PRSA is often the ideal primary vehicle. It’s particularly useful for those whose career paths aren’t linear, as it removes the stress of managing multiple small pots from different jobs.

Occupational and Executive Pensions

If you’re an employee, an occupational pension scheme is often your most valuable financial asset after your family home. The primary advantage here is the employer contribution. Many companies will “match” what you pay in, effectively doubling your investment before tax relief is even considered. This is essentially a pay rise that you’ll receive in the future, and ignoring it is one of the most common mistakes in retirement planning Ireland.

For directors and business owners, Executive Pensions offer even greater scope for corporate contributions. These allow you to extract wealth from your business in a highly tax-efficient manner, bypassing the heavy tax burden of a traditional salary. This structure is meticulously designed to support those with high levels of responsibility, ensuring their personal security is as robust as the businesses they lead. If you’re looking to streamline your approach, speaking with a professional advisor can help clarify which path aligns best with your long-term aspirations.

Strategic Contributions: Maximising Tax Relief and Long-Term Growth

Think of tax relief as a government-funded boost to your future salary. It’s one of the few areas where the state actively encourages you to keep more of your hard-earned money, provided you’re using it to build long-term security. The “Triple Tax Advantage” is the foundation of effective retirement planning Ireland. This framework allows you to claim relief on your contributions, enjoy tax-free investment growth, and eventually take a significant tax-free lump sum at the point of retirement.

For those paying the higher rate of income tax (40%), the immediate benefit is striking. A €100 contribution into your pension pot effectively costs you only €60. The remaining €40 is money that would have otherwise gone to Revenue, but instead, it stays in your pension where it can grow. This represents an immediate 66% return on your net investment before the funds are even invested. Understanding this “Gross vs. Net” distinction is vital. Your gross contribution is the full amount working for you in the market, whilst the net cost is the smaller amount that actually leaves your bank account.

Understanding Revenue Contribution Limits

Revenue sets specific limits on how much you can contribute whilst still receiving tax relief. These limits are based on your age and apply to your gross annual earnings, capped at €115,000 for 2026. If you’re earning above this threshold, you can still contribute more, but you won’t receive relief on the excess. Here is the current breakdown of age-related limits:

- Under 30: 15% of gross income

- 30–39: 20% of gross income

- 40–49: 25% of gross income

- 50–54: 30% of gross income

- 55–59: 35% of gross income

- 60 or over: 40% of gross income

If you haven’t maximised your contributions in previous years, the “carry forward” rule often allows you to claim relief for the prior tax year, provided you do so before the specific October or November deadlines. Regular reviews are essential to ensure you’re making the most of these allowances as you move into higher age brackets or receive salary increases.

The Power of Tax-Free Compounding

Whilst your money is held within a pension structure, it benefits from “gross roll-up.” This means your investments grow without being eroded by Deposit Interest Retention Tax (DIRT) or Capital Gains Tax (CGT), which currently stand at 33% for standard savings and investments. Over a 25-year period, the difference between a fund taxed annually and one growing tax-free is substantial. Compounding is the eighth wonder of the world for retirement. By shielding your gains from the taxman, you allow your wealth to snowball with far greater momentum. To ensure your portfolio is structured to capture this growth efficiently, seeking professional guidance can help you align your contributions with your long-term aspirations.

Organising Your Financial Future: Consolidation and Portfolio Management

Modern career paths rarely follow a single trajectory. For most professionals, a lifetime of work often results in a collection of “fragmented pensions” scattered across various previous employers. Managing multiple pots can be a significant source of friction in retirement planning Ireland, leading to unnecessary administrative stress and, quite often, higher aggregate fees. By organising these disparate funds into a single, cohesive structure, you gain a much clearer view of your total wealth and the progress you’re making toward your post-work goals.

A seamless approach to consolidation does more than just simplify your paperwork. It allows for a unified investment strategy where your assets are managed with consistent stewardship. When your funds are consolidated, it’s far easier to ensure your portfolio remains balanced and aligned with your personal risk tolerance. This reduction in “mental load” is a vital part of the transition, moving you from a state of scattered accounts to one of calm, centralised control.

The Process of Pension Tracing and Consolidation

The first step in taking control is tracking down old pension pots. This usually involves contacting previous HR departments or the trustees of your former schemes. If you’ve lost track of your details, a professional advisor can often assist in the tracing process. Once located, many people choose to move these funds into a Retirement Bond. This is a specific structure designed to house a single pension pot from a previous employment, keeping it secure and accessible until you’re ready to draw it down.

However, you must exercise caution when considering a move. Defined Benefit (DB) schemes, which promise a specific income for life, are increasingly rare and often carry valuable guarantees that are lost upon transfer. Defined Contribution (DC) schemes are generally more straightforward to move, but you should never proceed without a meticulous fee and benefit analysis. A professional review ensures that the move is genuinely in your best interest and that you aren’t sacrificing valuable perks for the sake of convenience.

Investment Stewardship and Risk Profiling

As you move through different life stages, your investment strategy must evolve. In your 30s and 40s, the focus is typically on growth, with a higher tolerance for market fluctuations. As you enter your 50s, the priority shifts toward preservation. This “glide path” ensures that your hard-earned capital is protected from significant market volatility just as you’re preparing to access it. Stewardship means being proactive, adjusting your exposure to ensure your fund is stable enough to support your desired lifestyle. To ensure your portfolio is correctly positioned for your specific stage of life, you can contact Engage Financial Solutions for a personalised risk assessment and a tailored management plan.

Transitioning to Retirement: Choosing Between ARFs and Annuities

The moment you reach the “Retirement Gate” marks a profound shift in your financial life. You move from the accumulation phase, where you’ve meticulously built your wealth, to the drawdown phase, where you begin to enjoy the fruits of your stewardship. This transition is the final, critical piece of retirement planning Ireland. It’s the point where your engineered “future salary” becomes a reality, providing the stability you need to pursue your post-work aspirations with confidence.

Before deciding on your ongoing income, you’ll typically have the option to take a tax-free lump sum. Most Irish pension structures allow you to access up to 25% of your total fund value as a tax-free payment, up to a lifetime limit of €200,000. For many, this provides the capital needed for significant life goals, such as clearing a remaining mortgage or funding a long-held travel ambition. Any amount taken as a lump sum between €200,001 and €500,000 is taxed at the standard rate of 20%, whilst amounts above this are taxed at the higher rate.

For the remaining 75% of your fund, you generally face a choice between two distinct paths: flexibility or a guarantee. Each option offers different benefits depending on your lifestyle needs and your desire for long-term security.

Approved Retirement Funds (ARF): Flexibility and Control

An Approved Retirement Fund (ARF) allows your money to remain invested in the market. This structure offers exceptional flexibility, as you can choose how much to withdraw each year, provided you meet the minimum “imputed distribution” requirements set by Revenue. Between the ages of 61 and 70, you must withdraw at least 4% of the fund value annually, rising to 5% from age 71 onwards.

A significant benefit of an ARF is its inheritance potential; unlike most annuities, the remaining fund can be passed to your estate upon your death. However, this flexibility comes with the risk of “bombing out.” If the underlying investments perform poorly or if your withdrawal rate is too aggressive, you could potentially exhaust the fund during your lifetime. For a deeper look at this flexible option, explore our ARF Ireland guide.

Annuities: The Security of a Guaranteed Income

An annuity is essentially buying a guaranteed salary for life. You hand over your pension pot to an insurance company in exchange for a fixed monthly payment that continues until you pass away, regardless of how long you live. Current annuity rates for a 65-year-old are often in the range of 5% to 5.7% for a single-life, non-escalating plan.

This path removes the stress of market volatility and provides the ultimate peace of mind, knowing exactly what will hit your bank account each month. Whilst an annuity generally lacks the flexibility and inheritance benefits of an ARF, its stability is a powerful tool for those who prioritise a predictable income over investment control. You can learn more about these guaranteed options in our Annuity Ireland guide. By aligning your drawdown strategy with your long-term vision, you ensure that your retirement is as seamless and secure as the plan that built it.

Secure Your Future With Calm Confidence

Effective retirement planning Ireland is less about choosing a single product and more about the meticulous stewardship of your lifelong earnings. By engineering a strategy that maximises your tax relief and organises your fragmented pension pots, you replace financial anxiety with a sense of stable progress. Whether you eventually opt for the flexibility of an ARF or the guaranteed peace of mind provided by an annuity, your plan should be as unique as the lifestyle you’ve worked so hard to build.

Engage Financial Solutions is regulated by the Central Bank of Ireland and provides bespoke financial guidance tailored to your unique goals. Our team are experts in ARFs, PRSAs, and annuities, acting as a steady guide to ensure your transition into post-work life is entirely seamless. You don’t have to navigate these complex financial milestones alone; professional support is here to simplify the process.

Book a personalised retirement consultation with Engage Financial Solutions today to start building your secure future. With the right partner by your side, you can look forward to your retirement with genuine optimism and the comfort of knowing you’re well looked after.

Frequently Asked Questions

What is the best age to start retirement planning in Ireland?

The best age to start is as early as possible, ideally in your 20s, to benefit from the maximum duration of tax-free compounding. Whilst it’s never too late to begin, starting early reduces the monthly contribution required to reach your final income goal. This proactive approach ensures your wealth has decades to grow, creating a more seamless transition to your post-work lifestyle when the time eventually comes.

How much can I contribute to my pension and still get tax relief?

You can receive tax relief on contributions up to a specific percentage of your gross earnings, which is capped at €115,000 for 2026. These limits are age-dependent, ranging from 15% for those under 30 to 40% for those aged 60 or over. Staying within these boundaries allows you to maximise the “Triple Tax Advantage” and safeguard your future salary in a highly efficient, professional manner.

Can I access my pension early if I need the money?

Most private pensions in Ireland can only be accessed from age 50 or 60, depending on the specific type of scheme you hold and your employment status. Early access before these milestones is generally restricted to cases of serious ill-health or specific occupational rules. The system is designed this way to ensure your funds remain protected for their intended purpose: providing stability throughout your later years.

What happens to my pension if I change jobs or move abroad?

If you change jobs, your pension pot remains yours and can often be moved to a new employer’s scheme or a Retirement Bond to keep your savings centralised. Moving abroad allows you to leave the fund in Ireland to grow tax-free or, in some cases, transfer it to a qualifying scheme in your new country. This flexibility ensures your retirement planning Ireland efforts stay with you regardless of where your career leads.

Is the State Pension enough to live on in 2026?

For most people, the 2026 State Pension of €299.30 per week is insufficient to maintain a comfortable standard of living on its own. It’s intended as a basic safety net rather than a full replacement for your working salary. Relying solely on this support often creates a significant income gap, making private provision essential for your long-term financial security and peace of mind.

What is the difference between a PRSA and a Personal Pension?

A PRSA is a flexible, portable account that stays with you across different jobs, whilst a Personal Pension is a contract typically used by the self-employed or those in non-pensionable employment. PRSAs are more modern and adaptable, especially for those with varied career paths. Both structures offer the same core tax benefits, ensuring your savings grow in a protected environment that is tailored to your needs.

Do I have to pay tax on my pension income when I retire?

Yes, the income you draw from your pension in retirement is subject to income tax, USC, and potentially PRSI, just like a regular salary. However, because you likely received tax relief at a higher rate during your working years, the net benefit of the structure remains significant. Proper planning helps you manage these drawdowns to maintain a stable and predictable post-work lifestyle without unnecessary friction.

What is a tax-free lump sum and how much can I get?

You can typically take 25% of your total pension fund as a tax-free lump sum at the point of retirement, up to a lifetime limit of €200,000. This provides a substantial capital boost, allowing you to settle debts or fund specific lifestyle goals as you finish work. Any amount taken above this threshold is subject to tax, so it’s vital to structure your drawdown meticulously to preserve your wealth.

Disclaimer

Engage Financial Services LTD T/A Engage Financial Solutions is regulated by the Central Bank of Ireland CRO 764570. Director David Moore. Suite 2 First Floor, 14 -18 Main Street, Blackrock, Co Dublin A94 W0Y3